Finance Company in a Tech Trench Coat

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return on Tuesday and take a look at some Federal Reserve research on the impact of AI.

Neoclouds and the Return on Silicon

If you want to understand the sheer scale of the AI build-out, you have to look at a rapidly growing category of companies known as "neoclouds."

Neoclouds are independent compute providers that have stepped into the gap left by traditional hyperscalers. They are attracting billions of dollars in capital, and their growth rates are staggering.

On the back of that growth, venture capitalists and public markets are treating these companies like the next generation of foundational tech platforms. CoreWeave is currently valued at roughly 6x next twelve months (NTM) revenue, while IREN is trading at around 10x NTM revenue. Those are software multiples.

But there is just one problem with treating the neocloud cohort like software companies: for most of them, the product isn't code—it's capital.

The Leasing Loop

To understand what a neocloud actually is, you have to look at the financial plumbing. A neocloud raises a massive amount of debt. It uses that debt to buy tens of thousands of highly expensive Nvidia GPUs. It puts those GPUs inside a data center shell with heavy cooling infrastructure. Then, it rents that compute capacity out to a hyperscaler (like Microsoft) or an AI lab (like Anthropic).

As hedge fund manager Jim Chanos recently pointed out at a conference, this is not a new, revolutionary technology platform. It is an equipment leasing company.

In effect, if you are buying chips from Nvidia, renting data center space from somebody else, and then renting the chips out to Microsoft, Google, or Meta, you're an equipment leasing company. You're not a high-tech company; you're a finance company, in effect, making a bet on the life of the chips and what you can get over the contract.

Chanos noted a very telling detail about the neocloud ecosystem: look at who runs it. CoreWeave was founded by former hedge fund managers from Magnetar Capital. Blackstone, the private equity and real estate giant, is heavily involved in financing the space.

When private equity and credit funds flock to a sector, they are not there to write code. They are there to manage financial spread.

The Margin Trap

If you borrow debt to buy a heavy, depreciating physical asset and then lease it out to a corporate customer, you are in the exact same business as the guy who leases tractors to farmers or commercial airplanes to Delta Air Lines.

Equipment leasing is a perfectly fine business. It is necessary. It generates cash. But historically, it is a highly cyclical, capital-intensive business that commands single-digit returns on invested capital (ROIC) and trades at the valuation multiple of a mid-western bank.

High-growth software companies historically command 10x revenue multiples because code requires zero capital. Once you write it, you can sell it infinitely. Neoclouds, however, require massive capital to buy rapidly depreciating physical assets.

No one is pretending neoclouds are writing code. Yet the market is still willing to award them software-like valuation multiples, largely because the near-term cash flows are so spectacular. We are in the middle of such a severe compute shortage that the rental prices for even older GPUs are actually going up. AI labs are so desperate that they are locking up whatever capacity they can find, defying every normal law of semiconductor depreciation. When near-term revenue is exploding because of a supply shock, it is easy for investors to look past the heavy cost of the assets sitting on the balance sheet.

But even in the middle of this unprecedented, price-gouging gold rush, the underlying math of equipment leasing is unforgiving.

According to a McKinsey report, once you account for labor, power costs, and a standard five-to-six-year hardware depreciation schedule, the gross profit margins of a GPU rental business sit at roughly 14% to 16%. That is a lower margin profile than many brick-and-mortar retail stores.

Here is the napkin math of a neocloud: earning mid-teens margin on a massively expensive piece of physical hardware translates to a single-digit Return on Invested Capital (ROIC). As Jim Chanos argued, these rental deals are currently penciling out at 5% to 8% pre-tax returns. And that is before you pay the interest on the mountain of debt you had to raise to buy the chips in the first place.

This exposes the fragility of the neocloud boom. If a single-digit ROIC is the absolute best these companies can do during the greatest hardware supply shortage in tech history, what happens to those margins when supply finally catches up?

There is a reason Microsoft and Amazon are willing to rent capacity from neoclouds rather than putting all that silicon on their own balance sheets. By signing a three-year lease with a venture-backed startup, the hyperscalers get the immediate compute they need to satisfy their AI developers, but they keep some of that terrifying physical depreciation risk off their own books.

The neocloud boom is fascinating because it is a triumph of financial engineering disguised as a tech disruption. These companies have figured out how to finance the hardware required to build the future of AI. But pricing a capital-intensive, low-ROIC tractor-leasing business as if it were a high-margin software platform is the ultimate hallucination.

Signal Stack

The operating reality beneath the headlines.

- The Growing Compute Shortage (Apollo Global Management) – Scarcity is reviving assets once written off as obsolete: crypto miners already possess what hyperscalers need most — power, land, and grid connectivity — and are being repriced as AI infrastructure plays in a compute-constrained world where access to those inputs has become a competitive moat.

📺 On Our Channel

How Big Tech Is Running Out of Ways to Pay for AI

Over the past five years, Alphabet, Meta, and Microsoft collectively bought back more than $500 billion of their own stock. Meta paused buybacks in its most recent quarter while raising its capex outlook to $145 billion. Alphabet has moved to issue new equity. And behind them, OpenAI, and Anthropic are preparing to come to market. The stock market's biggest buyer is leaving. Its biggest sellers are arriving. We broke down what that reversal means for the household wealth that has been quietly supporting consumer spending for a decade.

Watch ARPU's deep dive on YouTube (12 Mins)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

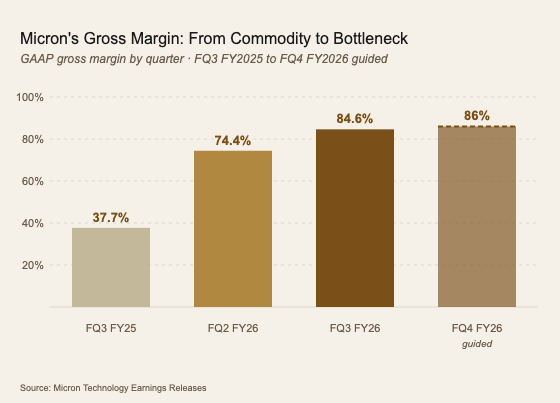

Micron's Commodity Moment

- The Data: Micron's GAAP gross margin expanded from 37.7% in FQ3 FY2025 to 84.6% in FQ3 FY2026—a 47-percentage-point swing in four quarters, with FQ4 guidance set at approximately 86%. Memory chips are a commodity business where margins are typically competed down toward cost over time. A gross margin approaching 85% on a commodity product is not operational efficiency. It is scarcity pricing.

- The Takeaway: AI data centers require high-bandwidth memory produced by only three companies worldwide, and hyperscaler demand is structurally outrunning production capacity. Micron's margin expansion is the clearest single financial measure of what that constraint looks like on an income statement — a commodity supplier repriced into a strategic bottleneck in the span of one fiscal year.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.