Vibes vs. Margins

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return next Friday to look at Microsoft.

The Audited Margins of AGI

The thing about going public is that Wall Street does not trade in vibes.

In the private markets, you can raise tens of billions of dollars on the promise of building artificial general intelligence, saving humanity, and figuring out the business model later. But when you are prepping an S-1 filing, investment bankers and institutional investors do not care if your CEO is a prophet—unless, of course, your CEO is Elon Musk. For everyone else, they only care about audited margins.

Sometime in late 2026 or 2027, OpenAI and Anthropic are expected to go public. The scale of these listings is almost incomprehensible; The Economist notes that if the major AI labs float just 15% of their shares, it will roughly equal the total capital raised across all U.S. IPOs over the prior decade.

When you are asking public markets to absorb that much equity, you need a flawless financial narrative. And a few months ago, OpenAI realized theirs was broken.

Under the direction of Application Chief Fidji Simo, the company quietly called a "Code Red." They dismantled Sam Altman's "do everything" approach, killing off consumer side quests like the Sora video generator, web browsers, and hardware experiments. The mandate was clear: stop trying to build cool consumer toys, and start chasing Anthropic's boring, high-margin enterprise coding revenue.

This was not a product revelation. It was an economic panic attack.

Rationing the Spice

To understand why OpenAI suddenly had to choose between consumer experiments and enterprise software, you have to look at the physical limits of the AI industry.

Compute is not software; it is heavy industry. In a recent note, Apollo Global Management borrowed a concept from Frank Herbert's Dune, describing compute as the "spice" of our era—the indispensable, physically constrained resource that controls the entire ecosystem. He who controls the compute, controls the universe.

And right now, the universe is tapped out: TSMC's advanced manufacturing nodes are booked solid through 2027. Power grids are maxed out. Spot prices for the DRAM memory needed in AI servers have spiked 8x since 2025.

Because compute is physically scarce, it must be ruthlessly rationed. And the enterprise tools that Wall Street actually values are computationally ruinous to run.

A traditional consumer chatbot request—asking ChatGPT to write a polite email—is computationally cheap. But "agentic" software, like a coding agent that autonomously debugs an enterprise database, consumes 100x to 1,000x more tokens. These models iteratively reason, check their own answers, run continuous loops, and chew through server capacity.

The napkin math is unforgiving. A gigawatt-scale data center costs roughly $8 to $16 billion a year just in depreciation. If OpenAI's new enterprise tools cost 1,000 times more to run, they cannot afford to waste their limited gigawatts generating videos of skateboarding cats for free users.

OpenAI originally planned to subsidize this massive consumer cash burn by building an advertising empire inside ChatGPT. Last year, they confidently projected their ad revenue would hit $100 billion by 2030. It was a beautiful spreadsheet assumption. The only problem is reality.

Emarketer recently analyzed the market and estimated that by 2030, the entire U.S. market for standalone chatbot ads—including Microsoft, Google, Amazon, and OpenAI combined—will max out at a measly $5.41 billion. For OpenAI's math to work, they would need to single-handedly capture nearly 20 times the revenue of their entire addressable market, outperforming the historical growth of every advertising format ever invented.

It turns out that while people love asking a chatbot for a recipe, advertisers are not willing to pay $100 billion to sponsor it. If you cannot monetize consumer curiosity with ads, and your compute costs are scaling exponentially, the consumer "everything app" strategy collapses. Every scarce GPU must be routed to the only token that carries a real margin: B2B enterprise software.

The Wall Street Reality Check

This pivot to enterprise is urgent because OpenAI is listing into a public market that is rapidly losing its patience with the AI hype cycle.

For three years, investors funded the AI boom on the assumption that AI would instantly make corporate America vastly more profitable. But as Torsten Slok of Apollo Global Management recently pointed out, outside of the tech sector, profit margins in the S&P 493 are completely flat. In heavily regulated, capital-intensive industries, process re-engineering and data governance take years. The "productivity hockey stick" that justifies AI valuations has not yet arrived.

Goldman Sachs' Jim Covello was even more blunt in a recent podcast. Right now, the only entities making real economic profits in the AI boom are the semiconductor companies selling the picks and shovels. The hyperscalers and AI labs are burning capital at the expense of their own free cash flow.

Here's Covello:

At some point you got to make money. You make investments in a business so that you can generate returns... We've gotten further away from that over the last couple of years instead of closer to it. That doesn't mean it's never going to happen. It just means the stakes are higher.

This is why OpenAI is sweating. They recorded an $8 billion net loss in 2025 and are projecting $115 billion in cumulative losses through 2029.

More importantly, they are on a ticking clock. In Amazon's recent $110 billion funding round, $35 billion of their commitment is reportedly contingent on OpenAI either achieving AGI or completing its IPO by the end of the year.

Spoiler alert: they are going to choose the IPO.

From Prophets to Profits

OpenAI's top-line revenue—a reported $25 billion annualized run rate as of early 2026—looks fantastic, right up until an investment banker looks under the hood. Roughly 60% of that comes from consumer subscriptions, and they are fickle and low-margin.

To justify its astronomical valuation in the public markets, OpenAI has to launder its consumer user base into sticky, high-margin enterprise revenue before the S-1 documents are filed. That is why they have negotiated a $10 billion joint venture with private equity firms like Bain and TPG to force their products into PE portfolio companies.

The era of the consumer assistant was just a very expensive, gigawatt-burning loss leader. To survive the largest tech IPO in history, OpenAI has to stop trying to build "God" for the consumer, and start building highly efficient, heavily rationed software for corporate procurement departments.

Signal Stack

The operating reality beneath the headlines.

- Google Gemini Launch Delayed as Tech Falls Short of Internal Goals (Reuters) – Google updated Gemini 3.5 Pro's training data in late June to close a performance gap with rivals, and the results missed internal targets — a signal that frontier model improvement is no longer reliably responding to more data or additional training compute, and that the remaining gains are harder to achieve than the infrastructure spending driving the AI buildout was built to assume.

- Oracle Faces Credit Downgrade as AI Spending Outpaces Cash Flow (Bloomberg) – Roughly half of Oracle's $638 billion contracted future revenue backlog is tied to a single customer—OpenAI—according to S&P estimates, meaning the credit standing of the second-largest non-financial issuer in the US investment-grade bond market depends materially on whether one AI lab's spending commitments hold.

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

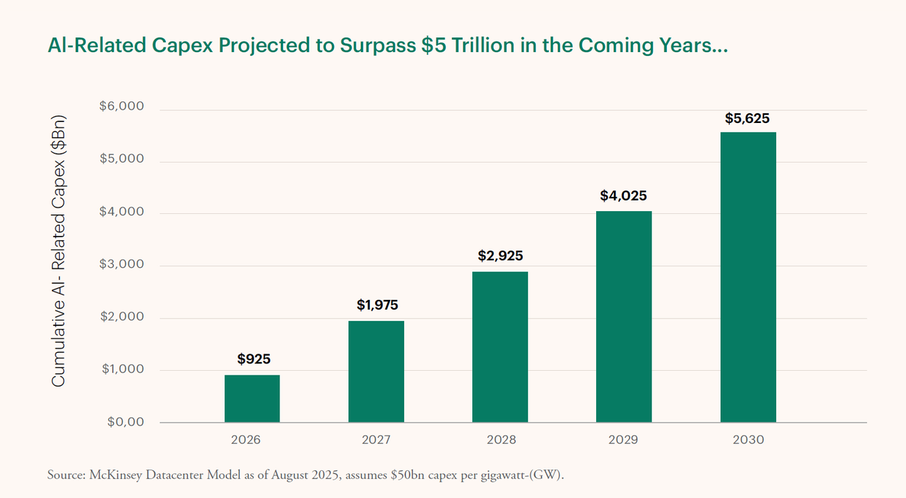

- The Data: The chart tracks cumulative AI-related capital expenditure from 2026 through 2030—covering data centres, power infrastructure, chips, and networking equipment. Each bar represents the running total from the start of the period, not a single year's spend. The cumulative total reaches $925 billion by end-2026, passes $2.9 trillion by 2028, and hits $5.6 trillion by 2030.

- The Takeaway: Apollo frames the financing implication directly: cloud computing was funded gradually over two decades, largely from organic cash flow. AI cannot follow the same model. At $5.6 trillion cumulative through 2030, the capital requirement exceeds what venture capital, free cash flow, and equity markets can absorb. The only pool deep enough is investment-grade debt—public and private—which is why Oracle's credit rating and hyperscaler balance sheet strain are all symptoms of the same structural constraint.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.