The 3:1 Math of Memory Scarcity

Sign up for ARPU: Stay informed with our newsletter.

Programming note: ARPU will return this Friday with a look at how Berkshire Hathaway thinks about AI.

Vendor Financing in Reverse

Normally, when a company wants to buy a component, it issues a purchase order. When it really wants to buy a component, it signs a long-term agreement.

When it is a multi-trillion-dollar tech giant caught in the middle of an AI arms race, it apparently just offers to buy the factory.

According to a phenomenal scoop from Reuters last week, the memory chip shortage has gotten so bad that major tech firms are aggressively courting SK Hynix with offers that have no precedent in the industry. They are not just submitting purchase orders for chips. They are offering to fund entire production lines. They are offering to buy SK Hynix its own extreme ultraviolet (EUV) lithography machines—the crown jewels of semiconductor manufacturing, made by Dutch firm ASML for upwards of $300 million a pop—just to guarantee a spot at the front of the line.

In the normal economy, vendors occasionally offer financing to their customers to help them buy a product. What is happening in the AI supply chain right now is vendor financing in reverse.

The demand for high-bandwidth memory (HBM) is so inelastic, and the supply is so constrained, that the most powerful companies in the world are acting as private banks for their own suppliers.

And the best part of the Reuters report is that SK Hynix is hesitant to accept the money. There are two reasons for this. The first is a strategic flex: the South Korean memory giant is flush with cash and doesn't want to become hostage to a specific hyperscaler or be forced into offering a bulk discount. The second is a physical reality: even if they wanted the money, they have nothing left to sell. As one source told Reuters: "Regardless of the type of offer, available capacity is essentially zero right now. There isn't even a small portion that can be designated for a specific customer."

When a customer offers to buy you a $300 million manufacturing tool and you tell them you will have to think about it, you are no longer operating in a commodity business. You are operating a chokepoint.

The Math Behind the Shortage

To understand why the world's largest technology companies are acting as capital providers for their own suppliers, you have to understand the industrial arithmetic happening inside the fabs.

The official story is that AI requires a lot of memory. True, but incomplete. The deeper bottleneck is the physical cost of producing the right kind of memory.

Micron CEO Sanjay Mehrotra recently described this to investors as the 3-to-1 trade ratio.

HBM is a complex piece of hardware. It requires stacking multiple chips on top of each other and connecting them with microscopic vias. That architecture is what gives HBM its enormous bandwidth advantage. But from a manufacturing perspective, it is also painfully capacity-intensive.

According to Micron, HBM carries roughly a 3-to-1 capacity trade-off versus standard DDR5 memory: adding HBM output consumes about three times the DRAM manufacturing capacity that would otherwise support comparable DDR5 production. And as HBM gets more advanced, that trade-off only gets worse.

That is the part the "AI needs more memory" story misses. Cleanroom space is a zero-sum game. There is no version of this where everyone wins. Every time a memory maker allocates factory capacity to build high-margin HBM for an Nvidia GPU, it is physically displacing the capacity needed to make standard memory for traditional servers, laptops, and phones.

The AI buildout is not just competing with consumer electronics for memory. It is cannibalising the manufacturing lines that produce it. The shortage is not a temporary demand spike. It is an architectural consequence of what HBM actually costs to make.

This is also why the shortage cannot be solved quickly. Memory fabs take years to build. The three companies that control roughly 90% of the global DRAM market—Samsung, SK Hynix, and Micron—are all expanding capacity, but analysts expect meaningful relief no earlier than 2028. SK Hynix has said the shortage continues to 2030. The fabs they are building now are, in a very literal sense, the only answer. There is no shortcut.

The Balance Sheet Moat

When the physical supply of a critical component shrinks, procurement stops being a supply-chain function and starts being a competitive weapon.

If you listen to the recent earnings calls of the AI "haves"—the hyperscalers and the elite silicon designers like Nvidia and Broadcom—they are operating with a terrifying level of confidence. They are using their massive cash piles to bypass the spot market entirely.

Here is Broadcom CEO Hock Tan, explaining his competitive advantage during an earnings call:

We provide multi-year supply agreements as our customers scale up deployment of their compute infrastructure. Our ability to assure supply in these times of constrained capacity in leading-edge wafers, in High-Bandwidth Memory, and substrates ensures the durability of our partnerships, and we have fully secured capacity of these components for 2026 through 2028.

Broadcom is telling the world that the allocation of advanced memory through the end of the decade is largely settled, and they are inside it. They have visibility because they purchased the visibility. In the current environment, a secured allocation is worth more than a purchase order, and Broadcom has the former while much of the market is scrambling for the latter.

The Spot Market Bloodbath

Then there are the "have-nots."

If you do not have the balance sheet to prepay for a factory, you are forced to buy your memory in the spot market. And the spot market is currently a bloodbath.

Just look at Dell Technologies. On their Q3 earnings call, Dell's leadership sounded like they had things under control, explicitly describing a "deflationary" commodity environment. Fast forward three months, and Dell COO Jeff Clarke delivered a very different message on the Q4 call:

The spot market for a gigabit of DRAM, over the last 5, 6 months is up nearly 5.5 times. If you look at NAND, the cost is $0.20 a gigabyte, that's up nearly 4 times over the last 6 months. The industry analysts have Q2 up over Q1 in a range of 20%-50%. They have Q3, 5%-15%. Q4, 5%-10%. Those are estimates. Those are probably in ballparks where things are.

Dell walked into a market that changed faster than any quarterly planning cycle was designed to handle. Super Micro Computer reported that memory and SSD prices more than tripled in a six-month window. Cisco explicitly blamed higher memory costs for squeezing its product gross margins. These are not small companies with thin procurement operations — they are among the largest technology hardware businesses in the world, and the spot market hit them anyway.

This dynamic is already bleeding into the consumer market. The Guardian recently noted that "RAMageddon" is spelling the end of the cheap laptop and the budget smartphone. HP and Lenovo are warning that PC unit sales will face pressure as component costs skyrocket. Apple, Microsoft, and Sony have all quietly raised prices or phased out their lower-memory base models.

This is the ultimate downstream effect of the 3:1 trade ratio. The hyperscalers are effectively taxing the entire consumer electronics market to fund their AI infrastructure. The cost of building Mark Zuckerberg's super-brain is being paid not just by Meta's shareholders, but by anyone trying to buy a PlayStation 5 or a $500 Chromebook.

The tech industry has effectively split in two. There are the companies that can afford to buy the ASML machines for their suppliers, and there are the companies left fighting over the scraps. In the AI economy, the ultimate competitive moat isn't software. It's the ability to write a blank check.

Related reading:

- AI Tailwinds and Memory Shortages (Nasdaq)

- Global Memory Shortage Crisis (IDC Global)

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech.

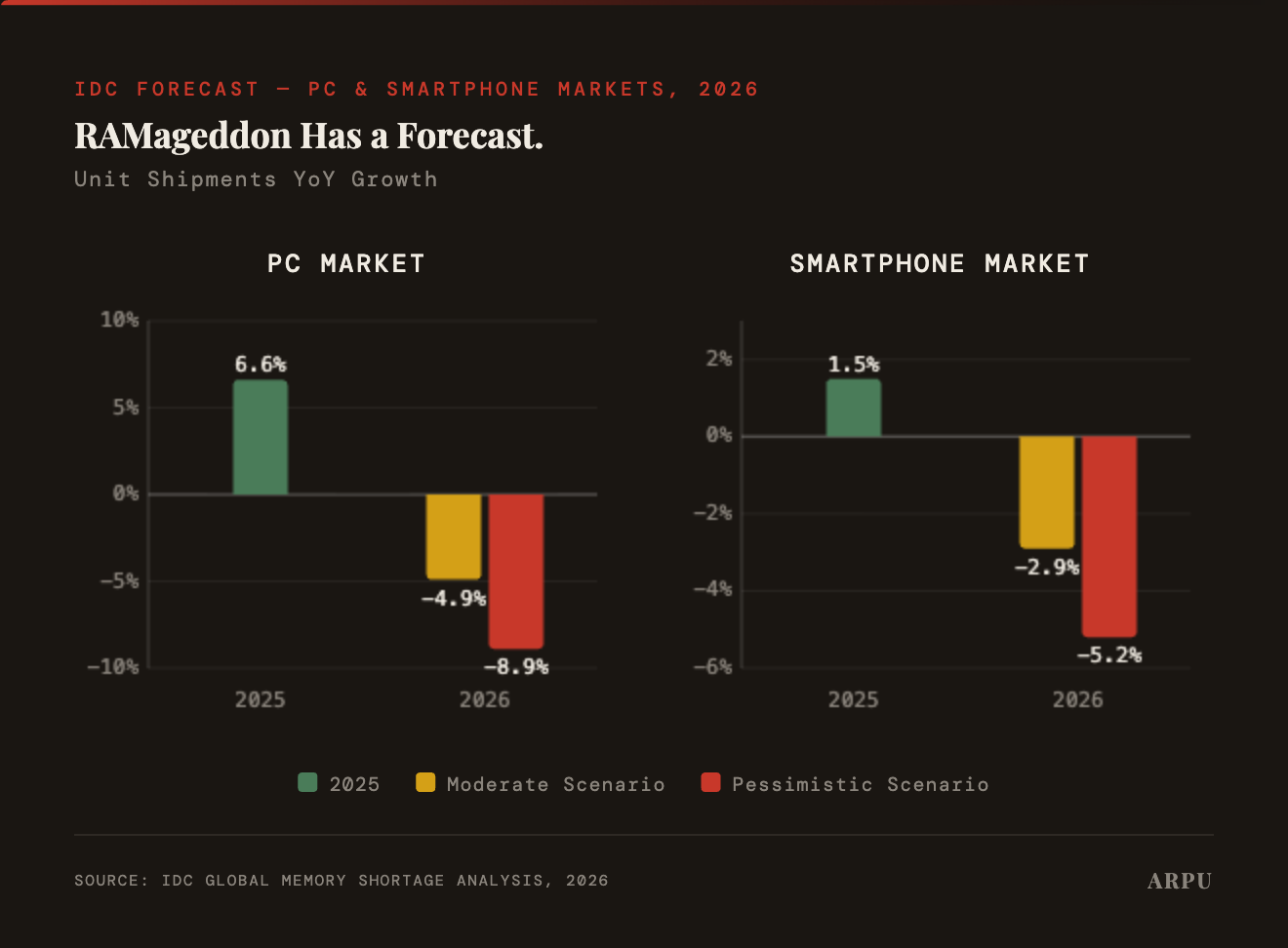

- The Data: The PC market is forecast to contract in 2026: 4.9% in the moderate case and 8.9% in the pessimistic case. The smartphone market faces a similar contraction of 2.9% to 5.2%. Both markets expect average selling price increases of 4–8% on top of the volume declines, as manufacturers pass rising memory costs to consumers.

- The Takeaway: The PC pessimistic scenario represents a 15 percentage point swing from 2025's growth — not because demand collapsed, but because the memory needed to build devices has been reallocated to AI data centres. IDC expects DRAM and NAND supply growth to run below historical norms through 2026, and new fab capacity will not arrive before 2027 at the earliest. The consumer electronics market is, in effect, subsidizing the AI infrastructure build-out.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.