SpaceX IPO Is the Ultimate Package Deal

Sign up for ARPU: Stay informed with our newsletter.

Programming note: we will return on Friday and take a look at Dell.

A Sentient Sun

If you read the prospectus for SpaceX's upcoming initial public offering, you will find a document that reads less like a standard S-1 and more like a syllabus for a graduate seminar in science fiction.

In it, SpaceX outlines an ambitious corporate mandate: launch 100 gigawatts of solar-powered orbital AI compute every year, establish a multiplanetary civilization, and scale humanity to a Kardashev Type II civilization. This builds on Musk's earlier, slightly more poetic remarks during the xAI merger announcement, where he declared the ultimate goal was to make a "sentient sun." For this, SpaceX is targeting a $1.8 trillion valuation—instantly making it one of the largest publicly traded entities on the planet.

The official pitch is that Earth has simply run out of juice. Terrestrial power grids cannot sustain the AI boom, meaning humanity's compute must migrate to the stars to control the "physical stack."

The company's prospectus explains the current power crisis:

On Earth, the massive expansion of data center capacity to support growing compute demand is significantly outpacing electricity generation, which was effectively flat in the United States for approximately 15 years, growing at a compound annual growth rate of 0.1% from 2008 to 2023...

We expect the gap between demand for compute and power supply to continue to widen meaningfully as AI compute needs proliferate...

The Sun contains approximately 99.8% of the solar system's energy and, as a result, we believe it is the only truly scalable solution to terrestrial energy constraints in the age of AI... Space-based solar arrays can generate more than five times the energy per unit area of terrestrial solar due to continuous illumination, lack of atmospheric interference, and optimal orientation.

It is a grand, sweeping narrative. It is also a remarkably clever exercise in corporate structuring.

While the sentient sun might be on the long-term roadmap, the immediate reality is a bit more down-to-earth: frontier AI is a famously capital-hungry sport, and consolidating a dominant rocket business with a fast-growing, cash-burning AI startup is an exceptionally elegant way to fund the server bills.

The Math of a Consolidation

To understand what is happening in the SpaceX IPO, you have to separate the business of physics from the business of AI.

The physics business is fantastic. SpaceX has established a clear, structural lead, accounting for over 80% of the world's mass to orbit since 2023. At the heart of its $18.7 billion annual revenue is Starlink, whose subscriber base surged from 2.3 million in 2023 to 8.9 million in 2025. This drove Starlink's operating income to $4.4 billion, supported by an orbital fleet 15 times the size of its nearest competitor.

To be sure, the launch segment is currently losing money—posting a $662 million operating loss in Q1 2026 as the company pours capital into Starship. But the business model relies on driving launch costs down to a projected $185 per kilogram. If SpaceX can actually hit that target, down from NASA's historical average of $18,500, it locks in a cost advantage that is highly difficult for competitors to match.

Then there is the AI business.

Earlier this year, SpaceX acquired xAI in an all-stock transaction that valued the AI arm at $250 billion. When you look at the S-1, the financial footprint of this acquisition is substantial. Last year, SpaceX's AI operations posted an operating loss of $6.4 billion. Capital expenditures nearly doubled to $20.7 billion, with more than half of that money allocated to the AI business.

The math here is straightforward. Competing in frontier AI requires endless capital. Google and Meta can afford to spend tens of billions of dollars on GPUs because they own digital cash-machines powered by targeted advertising. Musk does not have a high-margin search engine. He has X, a social network whose advertising revenue is not quite sized to fund a global AI arms race. So, he consolidated his capital-intensive AI startup with his cash-flowing rocket monopoly.

By merging xAI into SpaceX right before the IPO, Musk has bypassed the need to raise another round of venture capital for xAI. Instead, he is leveraging the immense popularity and dominant market position of his aerospace company to secure the necessary AI funding directly from public markets.

It's a package deal: if you want a piece of the world's only functional space logistics network, you also get to participate in the frontier AI race.

The Inverted Moonshot

There is a distinct irony to this arrangement.

A decade ago, the tech industry operated on a very specific economic model: you build a cheap, infinitely scalable software product (like a search engine), and you use the massive profits from that software to fund capital-intensive "moonshots" in the physical world (like self-driving cars or curing aging). The software subsidizes the hardware.

SpaceX has inverted this model.

Today, building LLMs is so expensive that literal moonshots—the physical act of launching rockets—have become the cash-generating engine tasked with supporting an AI product. It means that some of the world's most advanced aerospace engineering is currently being optimized to generate the cash flow needed to train a chatbot. It is, if nothing else, a remarkably roundabout way to fund the AI ambition.

The Physical Moat

This brings us to the ultimate comparison of the 2026 IPO cycle: SpaceX vs. OpenAI.

OpenAI is reportedly preparing its own public offering at a valuation approaching $1 trillion. But there is a fear that that LLMs will eventually become a commodity. OpenAI's ChatGPT is currently locked in a brutal margin war with Anthropic's Claude, Google's Gemini, and a flood of open-source models. OpenAI is selling software in a market where the barrier to entry is primarily capital.

SpaceX is selling infrastructure in a market where the barrier to entry is gravity. And execution. Jeff Bezos founded Blue Origin two years before SpaceX, yet its New Glenn rocket is still trying to find its footing, recently failing to orbit a communications satellite. Even Amazon, which is spending $11.6 billion on spectrum to build its own satellite network, is structurally disadvantaged from day one because it has to buy launches at retail prices. In space, if you do not own the shovel, you are just digging a very expensive hole.

The most revealing detail of the SpaceX IPO isn't the Mars colony timeline. It is the disclosure that Anthropic—OpenAI's fiercest rival—is paying SpaceX $1.25 billion a month for computing capacity.

This is a real moat. While OpenAI is fighting for chatbot subscriptions, SpaceX is positioning itself as a key infrastructure provider for the entire AI industry. It is using its massive launch capacity to build orbital data centers, and then renting that compute back to other frontier labs. Even if the consumer chatbot market remains highly competitive, SpaceX still collects rent on the physical infrastructure that powers the ecosystem.

Under the Hood

For investors, the SpaceX IPO is a bet on a one-man mandate. They may get access to the company's economics, but the votes stay with Musk. Under the proposed dual-class structure, Class B shares carry 10 votes to Class A's one, leaving Musk with 85.1% of the total voting power post-IPO. Public investors are being asked to provide up to $75 billion while receiving virtually zero governance in return.

Large public pensions have already raised alarms, pointing out that this lock gives Musk a permanent veto over his own firing, regardless of how the high-risk xAI integration turns out. Yet, in return for surrendering their voting rights, investors get equity in a company that controls the physical constraints of the launch market.

It is a steep entry fee, but in an era of intense software commoditization, backing an infrastructure giant where you have absolutely no say might just look like a reasonable cost of doing business.

Signal Stack

The operating reality beneath the headlines.

- Exploring a Space-Based, Scalable AI Infrastructure System Design (Google Research) - Lab tests show Trillium TPUs are surprisingly radiation-hard, and launch costs falling below $200/kg by the mid-2030s could make orbital compute cost-competitive with terrestrial data centers.

- Moonshot? Data Centers in Space (Natixis CIB) – At today's launch costs, an orbital gigawatt costs 4 times a terrestrial equivalent; the investment case only closes if launch prices, satellite lifespans, and chip efficiency all improve simultaneously.

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

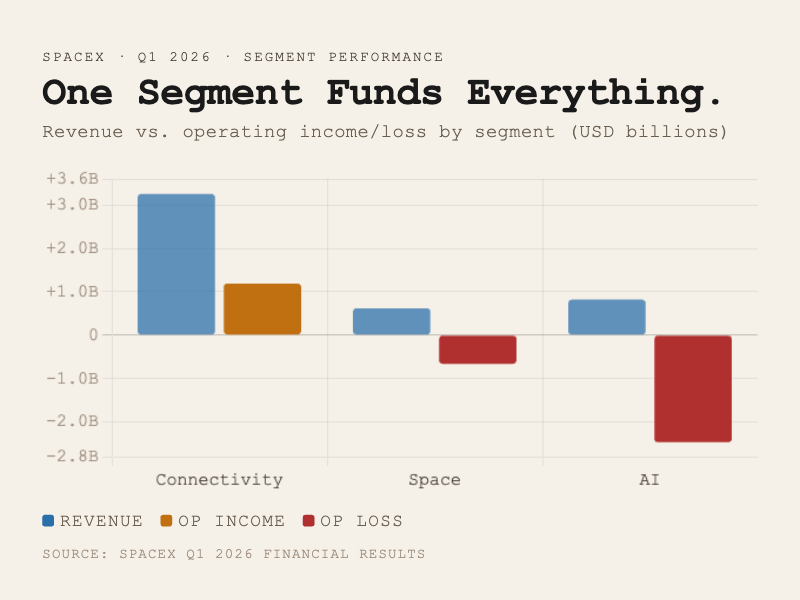

- The Data: SpaceX reported Q1 2026 results across three segments. Connectivity generated $3.3 billion in quarterly revenue with $1.2 billion in operating income. Space generated $619 million in revenue at a -$662 million operating loss. The AI segment generated $818 million in revenue at a -$2.5 billion operating loss—losing more than three dollars for every dollar it earns. The consolidated operating loss across all three businesses was -$1.9 billion.

- The Takeaway: There is one profitable business inside SpaceX, and it is a satellite internet provider. That business is currently subsidising both a rocket company and an AI operation. SpaceX's AI ambitions are being bankrolled by the monthly subscriptions of Starlink users in rural Montana. The boring, operational, cash-generating business is what makes the moonshot possible.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.