Meta Has Some Spare GPUs if You Want Them

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return this Friday and take a look at the fragmentation of the AI compute market.

Zuck's Accidental WeWork

There are two ways to enter the cloud infrastructure business. The first is to spend twenty years meticulously building a global platform of enterprise software, storage, and sales teams, like Amazon and Microsoft did.

The second is to buy so many expensive Nvidia chips that you accidentally become an infrastructure landlord—only to realize you have no immediate, tangible use for all that capacity.

Meta appears to have chosen the second path. Under a new initiative dubbed "Meta Compute," the social media giant is preparing to open its private data center gates to the public. Here's Bloomberg:

Meta, which has been rushing to secure expensive data centers and other infrastructure to fuel its own artificial intelligence ambitions, is forming a business to generate revenue from excess computing power sold to outside customers.

One potential plan includes selling access to various AI models that are hosted on Meta's existing AI infrastructure, an approach similar to AWS's Bedrock offering... The company is also considering selling access to "raw" computing capacity, akin to other so-called neocloud businesses like CoreWeave Inc.

On paper, this might be framed as a bold new vector of competition—Mark Zuckerberg taking the fight directly to AWS. In reality, it looks more like a financial pressure release valve to offset the near-term depreciation of a massive capital layout.

The Depreciation Deficit

To understand why a social media company is suddenly trying to rent out servers, you have to look at the unforgiving math of its balance sheet.

Meta has committed a whopping $183 billion to AI infrastructure, including an Ohio data center roughly the size of Manhattan. Zuckerberg's strategy has essentially been: amass as much compute as physically possible, and figure out the exact business model later.

The problem with this strategy is that GPUs are not fine wine. They do not appreciate in value while sitting in a cellar. Hardware sits on a five-year depreciation cycle. If you spend billions on H100 chips, you take a massive depreciation charge against your earnings every quarter. If those chips are actively generating revenue, the math works. If they are just sitting there training open-source models that you give away for free, the depreciation eats a hole in your income statement.

This exposes Meta's disadvantage. When we looked at Microsoft recently, CEO Satya Nadella admitted the company is actively rationing raw GPUs. Microsoft has a massive, paid enterprise bundle (Microsoft 365) where it can charge corporations extra money for AI usage. Meta's core product is a free app where people upload photos, swap memes, and occasionally overshare about their personal lives.

While Meta is undoubtedly using AI to optimize ad targeting and recommend Reels, there is a limit to how much supercomputing power you need to serve a better Instagram ad. Meta simply does not have the direct revenue streams to fully absorb the physical capacity of a Manhattan-sized data center. And Wall Street's patience has a much shorter half-life than an Nvidia chip.

The Skyscraper Pivot

Zuckerberg effectively admitted this was a possibility on an earnings call back in May. Defending his massive spending, he noted: "Obviously if we get to a point where we feel that we have overbuilt, then that is an option that we have [to sell the compute]... that is partially what gives us confidence in investing."

Well, here we are.

Meta isn't entering the cloud computing market because it has a sudden, burning desire to deal with IT procurement departments. It is doing it because it has a $183 billion pile of depreciating silicon that needs to start paying for itself. The closest analogy here isn't Amazon Web Services. It is commercial real estate.

Imagine a developer who buys a 100-story skyscraper on speculation, convinced his own company will eventually grow fast enough to fill the whole thing. Two years later, his employees only take up 30 floors. The building is magnificent, but the property taxes and maintenance costs are bleeding the company dry. So, to appease his accountants, he slaps a "Co-Working Space" sign on the lobby and starts renting out desks on the empty floors to local freelancers.

Meta Compute is Zuck's accidental WeWork.

Renting out excess compute is a perfectly rational financial move to offset costs. SpaceX is doing the exact same thing, renting its Memphis data center to Anthropic and Google. But the more interesting point is what it says about the broad industry context of "AI compute shortage." It seems to suggest the market is getting messier. A company can be short compute for its future ambitions and long compute for its present utilization at the same time. That is not quite AWS. It is not quite WeWork either. It is the weird new middle ground of AI infrastructure: part cloud strategy, part financial pressure release valve, part landlord business with GPUs.

Signal Stack

The operating reality beneath the headlines.

- Colocation Data Centers: The Infrastructure Race Behind AI (McKinsey) - As much as 50 percent of global data center capacity scheduled to come online in 2026 could be delayed by permitting bottlenecks, grid connection wait times now exceeding four years in some markets, and component lead times that have more than doubled since 2019—meaning the physical infrastructure race may be structurally incapable of keeping pace with the demand curve hyperscalers are funding.

- What Meta, Oracle Moves Say About Data Center Economics (CIO) - Oracle's latest 10-K explicitly warns that overbuilding or misjudging demand could leave it with infrastructure assets that cannot be re-leased, repurposed, or assigned on acceptable terms—the clearest acknowledgment yet from a major hyperscaler that the AI data center buildout carries stranded-asset risk at the scale of a $300 billion Stargate commitment.

📺 On Our Channel

Neoclouds: Cloud Companies or GPU Finance Vehicles?

The neocloud business model works like this: borrow against a hyperscaler's take-or-pay contract, buy GPUs, rent those GPUs back to the same hyperscaler, then use the revenue to service the debt and absorb depreciation on hardware. What remains—per CoreWeave's own unit economics—is 16 cents on the dollar. We broke down why that structure makes a neocloud a financing vehicle, not a technology platform.

Watch ARPU's deep dive on YouTube (12 Mins)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

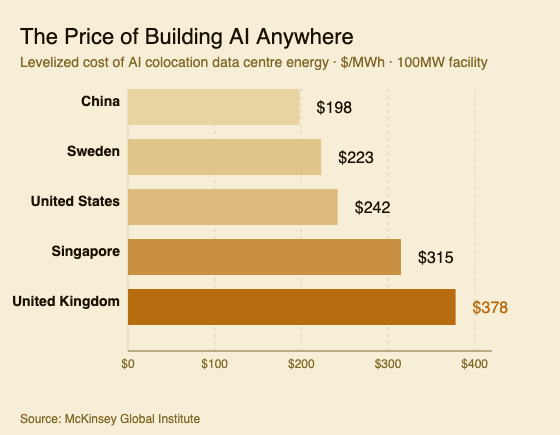

- The Data: The chart shows the levelized cost of building and operating a 100-megawatt AI colocation data centre across five major markets modelled by McKinsey—infrastructure only, excluding IT hardware. Each bar extends proportionally to cost per megawatt-hour of facility energy. China's eastern demand centres are the benchmark at approximately $200. Electricity is the primary driver, accounting for 55 percent of China's cost structure and running 1.9 times higher in London. Northern Sweden's competitive position reflects abundant renewable power and natural cooling.

- The Takeaway: Lower cost does not automatically produce higher returns. McKinsey finds retail colocation generates 20–25 percent equity IRR while wholesale hyperscaler leases return 13–18 percent—a difference driven by contract structure and market saturation, not electricity bills. London and Northern Virginia continue to attract capital despite higher costs because fiber density and proximity to enterprise demand can outweigh the per megawatt-hour electricity disadvantage.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.