The Missing Layoffs

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return next Tuesday and take a look at the compute capacity constraints.

What the Fed Discovered About AI

If you are looking for a way to mathematically justify a $7.6 trillion AI build-out, the cleanest path is labor replacement.

This is the AI maximalist argument: you don't just buy a software tool to help your staff; you buy Agentic AI—autonomous agents running on a $100/month Claude Max plan that can coordinate workflows, act like humans, and work 24/7. In this bullish vision, you replace your $80,000-a-year junior analysts entirely. Last year, Anthropic CEO Dario Amodei made this warning explicit, stating that AI could eliminate up to 50% of all entry-level white-collar jobs within five years, causing unemployment to spike. Under this thesis, the corporate payroll drops, margins expand, and the trillion-dollar valuations of the tech sector make sense.

The underwriting of the AI build-out relies heavily on this assumption of white-collar displacement.

There is just one problem with this thesis. The Federal Reserve just checked the data, and it turns out nobody is getting fired.

Asking the CFOs

Instead of asking tech CEOs what AI will do, economists across the Federal Reserve system decided to ask actual corporate managers what AI is currently doing. Over the last few months, the St. Louis, Richmond, and Atlanta Feds have published a flurry of data testing the AI hype against the mundane, spreadsheet-level reality of ordinary American businesses.

The results are remarkably consistent, and they do not support the Silicon Valley narrative.

First, the St. Louis Fed tracked AI adoption across the U.S. and Europe. They found that while adoption is growing rapidly (with 43% of U.S. workers using AI), there is currently "no evidence that AI adoption is associated with job losses at the industry level."

Second, the Richmond Fed surveyed businesses in December to ask why they were adopting AI. The overwhelming answer was to improve "efficiency and productivity." Reducing labor costs barely registered. The Richmond Fed concluded that firms "do not think of AI primarily as a way to reduce the need for workers."

Finally, a joint study by economists from the Atlanta and Richmond Feds, along with Duke University, surveyed 734 senior financial executives (mostly CFOs). If anyone is eager to replace expensive humans with autonomous $100/month agents to boost margins, it is a corporate CFO. Yet, these executives reported that the expected aggregate employment decline due to AI in 2026 is a negligible 0.4%.

For American workers, this is wonderful news. For AI companies, it complicates the argument for their massive spending.

The Productivity "Wedge"

The obvious defense of this paradigm is that you don't need to fire people to make the math work. Even if companies aren't ready to deploy fully autonomous agents to replace entire departments, surely the lower-end fallback is still a win? Even a basic $30-a-month Copilot license that makes a human worker just 15% more productive is an easy financial victory.

But the Fed economists dug into this defense as well, and they discovered a massive discrepancy—what they call a "productivity wedge."

When you ask corporate managers subjectively how much productivity they are getting from AI, they report big gains. But when the Fed economists calculated implied productivity—the hard math of dividing a company's actual revenue by its actual headcount—the results were shockingly low. In 2025, the actual AI-attributed labor productivity growth across surveyed firms was just 0.6%. For 2026, it is projected to reach only 1.8%.

Why is there such a massive gap between how productive people feel and what actually shows up on the balance sheet?

The Richmond Fed survey provides the answer: firms are currently using AI for tasks, not operations.

Employees are using AI to draft emails, summarize meeting notes, and generate graphs. They are not trusting it to automate their accounting, optimize inventory, or manage supply chains.

This is the Solow productivity paradox in real-time. Drafting an email 10x faster is highly convenient, but it does not mean the firm makes 10x cost savings. It just means the employee has more free time or sends more emails. The productivity gains are "trapped" inside individual workflows and fail to scale to the bottom line.

Unless those theoretical time savings translate into actual payroll cuts, the AI is not saving the company any money. It is simply a net cost increase. You continue to pay the $80,000 salary to keep the human, but now you also pay Microsoft or OpenAI for the software.

The Underwriting Gap

This leaves the stock market in a rather awkward position.

Big Tech is borrowing billions of dollars and issuing massive amounts of equity to build the most expensive infrastructure in corporate history. They are doing this under the assumption that corporate America will eagerly pay to replace its workforce or unlock massive new revenue streams.

But corporate America is looking at the technology and deciding it is basically just a highly advanced spellchecker. They are happy to rent it for $30 a month to make their employees' lives a little easier, but they aren't firing anyone, and their revenues aren't moving.

The gap between what AI is priced to do (replace human labor) and what corporate CFOs say it is actually doing (drafting emails while headcount and revenue stay flat) represents a very wide valuation gap in the market today. If the straightforward path of labor displacement is missing, the road to those massive AI returns becomes a much steeper, more speculative climb.

Signal Stack

The operating reality beneath the headlines.

- Firms and Artificial Intelligence: A Regional Update (Richmond Fed) – In a Fed survey, firms do not think of AI primarily as a way to reduce the need for workers—efficiency and productivity improvements ranked far above labour cost reduction as adoption drivers, and firms using AI were no more likely to report or expect headcount declines than firms not using AI.

📺 On Our Channel

The Networking Bottleneck Behind the AI Boom

A 100,000-GPU cluster requires millions of devices that convert electrical signals to light to keep data moving between racks. Those devices depend on a laser built on indium phosphide, manufactured at scale by fewer than a handful of companies globally. Production is currently 40–60% below demand, and new capacity takes 18-24 months to build—which means this shortage does not clear this year. We break down the layers of the networking stack and which companies are positioned in front of this shift.

Watch ARPU's deep dive on YouTube (13 Mins)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

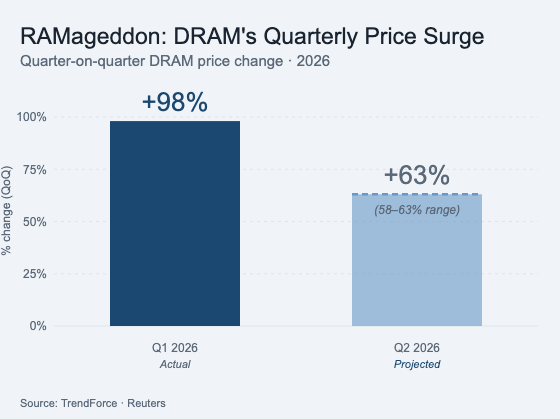

Apple's Memory Bill

- The Data: DRAM prices—the memory chips inside every smartphone, laptop, and tablet—surged 98% in Q1 2026, driven by AI data centres locking up supply through long-term contracts with producers like Micron. A further 58-63% increase is projected for Q2. Industry analysts have called the phenomenon "RAMageddon." Apple, which said it had "never seen a component price increase this much, this quickly," raised MacBook and iPad prices by as much as $300 per model in June—after absorbing the cost for months using existing inventory.

- The Takeaway: The same shortage that produced Micron's record 85% gross margin in FQ3 FY2026 is now repricing consumer hardware. Apple's price hikes are not a company-specific problem—they are the consumer-facing output of a supply chain reorganised around AI data centre demand. IDC projects the smartphone market will see its largest-ever annual decline of 14% in 2026, and the PC market to fall 11.3%.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.