The AI CapEx Story (Part 1): Trading Buybacks for GPUs

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return on Friday with Part 2 of the AI CapEx story, exploring the macroeconomic paths to AI profitability.

Manageable Luxury

For the last two years, the stock market has treated Big Tech's AI infrastructure build-out as a manageable luxury.

Sure, buying hundreds of billions of dollars worth of Nvidia GPUs and powering them with dedicated power plants is expensive. But if anyone could afford the AI future, it was Microsoft, Alphabet, Amazon, and Meta.

The accepted narrative was that the hyperscalers could digest these costs out of their operating cash flows. They could build supercomputers, maintain their core businesses, and—most importantly—keep running their massive stock buyback programs without skipping a beat.

But the math is finally starting to assert itself.

PIMCO estimates that hyperscaler capital expenditures will absorb roughly 94% of operating cash flow in 2025 and 2026, up from about 40% in 2023. In other words, almost every dollar coming in the door from search ads and cloud services is going straight out the back door to pay for infrastructure.

When a company's ambitions exceed its cash flow, it has to find the money somewhere else. What we are watching right now is the tech industry executing a sequential funding playbook:

- Phase 1: Operating Cash Flow. You use the cash flow generated by your search engines, social networks, and enterprise softwares to buy servers. (Now exhausted).

- Phase 2: Corporate Bonds. You tap the debt markets, issuing corporate bonds to fund your data centers. (Began last fall, but debt has its limits).

- Phase 3: Equity Issuance. You print new shares.

We have officially arrived at Phase 3. Google recently announced a plan to raise nearly $85 billion in equity, with Meta reportedly weighing a similar offering.

That changes the market equation.

Big Tech had long been one of the stock market's most important buyers. It bought back shares, reduced the supply of equity, and helped support valuations. Now, some of those same companies are moving in the opposite direction. They are reducing the cash available for buybacks, issuing more debt, and, increasingly, preparing to issue more equity.

The ultimate buyers of the stock market are becoming its sellers. And that matters beyond Wall Street.

The Leakage into Real Economy

To understand why a flood of tech equity is bad news for the real economy, you have to look at how the American consumer spending has actually been holding together.

For the asset-owning household—and especially the upper-income consumer that drives a large share of discretionary spending—the stock market and the wallet have become essentially the same thing.

Over the last two years, consumer spending has remained surprisingly resilient despite flat real wages. People are not spending more because their paychecks are bigger; they are spending because they feel wealthier from their stock portfolios. They are "dissaving"—liquidating their personal financial assets to pay for vacations, refrigerators, and cars. The American consumer is effectively using their E-Trade account like a checking account. With the personal savings rate falling to 2.6% (well below its 8.4% historical average), spending is being funded by wealth rather than income.

This strategy only worked because consumers were selling their stocks into a market that had a massive, price-insensitive buyer: the corporations themselves. Corporate share buybacks were the single largest source of net demand for U.S. equities since 2007.

And no group did this more aggressively than the hyperscalers, who spent years repurchasing stock at enormous scale. Tech giants built a perpetual wealth machine, keeping stock prices high and giving everyday consumers a liquid buffer to sell into when inflation pinched.

But the AI boom is breaking this machine.

You cannot logically run a massive share buyback program while simultaneously issuing tens of billions in new equity to pay for data centers. To fund the AI build-out, the free cash flow that once flowed back into share repurchases is being rerouted to GPU clusters.

The consequence cuts both ways. By canceling buybacks, tech giants remove one of the market's most persistent sources of price support. By issuing new stock, they introduce an unprecedented wave of new supply. The floor keeping equity prices elevated is quietly pulled away, while the ceiling of new supply presses down. Portfolios deflate. The wealth buffer shrinks.

The consumer trying to liquidate a few shares to pay for their lifestyle is now competing for market liquidity against a trillion-dollar tech monopoly trying to buy AI accelerators and server racks.

This is the second-order effect of the AI boom that gets lost in the hardware race: it is not just a tech competition, but a massive reallocation of capital. When cash that once went into share buybacks is redirected into GPUs, the effect does not stay neatly inside Silicon Valley. It changes the liquidity backdrop for the broader marke—and, through household portfolios, the consumer economy.

Signal Stack

The operating reality beneath the headlines.

- How AI Debt Financing Impacts Duration Supply and Interest Rates (Dallas Fed) – When data center builders borrow at floating rates from private credit funds and then swap into fixed rates, they are effectively adding bond supply to rates markets without issuing a single bond.

- The Outlook for AI-Related Stocks and US Interest Rates (Goldman Sachs) – Goldman's rates desk argues we're not seeing a repeat of the dotcom era: AI companies have real earnings, credit spreads remain tight, and the credit market is unlikely to pull funding for another 12 to 18 months.

📺 On Our Channel

Intel's CPU Comeback is Real. But Can It Catch TSMC?

As AI shifts from model training to agentic workflows, CPU-side processing now accounts for over 90% of total latency—and the hardware ratio in data centers is moving from one CPU per eight GPUs toward one CPU per two, meaning the same GPU buildout suddenly requires four times as many server CPUs. That structural shift is what made Intel relevant again. We broke down whether it can convert a cyclical shortage into a lasting foundry business capable of challenging TSMC.

Watch ARPU's deep dive on YouTube (18 Mins)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

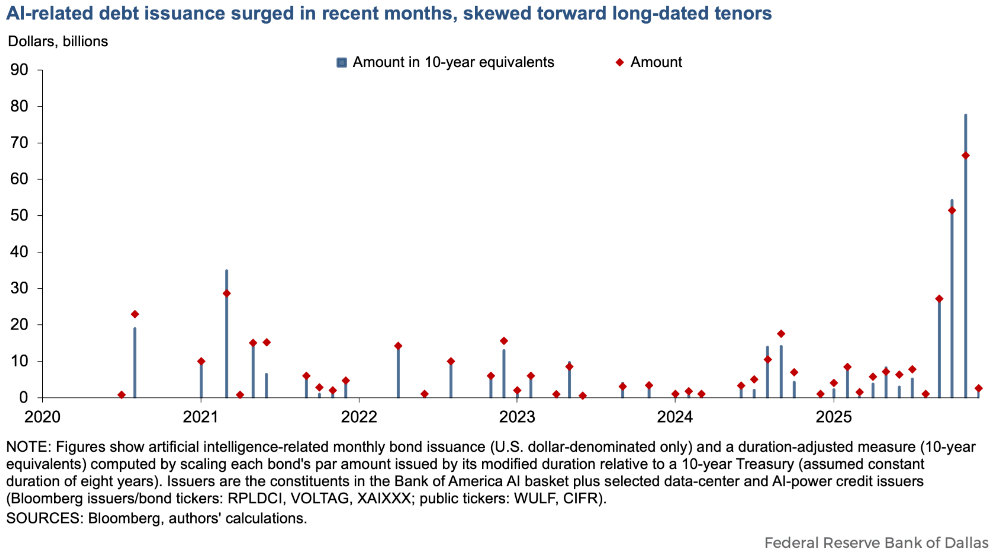

- The Data: AI companies issued a record $77.7 billion in long-term bonds in November 2025 alone. These bonds are unusually long—typically 15 to 30 years—because data centers last decades and companies want to lock in a fixed borrowing cost for the life of the asset, the same logic behind a 30-year fixed mortgage. Wall Street estimates $300 billion in similar AI bonds will be issued in 2026.

- The Takeaway: Most AI coverage focuses on stock prices and chip spend. The less-tracked story is what happens when the world's largest companies take out 30-year mortgages simultaneously, at record scale. Bond markets have to absorb all of it — and absorbing it pushes long-term interest rates higher. By 2026, AI financing could be adding the equivalent of one-eighth of what the US Treasury borrows annually.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.