Private Equity's Quiet Retreat

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU returns next Tuesday with a two-part investigation into the macroeconomics of the AI capex boom, and the impossible choices it is forcing on the stock market.

Dry Powder Is for Sitting On

Quarterly earnings calls have a way of encouraging broad, optimistic narratives. They are highly structured events where executives can frame market volatility not as a risk, but as a strategic opportunity.

This was especially true in the private equity sector over recent months, as buyout firms faced growing pressure to prove their multi-billion-dollar software portfolios are safe from AI disruption. In February, as the industry's major PE players reported their earnings, the narrative-building was in full swing: the market panic over AI was not a threat; it was a historic buying opportunity.

Apollo CEO Marc Rowan assured analysts that "the market's overreaction to software is extreme" and that his firm was "on offense." KKR co-CEO Scott Nuttall suggested that moments of market anxiety like this "tend to be amazing vintage years for investments." Steve Schwarzman of Blackstone pointed to his firm's roughly $200 billion pile of "dry powder"—cash committed by investors but not yet spent—as a weapon ready to be deployed.

The message to the market was clear: we love the opportunity, and we are about to buy the dip on software.

It was a confident narrative. In reality, underwriting this volatility has proven much harder than pitching it on an earnings call.

The Great Freeze

Four months later, we have the actual deal data. It does not look like an offensive. It looks like a retreat.

According to PitchBook data analyzed by the Financial Times, software buyout deals have collapsed to their lowest level since the Covid-19 pandemic. In the first five months of 2026, PE firms struck just $50 billion in software deals, down from $88 billion in the same period last year. Last year, the industry completed $290 billion in software acquisitions—an eleven-year high. It went from one of the best years to its worst start in eight years in a single turn. If this pace continues, 2026 will be the weakest year for software dealmaking since 2018.

The monthly deal volumes are damning. Software buyouts hit $24 billion in January. By February—right as executives were bragging about their dry powder—that figure had collapsed to $9 billion. By May, it was $5 billion. If the firms were playing offense, they were doing it very quietly.

If these software companies are supposedly trading at attractive, panicked discounts, and if PE firms are sitting on mountains of cash, why is nobody buying?

The Valuation Void

The answer, as it usually does in PE, comes down to the Excel spreadsheet.

To buy a company, a PE firm must present a valuation model to its investment committee and, more importantly, to the private credit funds providing the debt for the purchase. That model predicts cash flows five to seven years out.

But as an analyst told the FT: "Until an investor knows what a business may be worth post-AI adoption, it's impossible for them to make a case to their investment committee."

Software was the perfect PE target because its revenues were sticky. Enterprise integration meant switching costs were prohibitive. You could model 95% customer retention with your eyes closed. Now, autonomous AI agents from Anthropic and others threaten to bypass traditional software interfaces entirely—and with them, the per-seat pricing models that underpin enterprise software valuations. Half the department automated means half the licences needed.

If you are an associate building the valuation model for a software target, how do you project Net Revenue Retention when the very concept of a "user seat" is dissolving? What number do you put in cell G14 for Year 4 revenue?

The paralysis is not only on the equity side. The private credit market—the $3 trillion shadow banking system that finances leveraged buyouts—holds an estimated 20 to 25% of its exposure in software. If the equity sponsors cannot model Year 4 revenue, the credit funds cannot underwrite the loan. You need both to do a deal. And right now, neither side can move.

The Safe Harbor of Concrete

Faced with systemic uncertainty, PE firms do not play offense. They find something else to buy.

The mega-firms are quietly redirecting dry powder toward tangible AI infrastructure. Blackstone formed a joint venture with Google, committing an initial $5 billion in equity to build a new TPU cloud platform with 500 megawatts of capacity expected online in 2027. Meanwhile, KKR launched a $10 billion AI infrastructure company with Nvidia and Vistra.

By the time Blackstone reported its Q1 2026 earnings in April, the language had shifted. Schwarzman described software as having "come into focus as an at-risk area." Rather than trying to pick software winners and losers, firms are buying the physical infrastructure that software runs on.

Ultimately, dry powder makes for a highly comfortable cushion to sit on when the alternative is catching a falling knife. On an earnings call, volatility is an amazing investment vintage. In the investment committee room, it is a risk that cannot be underwritten.

Signal Stack

The operating reality beneath the headlines.

- Private Credit's Exposure to Ailing Software Industry Is Bigger Than Advertised (WSJ) – Four of the largest private-credit funds carried average actual software exposure of 25% against a reported 19%, with one fund at nearly double what it disclosed — at the exact moment AI disruption is making leveraged software loans the riskiest category in private credit.

- Private Credit Market Enters a New Phase (McKinsey) – Redemption requests at semiliquid vehicles hit an estimated 16% of NAV in Q1 2026—more than three times the quarterly cap at several funds—as what managers spent years calling "permanent capital" proved considerably less permanent when software concerns arrived.

📺 On Our Channel

How AI Created a Memory Shortage That Money Can't Fix

The AI memory market has split in two: companies that secured allocations years in advance, and everyone else watching the cost of a gigabit of DRAM rise fivefold in six months. The deeper issue is structural—producing high-bandwidth memory carries a 3-to-1 capacity trade-off against standard chips, meaning every AI server built physically removes memory supply from the rest of the market. We broke down why the world's largest tech companies are now offering to finance their suppliers' $300 million machines.

Watch ARPU's deep dive on YouTube (9 Mins)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

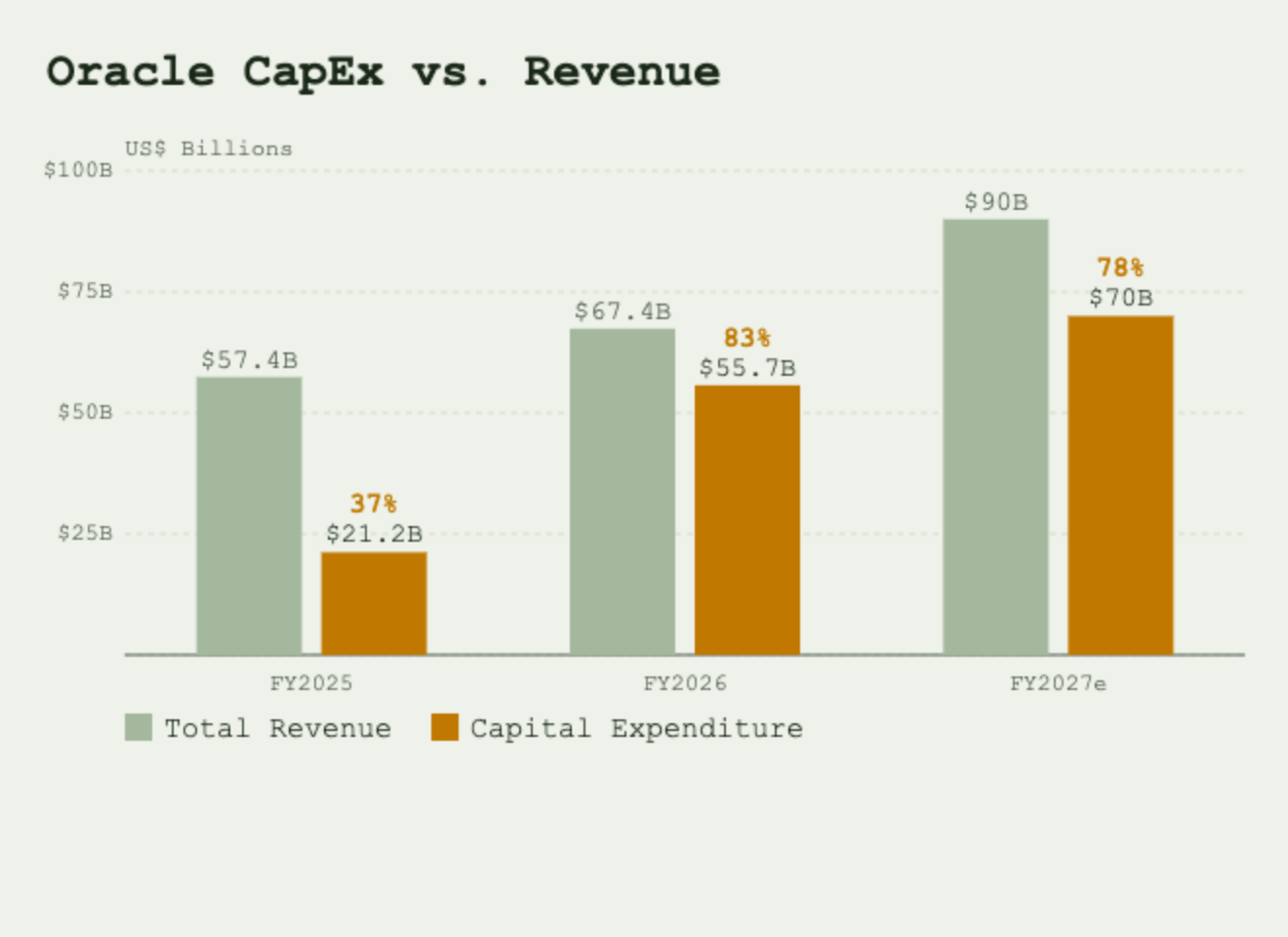

Oracle's Build-First Bet

- The Data: Oracle reported $55.7 billion in capex for FY2026 against $67.4 billion in full-year revenue—an 83% capex-to-revenue ratio, up from 37% the year prior. The company's CFO guided approximately $70 billion in net capex for FY2027 against revenue guidance of $90 billion, bringing the ratio down slightly to 78%. Free cash flow swung from near-zero in FY2025 to negative $23.7 billion in FY2026.

- The Takeaway: Oracle is growing cloud infrastructure at 77% annually, but the data centers required to fulfil a $638 billion backlog are consuming the entire operating cash flow and then some. What separates it from a speculative builder: customers have already committed to buying what is being built. The risk is timing. Depreciation nearly doubled from $3.9 billion to $7.6 billion last year—the income statement pressure from this construction cycle has barely started. The question is whether $638 billion in backlog converts to cash before debt begins to constrain its options.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.