Spotify: Product, Business Model, Competitors

Sign up for ARPU: Stay informed with our newsletter.

In this week’s business review, we will look at Spotify by unpacking its trajectory, its go-to-market strategy, and key financial metrics. We will also look at the competitive landscape, the company’s major acquisitions and what could be next for this popular streaming service.

Without further ado, let’s dive in!

Founding history

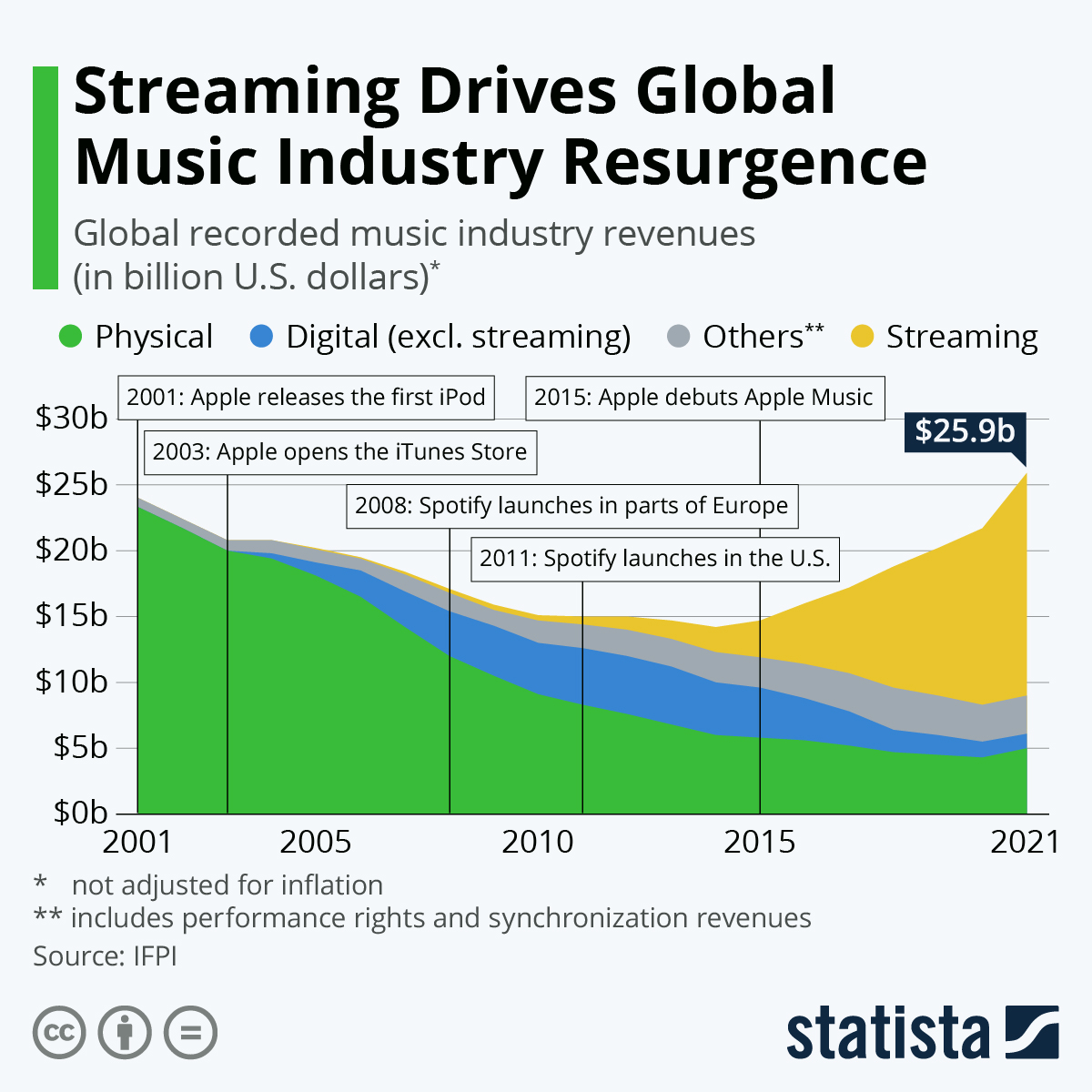

Music consumption went through five major medium changes and each propelled profound changes in the music industry. The invention of the phonograph by Thomas Edison allowed music lovers to move away from the live-only experience and gave birth to the record industry. The change from vinyl to CD which occurred in the 1980s led to a major industry consolidation with three record labels (Warner Music, Universal Music Group and Sony) gaining a stronghold on the industry.

In the early days of the internet, online piracy, as epitomized by the rise and fall of Napster, became the dominant practice. As a result, US music industry revenues were cut in half.

The tide has only turned when the access-based model of streaming music on demand took off. It allowed users not to rely on radio’s linear distribution of a limited song selection and to stop buying and owning music. In 2015, following more than a decade of declines, the global recorded music business reached a digital inflection point. Since then, music industry revenue increased steadily at single digits each year. Streaming accounts for well over a half of this revenue.

Spotify is an early pioneer of streaming and one of the world’s most popular audio streaming subscription services. It was born as a response to piracy, out of a single assumption that music fans would be willing to pay for a legal service, if the experience was frictionless.

In 2006, two successful Swedish entrepreneurs wanted to start a project they would care about. Daniel Ek, a computer prodigy, sold his ad-tech business to Martin Lorentzon’s sprawling affiliate marketing company, TradeDoubler and managed to persuade Lorentzon to leave his company and start Spotify.

At the height of the economic crisis, Ek gathered a few engineers in a small flat above a coffee shop and went on a mission to secure global licences from major record labels. Following many rejections and two years with no income, he narrowed his focus on Europe. When he finally loaded a Spotify demo with pirated tracks for label executives to try it for themselves, things started picking up.

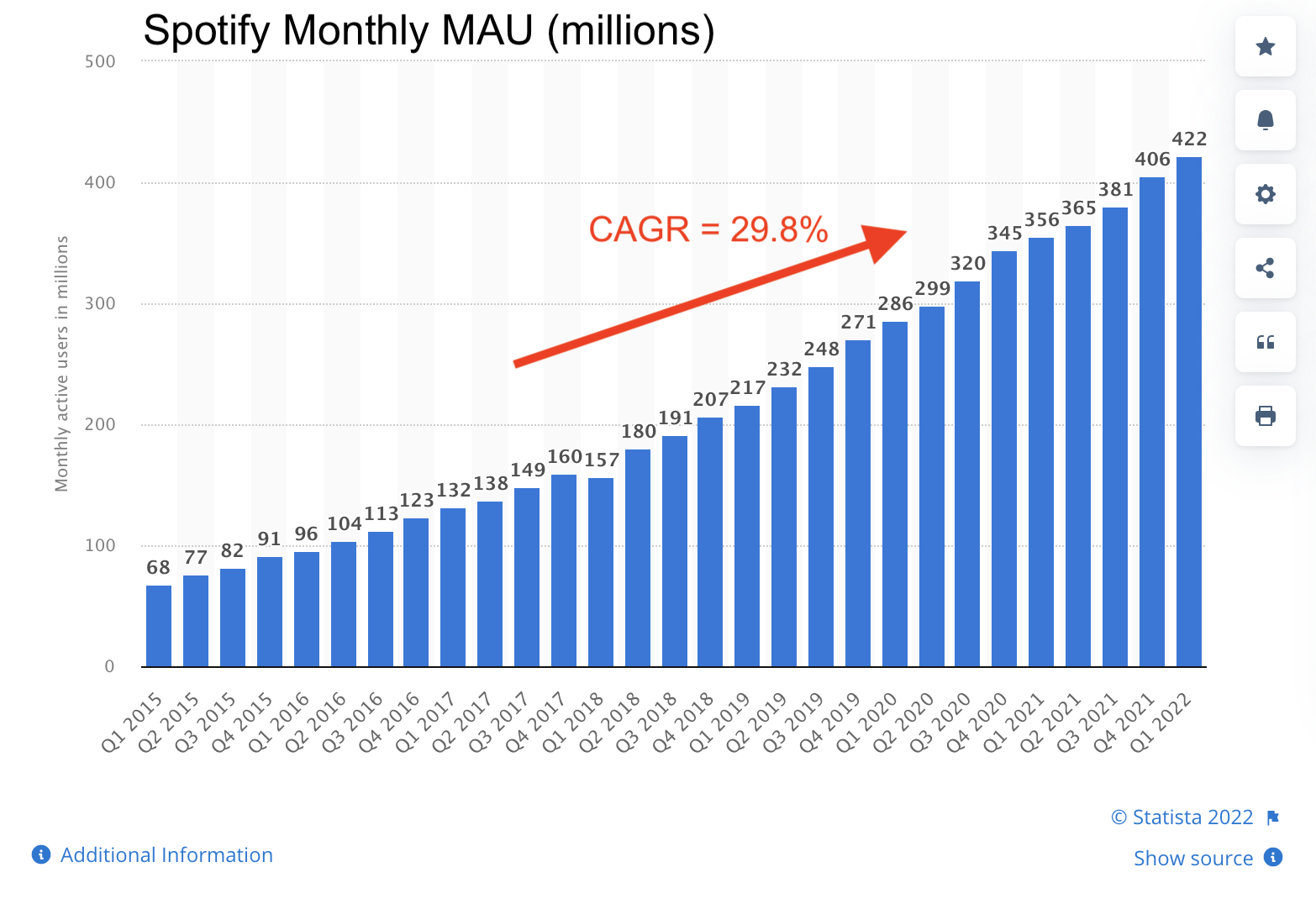

In October 2008, Spotify went live, by invitation only, in Scandinavia, the UK, France and Spain. In July 2011, it officially launched in the US. Just two months later, it has 2 million paid subs and has been growing since.

In February 2018, Spotify went public in a direct listing without raising additional funds. Today, the company is valued at around $20 billion. It has over 422 million MAUs, including 182 million paying subscribers with access to 82 million tracks, including more than 3.6 million podcast titles. In 2021 alone, Spotify’s audience streamed 110 billion hours of content.

The first product

Gustav Söderström, Spotify’s Chief R&D Officer rightly compared the company’s early product to Skype. It wasn’t a completely novel idea but it was faster, easier to use and more social than others.

It was clear early on that Spotify was not selling a unique product. It also did not own the content it was providing access to. So, the company had to ensure the best user experience in order to attract the most consumers. Ek’s early mantra was to make Spotify “like water”. He was very focused on reducing the response time, so that the human brain could perceive it as instant. Spotify was able to play songs within 285 milliseconds.

Some of the early Spotify enthusiasts included Mark Zuckerberg, Sean Parker and Barack Obama.

Go-to-market motion

Spotify was able to achieve scale by utilizing a freemium model. It acquires customers primarily through their ad-supported service which has no subscription fees and provides users with limited on-demand online access to music and unlimited online access to podcasts on multiple devices. 60% of Spotify’s paying subs start out using the ad-supported option.

Spotify also offers a variety of subscription pricing plans for the premium service, so that users across demographics, age groups and lifestyles can have access to it. For example, the family plan allows up to six accounts, while the student plan is bundled with other services and costs half the normal price.

Spotify’s pricing is also adapted to local markets and takes into account consumer purchasing power. So the same service that costs $10/month in the US, costs $2.4/month in the Philippines. While these price variations allow for robust MAU growth, they also have a direct impact on the company’s premium ARPU which is around half the standard US $10/month fee.

You can see from the chart and table below that the ARPU for Spotify steadily declines as Spotify expands internationally.

Source: Business of Apps, company data

Evolution of the company

As the company evolved, it continued to focus on enhancing the consumer experience. It added free streaming on mobile devices in 2013, followed by matching music with the listener’s running pace and integrating mood- and time-based playlists into the service. It also expanded its so-called discovery business by leveraging listening data to guide customers to content they would not otherwise find.

Secondly, streaming meant that the understanding of consumer behavior no longer ended at the point of sale. As Spotify gathered vast data on who listens to what, when and where, it could open the pathway to the so-called two-sided marketplace by providing creators with analytics and tools that help them better understand their fans and enhance their monetization capabilities.

Finally, Spotify is very clear about its ambition to become a leading figure in podcasting. It actively invests in podcasts and other forms of spoken word content and is determined to make such content exclusive to Spotify’s platform through direct ownership or licensing arrangements, so that the service is differentiated, attracts more users and enhances engagement.

This strategy is best exemplified by exclusive licensing of the Joe Rogan Experience, the acquisition of three podcast studios, the Ringer, Gimlet Media and Parcast and promoting Bill Simmons to the global head of sports content and managing director for the Ringer (which Ek recently anointed as the next ESPN).

Financials

Spotify derives revenue from:

- the sale of the premium service directly to end users or through partners who bundle the subscription with their own services or collect payment for the stand-alone subscriptions from their end customers;

- the sale of display, audio, and video advertising delivered through advertising impressions across music and podcast content;

- arrangements with certain advertising automated exchanges, internal self-serve, and advertising marketplace platforms to distribute advertising inventory for purchase.

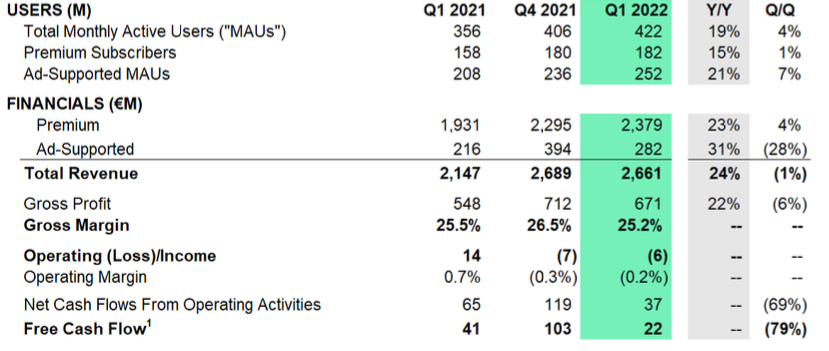

In 2021, total revenue reached €9.7 billion. Premium revenue increased by 19% relative to the prior year and amounted to €8.5 billion. It comprised 88% of total revenue (down from 91% in 2020). The increase was attributable primarily to a 16% increase in premium subscribers. In the last quarter, premium revenue grew 23% year-over-year to €2.4 billion.

For 2021, premium ARPU equaled €4.29, which was relatively flat relative to the preceding fiscal year. However, in the last quarter, it was up 6% year-over-year, amounting to €4.38 due to price increases and a favorable product mix shift.

In the last quarter, premium subscribers grew from 180 million to 182 million, for a 15% increase year-over-year. Interestingly, the churn of approximately 1.5 million subscribers stemming from Spotify’s exit from Russia, was offset by outperformance in Latin America and Europe.

For 2021, ad-supported revenue increased by €463 million or 62% and amounted to €1.2 billion. It comprised 12% of total revenue (up from 9% in 2020). This increase was primarily due to growth in music impressions sold and the growth in CPMs. Ad sales from the self-serve platform, podcast ad sales from The Ringer, and exclusive licensing of the Joe Rogan Experience also contributed to the increase in revenue during the year.

Last quarter was the largest ever for ad-supported revenue, as it grew 31% year-over-year to €282 million. It benefitted from podcast revenue strength, an increase in impressions, and a double-digit growth in CPMs.

Spotify is currently in 184 countries and territories. It has launched in over 80 new markets across Asia, Africa, the Caribbean, Europe, and Latin America in 2021.

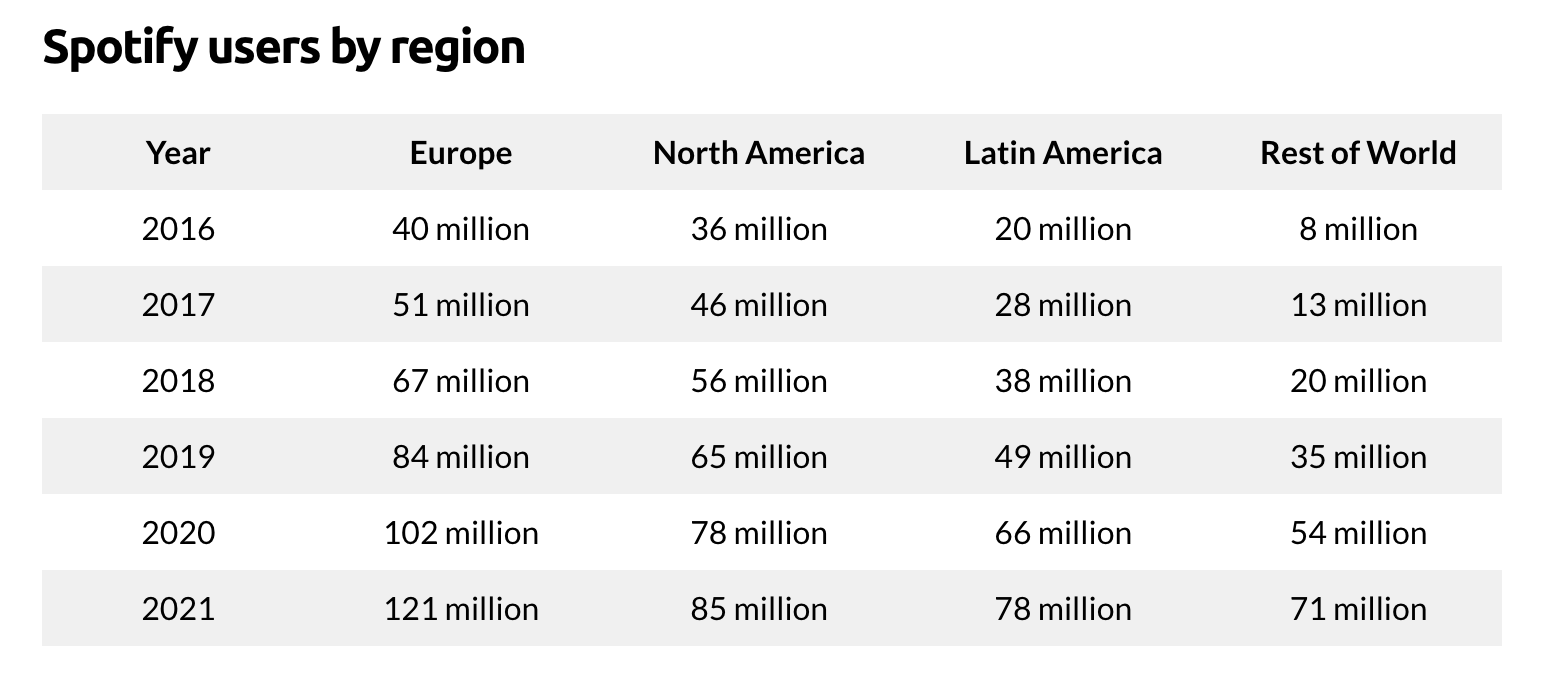

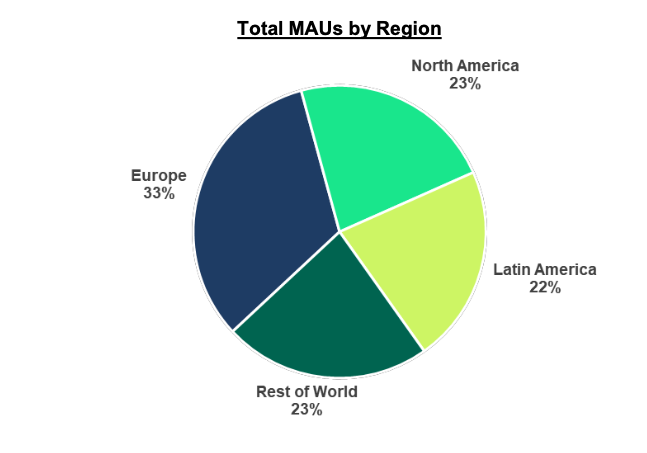

On a geographic basis, all four major regions are growing.

Europe is Spotify’s largest region. It accounts for 33% of total MAUs. Last year, it grew by 14%. The North America region accounts for 23% of MAUs and grew by 11% last year. Latin America amounts to 22% of MAUs and grew by 15% last year. The rest of the world has 23% of MAUs and grew the most by 35% in 2021.

In the last quarter, total MAUs grew 19% year-over-year to 422 million. The business benefited from outperformance in Latin America, Indonesia, Brazil, and Mexico. MAU growth was particularly strong in the Gen Z audience.

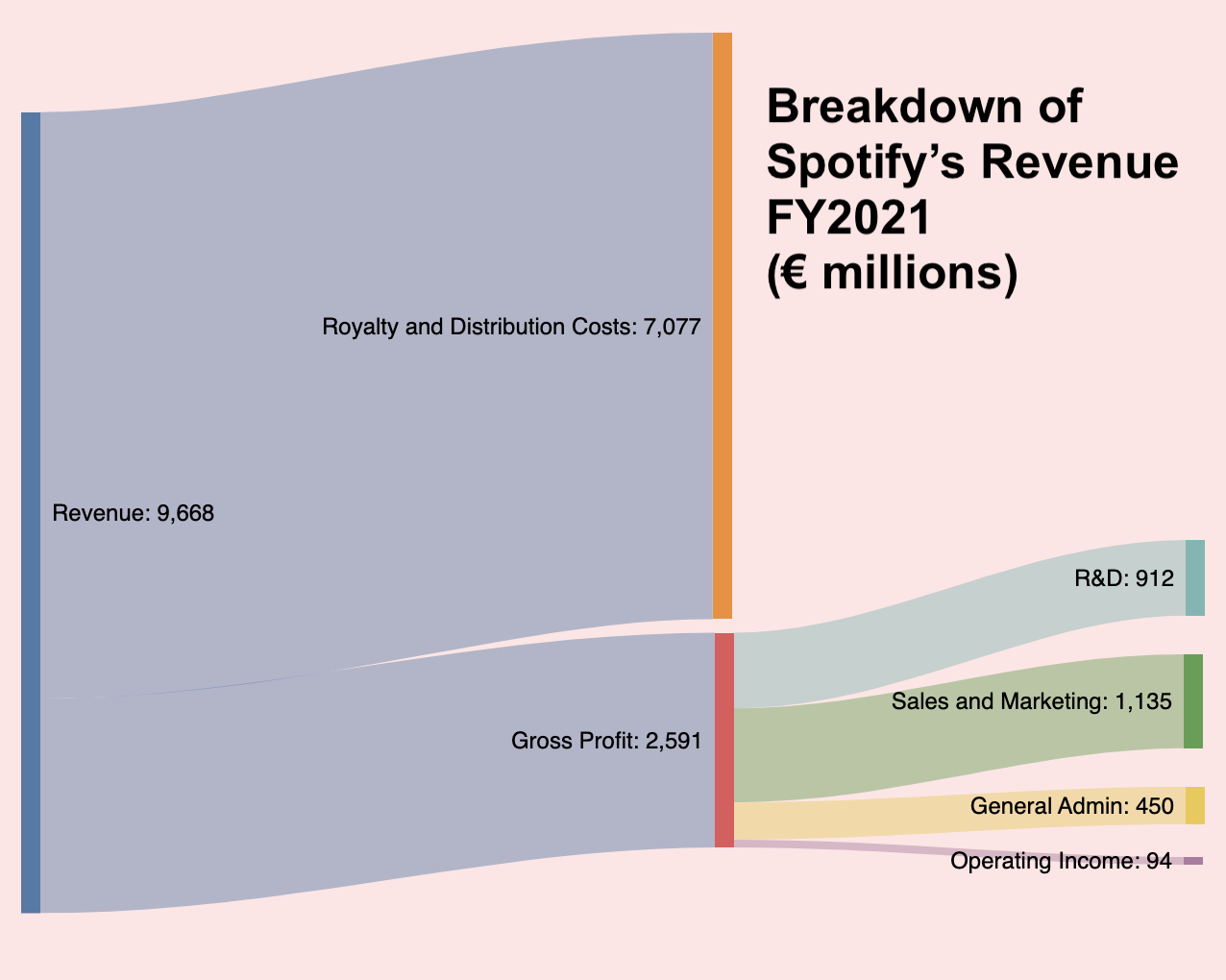

Given that Spotify does not own the music it sells access to, it has to pay hefty sums to the record labels that control Spotify’s music catalog (primarily UMG, Sony, Warner and Merlin). In 2021 alone, it had to pay $7bn in royalties to them. As a result, it is a low-margin business.

In the last quarter, gross margin amounted to 25.2% which was down 29 bps year-over-year. Favorable revenue mix shift towards podcasts and growing marketplace activity were offset by increased non-music content spend and investments in music product enhancements. Interestingly, premium gross margin was 28.4% and ad-supported gross margin was (1.5)% as all content costs related to podcast investment are included here.

Their gross margin is relatively low for a technology company because a lion share of the revenue goes towards paying licenses, royalty and distribution, as the diagram below illustrates.

In the last three months, free cash flow amounted to €22 million, down by €19 million primarily due to higher licensor payments. Last year, Spotify made just €94 million in operating income on €9.7 billion in revenue. However, Spotify has €3.6 billion in cash on its balance sheet.

Acquisitions

Ever since Spotify made its first acquisition of Tunigo (an app for finding, creating and sharing new music and playlists) in March 2013, it has been very prolific in the M&A space. A year later, it acquired The Echo Nest, which specialized in using machine learning to make music recommendations and generate playlists.

Since then, Spotify’s acquisitive history can be divided into two buckets.

From 2015 to 2019, it has acquired several companies with a cross-cutting theme of enhancing the user experience on the platform. These included buying Seed Scientific which was a data science consulting and analytics company, Cord Project and Soundwave which were social and messaging startups, CrowdAlbum which collected photos and videos of performances shared on social networks, Preact which was a cloud-based platform designed to reduce churn, and Sonalytic, an audio detection startup.

Spotify also acquired MightyTV, which connected it to television streaming services and recommended content to users. It also bought Mediachain, a decentralized database system for managing attribution, Niland designed to improve personalisation and recommendation features for users, and Soundtrap, an online music studio startup.

Since 2019, Spotify made most acquisitions with the goal of becoming a leader in podcasting. These included Anchor FM, a software company that enables users to create and distribute podcasts, Gimlet Media, an independent producer of podcast content, Cutler Media a storytelling podcast studio, and Bill Simmons Media Group, a creator of sports, entertainment, and pop culture content.

Further purchases included Megaphone LLC, a podcast technology company, Betty Labs Incorporated, a creator of interactive live sports experiences, and Podz, a technology company focused on the podcast discovery experience. Spotify also purchased exclusive licensing of the Joe Rogan Experience. In the last quarter, it acquired Podsights, an advertising measurement service and Chartable, a podcast analytics platform.

Competition

Since Spotify is selling access to the same music catalog as Apple, Amazon, Google and several others and its product is similar to its competitors, the company faces robust and rapidly evolving competition in all aspects of its business.

The competition plays out on multiple fronts, including the quality of experience, ease of use, relevance, accessibility, diversity of content and perception of advertising load.

Companies also compete on price (Spotify’s premium price has not changed since launching in the US), brand awareness, reputation, presence and visibility. Companies in this space also race to attract and retain software engineers, designers, and product managers.

Spotify goes against established and emerging competitors and the field is crowded.

More specifically, it competes with digital music streaming providers, such as Apple Music, YouTube Music, Amazon Music, Deezer, Joox, Pandora, and SoundCloud.

Other competitors include internet, terrestrial and satellite radio, podcast streaming providers, podcast creation and hosting platforms, live talk audio content providers and companies that offer advertising inventory and opportunities.

What’s next

The company added 2 million subs in the first three months of the year, even though it exited Russia and had to face protests over podcaster Joe Rogan and misinformation regarding COVID-19. Spotify predicts it would add 5 million users in Q2, despite an additional loss of 600,000 subs in Russia.

The company also continues to invest in core platform capabilities which are multi-year investments to enable a constant iteration across products, tools and services.

Spotify recently announced it will be available on an Ikea Vappeby Speaker lamp, the first Bluetooth speaker on the market to come with a Spotify tap. New Porsches will come equipped with an infotainment system that streams Spotify as an audio source and the company will also become the official audio streaming partner of FC Barcelona.

In Q1 alone, Spotify ran almost 2,000 experiments. Some led to full global product launches. For example, during a recent Blend campaign, 22 million users created Blend playlists in the first 20 days. Spotify also observed that over 60% of streams come from Gen Z listeners. The independent-to-major record label ratio is also changing, with independents growing faster than majors as the share of overall streaming on Spotify.

But most importantly, Spotify is doubling down on the podcast business with more than 1,150 original and exclusive shows on the platform and claims that podcast consumption is strong and increasingly sticky.

In terms of the outlook for Q2, Spotify sees total MAUs reaching 428 million, premium subs amounting to 187 million, with total revenue of 2.8 billion, and a gross margin of 25.2 %.

To showcase confidence in the future of the business, Daniel Ek recently wrote on Twitter:

I’ve always been vocal about my strong belief in Spotify and what we are building. So I am putting that belief into action this week by investing $50M in $SPOT. I believe our best days are ahead...

— Daniel Ek (@eldsjal) May 6, 2022

I hope you enjoy this article! Hit the button below to have insights and stories like this delivered to your inbox!