The AI CapEX Story (Part 2): Awaiting the Business Model

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return next Tuesday to look at Microsoft.

The $7.6 Trillion Question

Silicon Valley has always had a high tolerance for faith-based investing, but the current cycle has elevated this to an institutional doctrine: if you pour enough billions into building a technology, the business model will eventually catch up.

And it seems to work, at least for now. OpenAI and Anthropic have scaled to billions in recurring revenue at record-breaking speeds (albeit at a massive operating loss). But the philosophical starting point of this boom was remarkably casual. In 2019, when asked how OpenAI actually planned to make money, Sam Altman offered an answer that was more honest than most fundraising pitches allow:

We have never made any revenue. We have no current plans to make revenue. We have no idea about how we may one day generate revenue. We have made a soft promise to investors that once we build this sort-of generally intelligent system, basically we will ask it to figure out a way to generate an investment return.

This is either the most candid investor update in Silicon Valley history or the most alarming. Probably both. It is also, more or less, the operating assumption behind the $7.6 trillion AI infrastructure build-out.

Big Tech is currently emptying its pockets, draining cash flows, and issuing equity to pay for data centers. Wall Street has eagerly endorsed this, bidding up valuations on the assumption that this massive CapEx will translate into a historic explosion of corporate profits.

But zoom out from individual spreadsheets to the macroeconomy, and you run into an awkward question: How does a company generate a financial return on hundreds of billions spent on AI capex?

The market is pricing in a very large, very fast return on one of the largest infrastructure build-outs in history.

That return has to come from somewhere. Broadly speaking, there are three paths.

Path A: Firing the Human

The most obvious way to generate a return is to cut costs. You replace human labor with an AI agent. The five junior employees who used to draft memos, answer support tickets, and write basic code become one senior employee supervising a machine.

While hard economic data has yet to show a major wave of AI-driven job losses, the corporate intent is already being mapped out. In the World Economic Forum's latest Future of Jobs Report, 41% of employers globally said they expect to reduce their workforce where AI can automate tasks within the next five years. Anthropic CEO Dario Amodei has warned that AI could replace up to half of entry-level office jobs in the same timeframe.

For a single corporation, this looks fantastic on a quarterly earnings report. Headcount shrinks, margins expand, and the investment pays for itself.

But economy-wise, this path is messy. Consumption makes up roughly 70% of the U.S. economy. The worker who looks like a cost line on one company's balance sheet is another company's customer. You can boost corporate margins by replacing labor right up until the point where you realize the labor force was also your customer base. It is a classic tragedy of the commons. If one firm automates away its staff, its margins win. If every firm does it, the aggregate income of the economy collapses. You can build the most efficient, AI-optimized enterprise software in the world, but you cannot sell it to a client base whose own customers no longer have paychecks

Path B: The Disinflation Bargain

The more benign alternative is that companies do not fire anyone. They keep their entire workforce and use AI to make them dramatically more productive.

At the macro level, this is the best version of the AI story. More output with the same workers means lower unit costs, bringing down inflation without a recession.

But for investors, the math is complicated. Productivity-led disinflation is good for the economy, but it is not necessarily good for high stock valuations.

If every competitor becomes more productive at the same time, competition forces them to pass those savings to customers via lower prices. Revenue is price multiplied by volume (R=P×V). If productivity gains from AI increase volume but lowers prices, the net effect on top-line revenue is flat unless demand is highly elastic. If demand doesn't expand fast enough, the owners of the infrastructure discover they spent hundreds of billions of dollars to create a world where everyone else captures the surplus.

That is the disinflation bargain: great macro, disappointing equity math.

And this is compounded by how the build-out is funded. Companies have raised over $100 billion in new debt to fund AI infrastructure. Debt is a fixed nominal obligation. It does not care if competition erodes pricing power faster than expected.

AI can probably make the economy more abundant but less inflationary, but nominal revenue growth might also stall. Companies that borrowed in nominal dollars will find their real debt burdens heavier precisely when revenue growth is disappointing. The economy can get better while the trade gets harder.

Path C: The New Frontier

There is a third path—the one history often delivers.

Major technologies do not only replace old work. They create new work. The internet destroyed travel agents, classifieds, and parts of physical retail, but it also created cloud computing, digital advertising, cybersecurity, e-commerce logistics, and entire software categories that did not exist before.

The World Economic Forum’s data makes the same point. The report that says 41% of employers expect AI-related workforce reductions also projects 170 million new jobs created against 92 million displaced—a net gain of 78 million roles.

AI's new markets are not difficult to imagine: accelerated drug discovery, personalized healthcare, AI tutors, scientific automation, and new creative industries. These would represent new economic output, not just cheaper versions of existing work. This is the outcome that could justify the $7.6 trillion build-out.

But it is also the least proven path. Cost cuts show up next quarter. New categories of demand take years to form. Which brings us to the central problem.

The Timing Trap

The costs of the AI boom are front-loaded. The benefits are back-loaded.

Right now, the spending itself is stimulative. Building data centers and buying chips employs construction firms, engineers, and semiconductor manufacturers. This is why the economy looks strong today, even as the underlying financial tensions accumulate.

But the return on that investment arrives much later. The internet provides the historical benchmark. The foundational infrastructure of the modern web was built in the late 1990s. The business models that actually justified it—streaming, cloud, e-commerce—took a decade to mature.

The dot-com crash was not a verdict that the internet was a bad idea. It was a verdict that 1999 valuations had priced in a 2009 world. AI appears to be following the same arc. Valuations are pricing in returns that may be, by historical precedent, a decade away.

The Demanding Model

This is the real problem with the AI return equation.

Current stock market valuations assume a highly demanding combination of outcomes arriving on a compressed timeline. They assume AI will raise productivity without causing mass unemployment, lower costs without forcing margin-eroding price cuts, and create new industries fast enough to carry the debt burden.

A messier version is more likely. Some workers are replaced, but the cost savings arrive too slowly or unevenly to justify current tech multiples. Productivity improves, but competition passes much of the surplus to customers. New markets emerge, but not fast enough to absorb the infrastructure bill. And the owners of the AI build-out discover that AI can be transformative for the economy while still disappointing for shareholders.

AI does not have to disappoint as a technology to disappoint as an investment. The market may have the destination right. It may simply have the clock wrong.

Signal Stack

The operating reality beneath the headlines.

- AI's Macroeconomic Challenges and Promises (NY Fed) – Economists from the NY Fed describe AI's macro risk as a "centrifugal bind": supply-side costs are rising now — memory chips, energy, specialized labor — productivity gains are arriving later, and the financial system is already exposed to debt predicated on returns that have not yet materialized, with all three forces compounding simultaneously.

📺 On Our Channel

Is Nvidia Running Out of Ways to Surprise Wall Street?

Last quarter, Nvidia's revenue jumped 85 percent year-over-year, but its stock barely moved. Meanwhile, five words from Jensen Huang sent Marvell up 32 percent in a single day. A company that has beaten expectations every quarter for three years has trained the market to expect it, and the surprise now flows to everyone around it instead. We broke down Nvidia's four candidates for its next surprise.

Watch ARPU's deep dive on YouTube (9 Mins)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

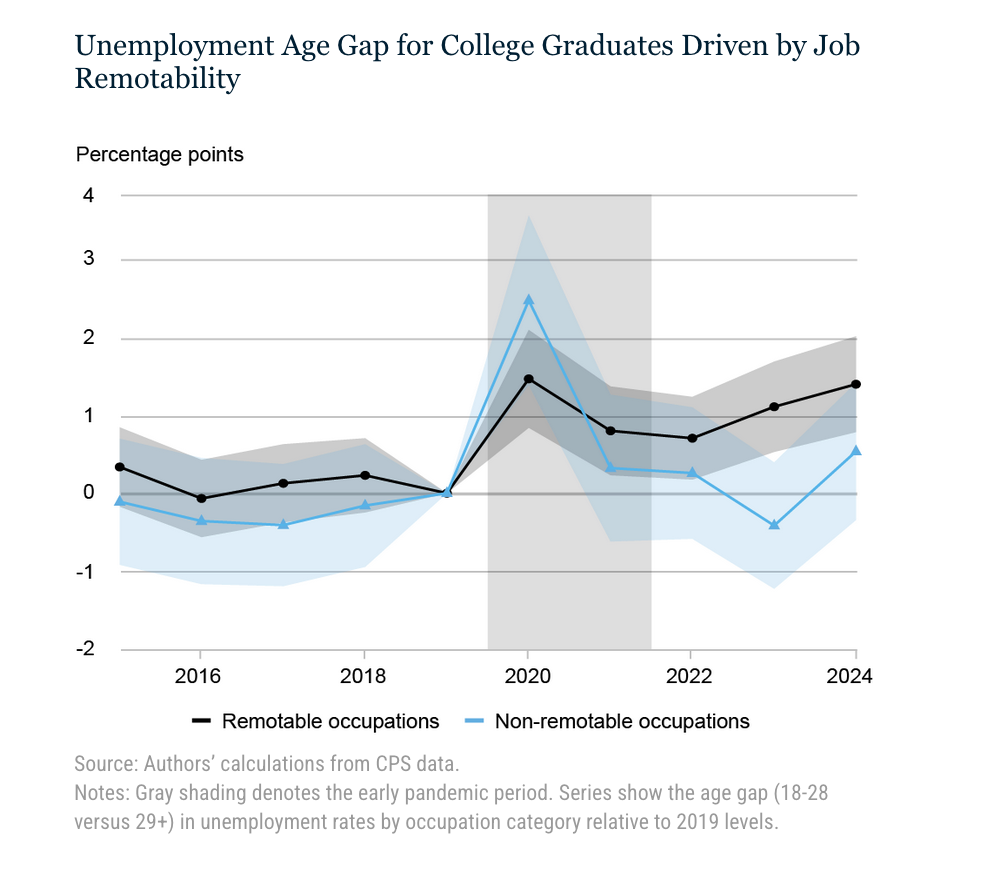

AI Displacement Myth

- The Data: The chart measures how the unemployment gap between young (18–28) and older (29+) college graduates has shifted since 2019, split by job type. A line above zero means young graduates have become more unemployed relative to their older peers than they were in 2019. In remotable jobs like software engineering (black line), that gap has climbed steadily to roughly 1.4 percentage points above its 2019 baseline and kept rising through 2024. In non-remotable jobs (blue line), the gap spiked during the pandemic but returned near zero. The NY Fed estimates remote work accounts for 64 percent of the overall rise in youth unemployment since the pandemic–and specifically rules out AI as the primary driver.

- The Takeaway: The obvious explanation for struggling young graduates has been AI. The evidence points elsewhere. The unemployment gap in remotable jobs predates the rapid diffusion of generative AI and persists even when AI exposure is held constant. The more likely cause is structural and simpler: companies are reluctant to train or retain junior employees they cannot physically supervise.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.