Netflix: A Content Arms Race For The Belt-Tightening Era

Sign up for ARPU: Stay informed with our newsletter.

In this article, we will do a deep dive on Netflix. If you like this article and would like to receive insights on tech companies in your inbox, please consider subscribing to our newsletter.

Marc Randolph, the co-founder of Netflix called his memoir “That Will Never Work”.

The title was meant as a defiant pronouncement of triumph, as the early doubters, who often uttered the phrase when Randolph would pitch business proposals to them, ranging from personalized shampoo to renting VHS tapes online, were finally proven wrong.

His thesis in the book was that viable business ideas do not descend upon clairvoyant entrepreneurs during divine-like moments of epiphany.

But rather that the ability to come up with hundreds of terrible ideas to find one that has the potential to work, followed by grit, iteration, improvement and practical orientation can finally lead to ultimate success.

On 17 September 2019, when the book was released, Netflix had a market cap of $130 billion which more than doubled in the next two years.

Time was ripe for victory laps and the insertion of a narrative around Netflix’s origin into mainstream awareness.

And yet, in the last quarter things started to crack.

Netflix lost 1 million subscribers, registering a first drop in a decade (although it also anticipates to gain 1 million subs in the next quarter).

As the company’s content spend obligations hover at $22 billion, while the actual runway to keep growing users against it appears to be ending, some argue that the memoir’s title can be a self-fulfilling prophecy.

Many skeptics have now come to the fore to proclaim that the streaming industry will never be able to generate profits resembling those of television and film groups during the linear era, as the pricing required to duplicate cable economics is colossal.

Morgan Stanley’s analysts went so far as to claim that there are reasons to doubt whether “there is a pot of gold at the end of the streaming rainbow”.

So in this deep dive, we will look at the history and evolution of Netflix, the company’s fundamentals, its current woes, the competitive landscape and what could be next for the world’s largest streaming service.

Founding History

Netflix’s origin story, which is circulated for marketing purposes, declares that Reed Hastings, the company’s second co-founder, was charged a $40 late fee for not returning his Apollo 13 tape to Blockbuster.

From sheer embarrassment, he thought of Netflix and a subscription based model, as a remedy for late fees.

But the story is slightly more complicated than this.

Prior to founding Netflix, Reed owned Pure Atria, a company that made software development tools. It bought Integrity QA, a 9-person startup developing automated software testing products that Marc Randolph helped build.

Following the merger, Hastings agreed for Pure Atria to be acquired for $700 million in the largest Silicon Valley deal of the time.

The acquisition would make both Hastings, Randolph and two other employees the latter brought with him redundant.

As the countdown to the deal began, Randolph had no duties of his own. He was growing increasingly bored and, in addition, felt responsible for the two protégées that followed him, only to face a prospect of becoming jobless

He often recalled how his father, who was a successful Wall Street financier, descended to his basement every day after work to build miniature steam-powered trains

It was clear to him that, despite attaining financial success, his father lacked the ability to build things and solve his own problems at work.

“A piece of advice” the banker once told young Randolph. “If you really want to build an estate, own your own business. Control your own life”.

Even if the message was too complicated to comprehend at the time, it made a mark on Randolph’s psyche.

So he started to wonder what it would be like to build a business from the ground up.

In the months leading up to the merger, Randolph and Hastings would drive over the Santa Cruz mountains to Sunnyvale to work together.

On these rides, Randolph would pitch various business ideas that Hastings quickly rejected, claiming they were not scalable.

Hastings insisted that the key to success was to sell a dozen products with the same amount of effort as selling one.

Randolph was slowly getting discouraged.

But one night, after watching Aladdin with his three-year-old daughter, he came up with the idea of renting VHS tapes online.

However, tapes were very expensive, clunky, fragile and difficult to ship.

After running the numbers, it quickly became clear that the operation stood no chance of being profitable.

However, shortly after DVDs came to the market, the idea of an online rental business, transposed onto the new medium looked attractive.

Once the entrepreneurs sent a CD in a regular envelope to Hastings’ house and it arrived intact the next day, Netflix was born.

The company launched on 14 April 1998 in Scotts Valley, California at 9 a.m. with a library of approximately 900 titles

Within 15 minutes, the website crashed due to the volume of orders which totalled 137 on the first day.

Randolph was responsible for designing the user interface and constantly tested different versions to perfect the experience.

The data generated from these tests, eventually led to the creation of Netflix’s successful business model.

It comprised three elements:

- a subscription-based service for unlimited access to DVDs with no due dates or late fees,

- a “Queue” allowing subscribers to specify the order in which they would like DVDs to be mailed to them, and

- an automated delivery system mailing out a DVD, after the previous rental was returned.

The subscriber data fed a recommendation engine known as “Cinematch” which helped manage the inventory and guided subscribers to DVDs that were in stock.

Evolution

As the company progressed, it went through four distinct chapters.

The first encompassed the growth of the DVD rental business which spanned a dot-com era crash, the 2003 IPO at $15 a share, Randolph’s departure from Netflix and the company attaining 6.3 million subscribers.

The second chapter started in 2007, when Netflix started transitioning to streaming, launching a new format by offering subscribers access to pre-existing movies and licensed TV shows and positioned as the ultimate disrupter with the ability to liberate viewers from the rigidity and costs of linear TV and premium cable.

The third chapter began around 2012, when the company started developing its own content.

Not only was it able to score an early hit with the Washington political drama House of Cards but it also upended the traditional model of releasing episodes week by week, by giving access to the entire series all at once, giving birth to an era of binge-watching.

The fourth chapter came with intense international expansion. The company moved to 190 countries, reached 222 million subscribers, poured tens of billions of dollars into worldwide content production and developed many popular shows outside the US.

It is now available worldwide with the exception of Mainland China, Syria, North Korea, and Russia.

Financials

Netflix at a glance (FY2021):

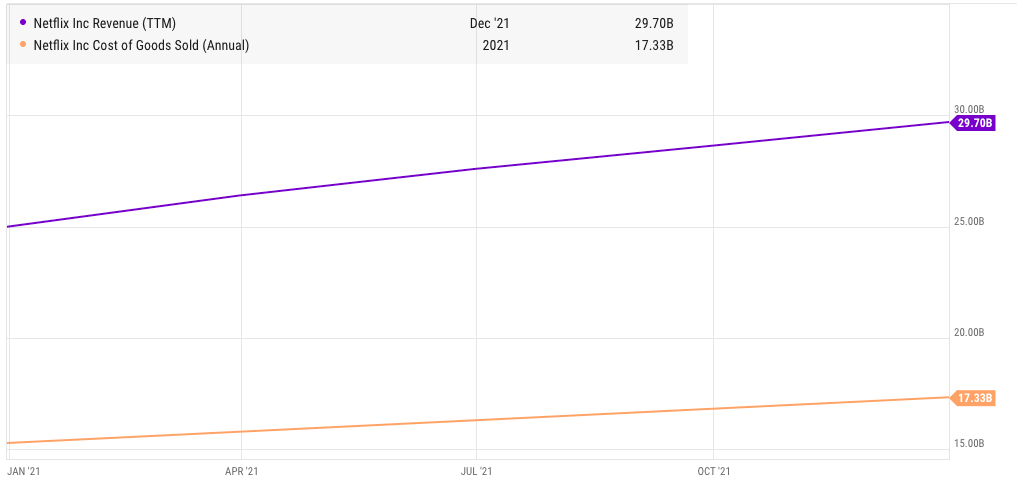

Revenue: $29.7 billion

EPS: $11.24

Cost of Revenue: $17.33 billion

Average Growth Rate: +26.38%

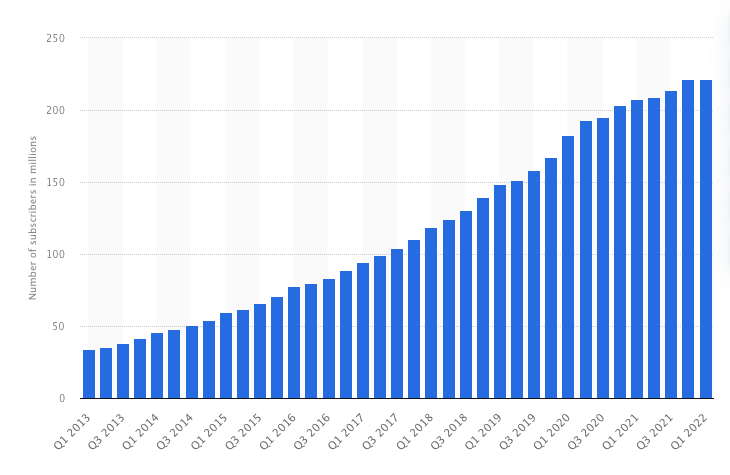

Total Subscribers: 221.64 million

Average Revenue Per Paying Member: $11.97

Cash From Operations: $393 million

Operating Income: 6.2 billion

Operating Margin: 21%

Free Cash Flow: - $158.89 million

Content Obligations: approx. $22 billion

Gross Debt: $14.6 billion

Net Debt: $8.6 billion

Source: Financial Times

Netflix derives revenue from monthly membership fees for streaming content.

The company offers a variety of streaming membership plans with prices varying depending on the country and the plan’s features. These range from $2 to $27 per month.

It has more than 200 million paid subscribers worldwide, paying an average of over $11 per month.

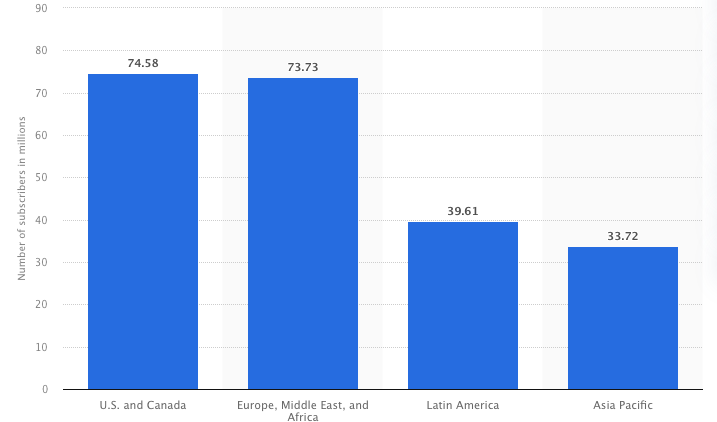

Average revenue per paying member is the highest in the US and Canada at $14.56 and the lowest in Latin America at $7.73.

The US and Canada are the largest market with nearly 75 million subs, followed by EMEA with close to 74 million, Latin America with 39 million and Asia Pacific comprising over 33 million subscribers.

Source: Statista

In 2021, Netflix generated $29.7 billion of revenue for an 18.81% increase from the year prior. In the last four years, the average revenue growth rate amounted to 26.38%.

The increase in revenue in 2021 was largely due to an 11% growth in average paying memberships and a 7% increase in average monthly revenue per paying membership from $10.91 to $11.97 (this metric is calculated as streaming revenue divided by the average number of streaming paid memberships).

The revenue growth resulted from price hikes and favorable fluctuations in foreign exchange rates.

Interestingly, in 2021, their legacy business of DVD rentals still contributed $182 million albeit this segment slid materially at 23.83% from the previous year.

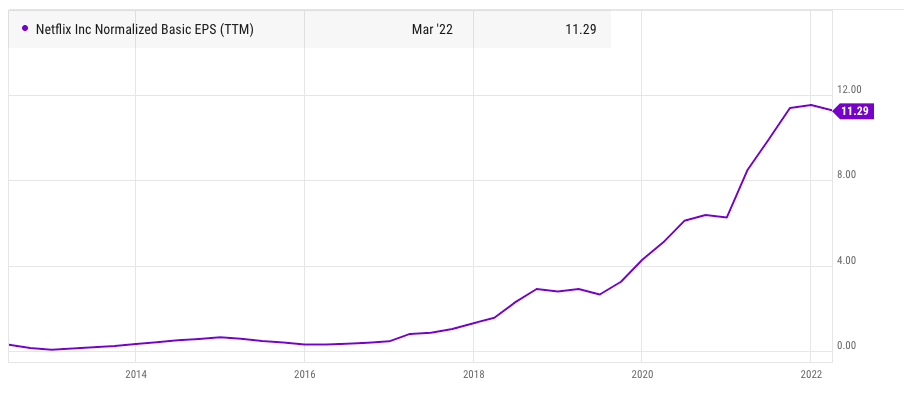

EPS has also been on a steady climb in the last few years, growing at above 75% and reaching $11.24 last year.

Source: YCharts

Source: Financial Times

This is where the good news ends.

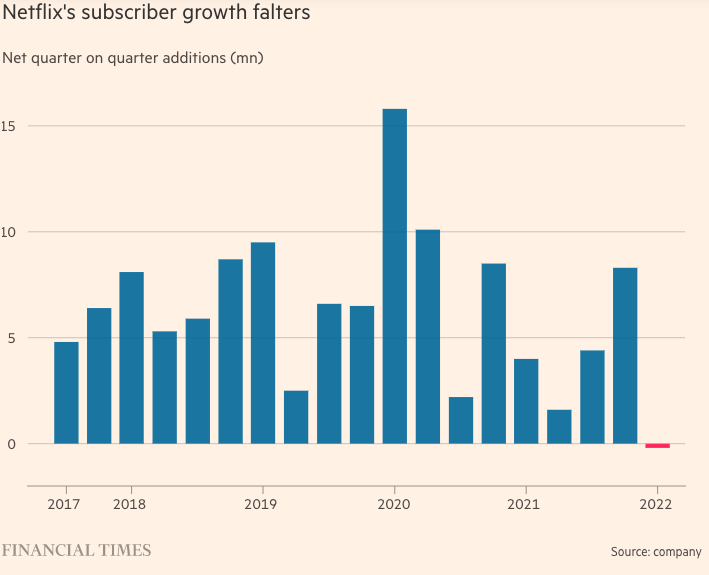

The canary in the saturation coal mine was already making noises last year, when the overall paid membership additions decreased by 50% (from 36.6 million in 2020 to 18.2 million in 2021) and not a single region registered increased additions relative to last year.

US and Canada, which is the most saturated market, slid 80% in this respect, Latin America went down by 60%, EMEA by 51%, and APAC by 23%.

Just to illustrate the degree of saturation in the US and Canada, last year, 90% of all paid net membership additions came from outside the region.

But the real blow came in Q1 2022, when Netflix announced losing subs for the first time in a decade, a trend that was followed up by the loss of 1 million subs in Q2 2022.

The company’s forecast was to reach 2.5 million paid net adds relative to 4 million in the previous year.

Instead, it lost 200,000 subscribers in Q1 and 1 million subscribers in Q2, largely as a result of the suspension of their service in Russia, macroeconomic weakness and their price changes.

Source: Financial Times

Source: Financial Times

Source: Chartr

As shown in the graphic above, amortization of content assets makes up the majority of cost of revenues.

Netflix acquires, licenses and produces content, including original programming. Typically 90% of content is expected to be amortized within four years after its first month of availability.

Other costs such as personnel expenses, music rights, production costs, streaming delivery costs and other operations make up the remainder of cost of revenues.

In 2021, cost of revenue went up largely due to a $1.42 billion increase in content amortization related to existing and new content, including more exclusive and original programming.

Other costs of revenue increased by $633 million, primarily due to growth in content production coupled with an increase in expenses for streaming delivery and payment processing fees.

However, when looking at the cost as a percentage of revenue, it decreased from 61% to 58% due to delays in content releases because of the pandemic, resulting in content amortization growing at a slower rate as compared to the growth in revenue.

Source: YCharts

Content is Netflix’s lifeblood. Until recently, it was the primary growth engine for the business.

Currently, however, Netflix seems to be boxed in, as any cuts in content spending could lead to a risk of further subscriber losses.

Over the years, the company has been steadily increasing the produced-to-licensed content ratio. In 2019, produced content stood at 21%. It then increased to 30% in 2020 and 34% in 2021.

Such a ratio increase requires humongous spending.

The company’s total content obligations which include amounts related to the acquisition, licensing and production of content are now surpassing $22 billion, $15.8 billion of which is not included on the balance sheet.

In 2021, content investment increased by 39% relative to a 13% increase in content amortization.

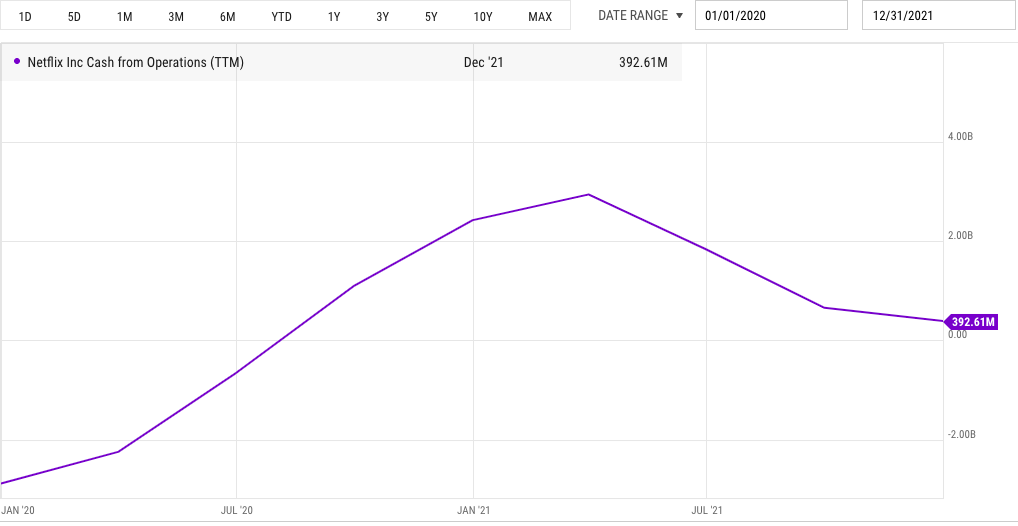

Such heavy investment requires upfront cash payment and has a great impact on both cash from operations and free cash flow.

Last year, net cash provided by operating activities decreased by a staggering $2.03 billion from the year prior to $393 million. Whereas free cash flow was $5.2 billion lower than net income, primarily due to cash payments for content assets.

Source: YCharts

Net cash generated by operating activities in Q1 was $103 million and free cash flow amounted to $13 million.

Netflix expects to be free cash flow positive for the full year and beyond and targets a 19%-20% operating margin for 2022.

The streaming giant uses a lot of leverage to fund content production.

At the end of Q2 2022, gross debt decreased slightly to $16.9 billion and net debt was $11.1 billion, equating to a 1.5x LTM leverage ratio (calculated as net debt divided by last twelve months adjusted EBITDA).

Woes

When growth came to a halt in 2021, the company’s executives thought it was a simple case of the pandemic pulling the expansion forward.

But now the C-suite has realized that their outlook was clouded and there are actually many structural headwinds at play that impact the company’s performance.

Hardware

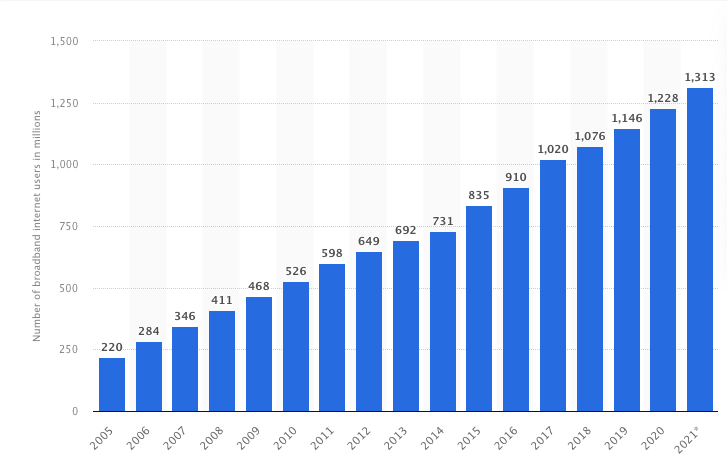

Netflix sees its TAM as all broadband homes. Their long-term game plan is to attain the highest possible broadband household penetration.

In 2021, the number of wired broadband subscriptions was estimated to have reached 1.3 billion connections worldwide.

Source: Statista

However, new variables came into play in relation to hardware. Early in the game, Netflix knew that the majority of their viewing was on TVs which still holds today.

Reed Hastings was opposed to developing Netflix’s own hardware, so that it would not appear that he is competing with the giants he wanted to partner with for distribution. Instead, it cleverly placed the Netflix button on most remote controls.

Most recently, the demand for connected TVs has started to soften, while the on-demand entertainment service space became very crowded with many players competing for attention on these devices, diluting attention.

Sharing

The company estimates that Netflix is shared with over 100 million additional households that do not pay for the service. 30 million of such households are in North America.

In the past, account sharing was a powerful expansion tool and was encouraged by the company. However, as growth stalled and saturation became an issue, it is now a major drag on revenue and Netflix is intensely looking at ways to crackdown on this phenomenon.

This will most likely take the form of additional payments for sub-accounts.

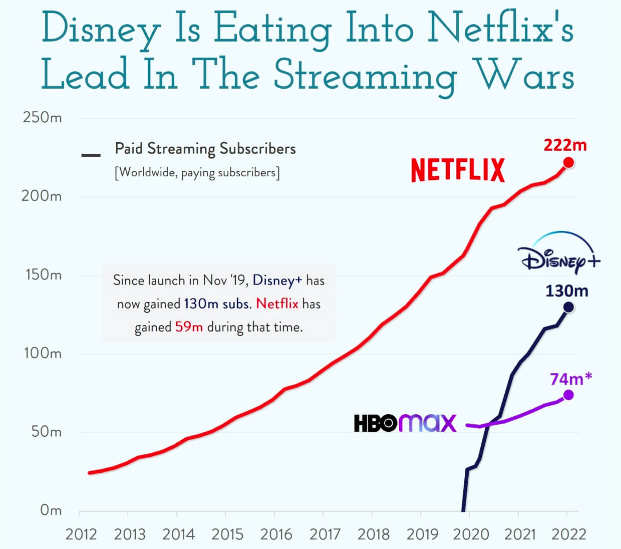

Competition

The company’s competition has always been robust. In the last fifteen years, Netflix went against linear TV, YouTube, Amazon, Hulu and the entire Hollywood, all the while transforming the television and movie industries.

From 2018 through 2021, Netflix spent $55bn on content to compete with these players.

However, in the last three years, the company’s remarkable success propelled traditional entertainment companies to a realization that streaming is the future.

So the largest media conglomerates went out to launch or buy their streaming platforms and content studios.

The space is now getting crowded to put it mildly.

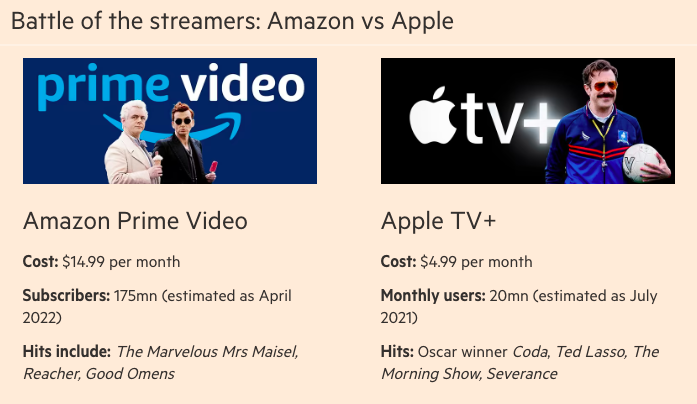

Companies which emulate Netflix include Disney’s Hulu and Disney+, Warner Bros Discovery’s HBO Max, NBCUniversal’s Peacock, Paramount’s Paramount+, as well as Amazon and Apple.

As the streaming land grab heats up, each of these companies has to spend enormous amounts of cash to compete.

In 2019, Amazon spent $1bn on a single Lord of the Rings TV show, the most expensive show in history.

And the content arms race is spiraling into new levels of staggering capital allocation. If you include sports rights, these behemoths are projected to shell out $140 billion in aggregate this year alone.

The splurge comes right around the time when growth is waning.

Most of the deep pocketed players are projected to significantly dilute their profit margins and lose money on their streaming pursuits. Yet, the alternative is to be left behind in the race.

Netflix is facing the toughest competition from legacy content creators such as HBO, Disney, NBCUniversal and Paramount and companies with the ability to spend big such as Amazon and Apple.

Source: Financial Times

This year, Disney’s investment in streaming content is likely to dwarf that of Netflix, as the company will spend $23 billion on new movies and TV shows and additional $10 billion on sports rights, marking a 32% increase in spending from last year.

Source: Chartr

As companies rush to produce shows to feed their streaming services, production costs are rising.

The competition for all parts of making content instigated a battle for locations and talent, pushing the prices up. Sound stages are now attracting investment from private equity groups.

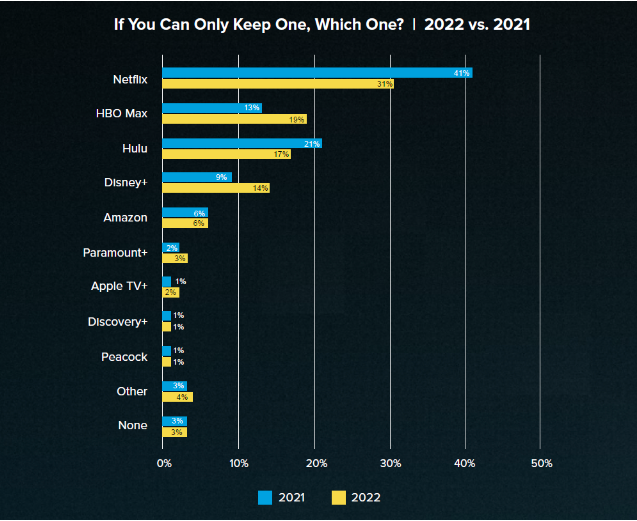

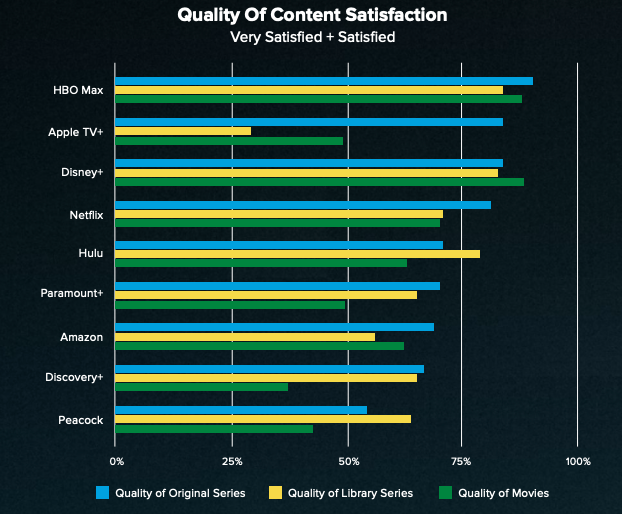

A recent Whip Media 2022 Streaming Satisfaction Report surveyed the landscape, measuring customer satisfaction with Netflix, Disney+, HBO Max, Apple TV+, Hulu, Peacock, Paramount+, Amazon’s Prime Video and Discovery+.

The survey showed that Netflix should fear HBO Max the most.

Netflix still leads the pack as the most indispensable service. 31% of US respondents said they would keep the service, if they could have just one subscription.

HBO Max came in second with 19%.

Despite retaining the crown for being the essential service, however, Netflix dropped by 10% relative to last year.

Source: Whip Media

Netflix also ranked at the top on user experience and content recommendation which is not surprising.

The company not only had a tech head start, while other companies are still playing catch up but it has put an enormous effort into the recommendation algorithm and product interface.

Netflix hired an army of engineers who AB test everything and put a lot of thought into product engineering.

The company also has the ability to subtitle and dub all of its shows in 30 languages without any lag, thanks to embedding local servers in every country they operate in.

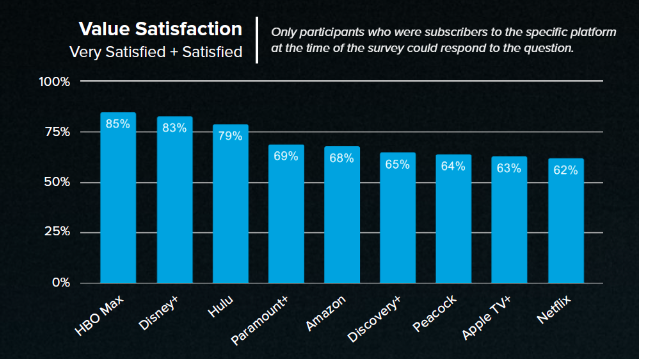

However, Netflix came last out of the nine services on perceived value satisfaction, where HBO Max emerged as the leader, followed by Disney+.

Source: Whip Media

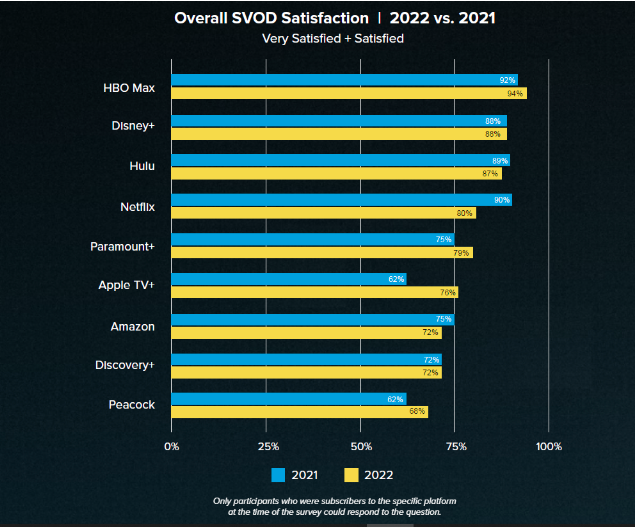

Overall, when it comes to general customer satisfaction, HBO reigns supreme with 94% of respondents being satisfied or very satisfied, followed by Disney+ (88%), Hulu (87%) and Netflix (80%).

Apple TV+ made the biggest gains in customer satisfaction in 2022, climbing 14% to 76% and surpassed Prime Video, Peacock and Discovery+.

Source: Whip Media

HBO Max also leads in satisfaction for the quality and variety of original content where Netflix ranks fourth and second respectively.

Source: Whip Media

The report concludes with the following recommendations:

“Despite its well reported subscriber losses, and declines in satisfaction, Netflix is still in a healthy position. Its satisfaction scores for both quality and variety of original and library series remain strong. Its user experience is the best of all the SVODs. However, its service is now generally priced higher than its competitors (depending on the tier), and the competitors also have highly regarded content. They will continue to need compelling shows to compete, and they might want to more frequently do additional seasons of their hits, a strategy they’ve often shunned. That will help build their library and, maybe, prevent churn”.

When it comes to increased competition, many experts claim, Netflix does not only compete with providers of long form passive content consumption.

In fact, the company has to face a battle for attention with social media companies (TikTok in particular can chain consumers to the screen for hours on end) and gaming (a pocket Netflix is attempting to break into).

Cost-conscious consumers

Even if competition for content consumers is rife, recent data from Ampere Analysis suggests that the key factor in the subscriber exodus has nothing to do with competing content but rather pertains to the actual pressure on household finances, resulting from higher inflation and a stock market meltdown.

The data reveals that in the two weeks after canceling their Netflix subscription, 87% of subscribers had not signed up to a rival service.

Many of those that left Netflix were aged between 18 and 24, or in households with an annual income of less than $15,000.

Netflix subscriptions in low-income households went down from 56.2% to 49%.

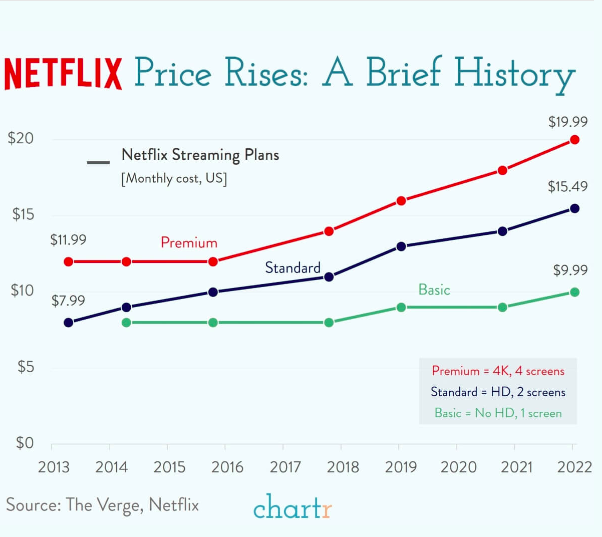

The subscriber subsidence came after the company raised the price in the US for its standard plan by $1.50 to $15.49.

The Whip Survey confirms this view. 69% of former Netflix customers said the price increases led them to drop the subscription.

Source: Chartr

The analysis also raised questions over its content. The data suggests that Netflix has a growing army of capricious subscribers who are willing to join and cancel depending on whether they find anything they want to watch.

And the binge-watching format is aiding this trend, as viewers can gobble up an entire series in one weekend, drop the service and rejoin when another series of interest hits the screen.

Lesser Economic Model

As the streaming competition intensifies, Wall Street analysts started to ring alarm bells that the streaming economic model cannot match that of cable television and will significantly dilute profit margins of the companies that are pursuing the battle for streaming dominance.

There are a few reasons for this:

- Streaming providers offer a limited service which does not include sports, live shows, local content or news and, therefore, cannot charge what cable charged in the past.

- Cable TV was approximately $50 per month, whereas Netflix’s $15.49 monthly charge is already considered a premium price that triggered a subscription meltdown.

- Cable had 90 million customers at $50 per month. Netflix has 221.64 million paid subscribers at $11.97 per month. A quick, back of the envelope calculation shows that 2.5 times more subscribers in streaming yield only 58% of cable revenue. And the more Netflix grows internationally, the more ARPU goes down, as pricing is much lower outside the US.

- On top of that, you have the perpetual spending on content to elbow out competitors, retain existing subscribers and acquire new ones. Netflix’s content obligations now stand at 74% of last year’s revenue and have to be financed through debt, as interest rates rise.

With this in mind, Wall Street now favors the so-called “arms dealer” strategy of supplying films and TV shows to streaming services, where Sony, for example, has been making money.

Rich Greenfield, an analyst at LightShed, recently wrote:

“While it feels hard to fathom abandoning streaming ambitions with so much capital committed to original streaming programming over the next several years, we wonder if that is the hard decision management teams such as NBCUniversal and Paramount should make?”

Future

As a result of all the aforementioned woes, Netflix announced:

- a clampdown on account sharing,

- “bigger, fewer, better” content,

- job cuts, and

- despite a longstanding opposition to the notion from Hastings, an introduction of an ad-supported subscription tier.

One of the most prominent Wall Street stories that surfaced during Netflix’s tumultuous period, pertained to Bill Ackman’s Pershing Square which amassed a stake worth $1.1bn in the company over the course of a few days in late January, making the hedge fund a top-20 shareholder in Netflix. Ackman pledged to focus on the “long-term horizon”.

However, once the subscriber loss transpired during the Q1 earnings call, Ackman quickly ran for the exit, losing roughly $400 million on the investment in a matter of months.

While many were quick to look down on the move, as yet another example of poor stock picking coupled with high concentration, Ackman’s letter to his investors offers an insightful and nuanced take on the company’s future. Most importantly, it underlines that the dispersion of outcomes for the company has widened.

Here is an excerpt from the letter:

“While we have a high regard for Netflix’s management and the remarkable company they have built, in light of the enormous operating leverage inherent in the company’s business model, changes in the company’s future subscriber growth can have an outsized impact on our estimate of intrinsic value. In our original analysis, we viewed this operating leverage favorably due to our long-term growth expectations for the company. Yesterday, in response to continued disappointing customer subscriber growth, Netflix announced that it would modify its subscription-only model to be more aggressive in going after non-paying customers, and to incorporate advertising, an approach that management estimates would take “one to two years” to implement. While we believe these business model changes are sensible, it is extremely difficult to predict their impact on the company’s long-term subscriber growth, future revenues, operating margins, and capital intensity. We require a high degree of predictability in the businesses in which we invest due to the highly concentrated nature of our portfolio. While Netflix’s business is fundamentally simple to understand, in light of recent events, we have lost confidence in our ability to predict the company’s future prospects with a sufficient degree of certainty. Based on management’s track record, we would not be surprised to see Netflix continue to be a highly successful company and an excellent investment from its current market value. That said, we believe the dispersion of outcomes has widened to a sufficiently large extent that it is challenging for the company to meet our requirements for a core holding. One of our learnings from past mistakes is to act promptly when we discover new information about an investment that is inconsistent with our original thesis”.

Conclusion:

- Netflix is the world’s largest streaming service.

- The company went from a DVD online rental service to a streaming pioneer, to a content producing powerhouse.

- It invented the binge-watching format and mastered international expansion by producing multiple hits series outside Hollywood which are instantly available in 30 languages.

- Netflix’s streaming services are available worldwide with the exception of Mainland China, Syria, North Korea, and Russia.

- The company has 221.64 million paid subscribers worldwide, who pay an average of $11.97 per month.

- Average revenue per paying member is the highest in the US and Canada and the lowest in Latin America.

- North America is the largest market, followed by EMEA, Latin America and Asia Pacific.

- Last year, overall paid membership additions decreased by 50%.

- US and Canada, which is the most saturated, slid 80% in this respect, Latin America went down by 60%, EMEA by 51%, and APAC by 23%.

- In 2021, 90% of all paid net membership additions came from outside the US and Canada.

- In Q1 2022, Netflix announced losing subs for the first time in a decade. The company’s forecast was to reach 2.5 million paid net adds but it lost 200,000 subscribers.

- In Q2 2022, Netflix lost a further 1 million subscribers, although they forecasted to gain 1 million subscribers in the next quarter.

- Softening demand swept across most of the regions with the exception of APAC.

- Netflix continues to increase the produced-to-licensed content ratio each year (currently 34% of content is produced) which entails huge spending.

- Its content obligations now surpass $22 billion (approx. 74% of last year’s revenue).

- Such heavy investment requires upfront cash payment and has a great impact on cash from operations and free cash flow, although the company expects to be FCF positive for the year.

- A lot of entertainment companies have entered the streaming arms race by launching or buying their streaming platforms and content studios.

- Netflix now has to compete with Disney’s Hulu and Disney+, Warner Bros Discovery’s HBO Max, NBCUniversal’s Peacock, Paramount’s Paramount+, as well as Amazon and Apple.

- These behemoths are projected to spend $140 billion this year alone, even though the streaming part of the business will not be profitable for most.

- This land grab is pushing production costs up in a self-reinforcing cycle.

- As the space gets more and more crowded, Netflix remains the leader as the indispensable service (31% would keep it, if they could only keep one) but the margin has narrowed and HBO Max is climbing.

- The company is also leading the tech game, as their user experience and content recommendation are unrivaled.

- However, Netflix ranks last on perceived value and has been taken out by HBO Max on the quality and variety of original content.

- The company has blamed many factors for the sluggish growth, including geopolitical events, account sharing, softening demand for connected TVs and strong competition.

- However, a recent survey showed that most subs dropped out because of price increases. The exodus is particularly acute in the low-income stratosphere.

- There are also more subs who dip in and out, depending on whether they find interesting content. Binge-watching aids this trend.

- Many on Wall Street now claim that streaming will not replicate cable economics. In light of this, supplying content to the streamers is a more profitable strategy.

- As a result of all its woes, Netflix announced a clampdown on account sharing, “bigger, fewer, better” content, and an introduction of an ad-supported tier.

- In the words of Bill Ackman, “it is extremely difficult to predict the impact of these business model changes on the company’s long-term subscriber growth, future revenues, operating margins, and capital intensity”.