How Intel Lost Its Way

Sign up for ARPU: Stay ahead of the curve on tech business trends.

In 1988, Intel's then-CEO Andy Grove published a book titled "Only the Paranoid Survive," urging companies to adapt to market shifts and disrupt even their own successful models. The book became a business classic, a gospel of sorts in Silicon Valley. Ironically, Intel, once the undisputed king of semiconductors, now embodies the dangers of ignoring that very advice. The company most recently posted a staggering $16 billion quarterly loss, and its stock has lost 60% of its value in 2024.

Intel's Market Segments in Trouble

Intel's declining fortunes can be attributed to a multitude of factors. A central issue has been Intel's inability to keep pace with advancements in chip manufacturing. The company, which once held a clear lead in this field, has fallen behind Taiwan Semiconductor Manufacturing Company (TSMC), which now produces the most advanced chips.

This didn't happen overnight. Morningstar's Brian Colello observes that "for several years, Intel has struggled by falling behind the curve on chip manufacturing, moving from a technological advantage over Taiwan Semi to a clear technological disadvantage in recent years." This technological lag has had a cascading effect on Intel’s ability to compete across all market segments.

Furthermore, Intel failed to capitalize on key market trends. The rise of mobile computing, for example, caught the company off-guard. The shift towards more energy-efficient processors and designs based on ARM architecture left Intel scrambling to catch up. A Wall Street Journal piece highlights this challenge:

For a concrete example of Intel’s challenges, look at Amazon, the world’s biggest provider of cloud computing. More than half of the CPUs Amazon has installed in its data centers over the past two years were its own custom chips based on ARM’s architecture, Dave Brown, Amazon vice president of compute and networking services, said recently.

This displacement of Intel is being repeated all across the big providers and users of cloud computing services. Microsoft and Google have also built their own custom, ARM-based CPUs for their respective clouds.

The company also failed to anticipate the demand for GPUs used in AI applications. While competitors like Nvidia have experienced explosive growth in this segment, Intel has struggled to make inroads.

"Intel … has some AI products, but they don’t appear to be making much of a dent in the market vs. Nvidia," says Colello

And even in segments it did control, like desktop and notebook CPUs, its dominance is being threatened. The introduction of ARM based processors that can run Windows, particularly Qualcomm’s Snapdragon X Elite, threatens Intel’s most important market segment, per EPSNews:

Qualcomm’s new Snapdragon X Elite processor...is already positioned as a formidable rival to Intel’s Core chips... With promises of higher performance and longer battery life, Qualcomm’s processor threatens to erode one of Intel’s most important market segments.

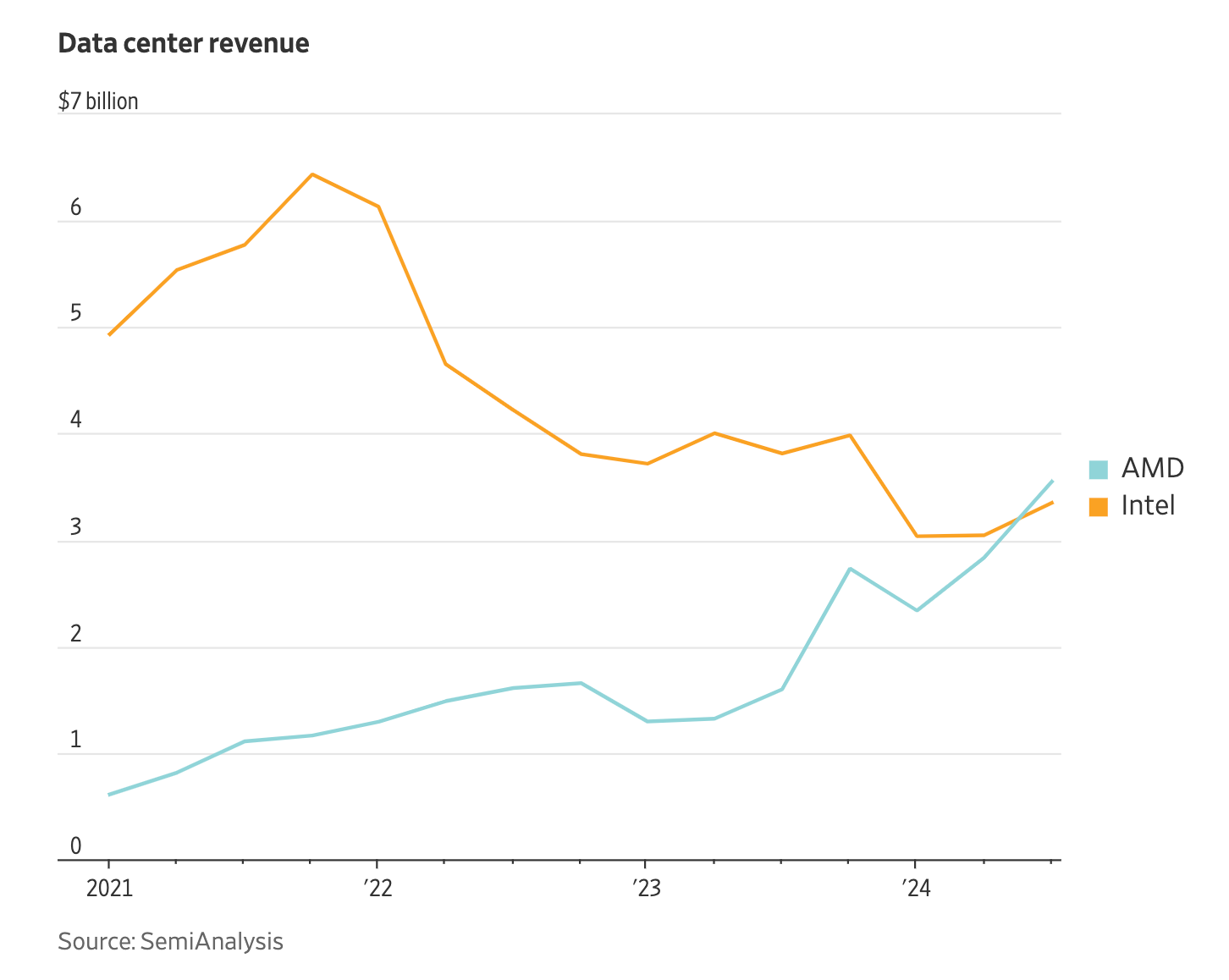

In the data center market, where Intel has historically been strong, it has been losing share to competitors, especially AMD. In the latest quarter, AMD eclipsed Intel’s revenue for chips that go into data centers. This is a "stunning reversal", says the Wall Street Journal:

In 2022, Intel’s data-center revenue was three times that of AMD... AMD and others are making huge inroads into Intel’s bread-and-butter business... Even worse, more and more of the chips that go into data centers are GPUs, short for graphics processing units, and Intel has minuscule market share of these high-end chips. GPUs are used for training and delivering AI.

Intel and Vertical Integration

Central to Intel’s historical success, and now a key factor in its current struggles, is its traditional business model, a vertically integrated approach that was once considered a gold standard in the semiconductor industry. Unlike many other companies that specialize in either chip design or chip manufacturing, Intel has long adhered to a model of doing both. This meant that Intel controlled the entire process, from the initial design of a chip to its final production in their own factories. This vertical integration initially provided Intel with significant advantages. As David Vellante explains:

For Intel, Wright’s Law once represented a formidable moat. Because Intel had the highest wafer volumes, thanks to its market share in PCs, it was able to protect profitability by capitalizing on its leadership in semiconductor manufacturing. Importantly, it was always first to market with the most advanced chips and it maintained a cost advantage for decades.

To better understand the advantage that high volumes provide, it is important to understand the concept of "wafer volume." In semiconductor manufacturing, chips are not made individually. Instead, they are built on large, circular "wafers" of silicon, and many chips are created on each wafer at the same time. Wafer volume refers to the total number of these wafers a company produces. Companies with higher wafer volumes benefit from the "learning curve" effects, also known as Wright's Law, where costs decline with increasing cumulative production volume.

In essence, Intel's control over both design and manufacturing allowed it to optimize its processes for its specific needs, enabling rapid innovation and cost efficiency. The company could also align its manufacturing roadmap with its product designs seamlessly, reducing time-to-market and ensuring a smooth, controlled supply chain. Moreover, Intel’s high production volumes for its x86 processors in PCs and servers allowed them to fully leverage Wright's Law, gaining further cost efficiencies and advantages over competitors who were unable to match those economies of scale, as Vellante notes: "For decades, Wright's Law has been a guiding principle in manufacturing generally and the semiconductor industry specifically. It explains how production efficiencies and cost reductions follow learning curves… and was the driving force behind x86’s ascendency.”

However, this once-powerful advantage has now become a significant liability. The key development that undermined Intel's vertical integration was the rise of specialized foundries like TSMC and Samsung, who were able to achieve greater manufacturing expertise and economies of scale by focusing solely on chip production for multiple clients.

This loss of advantage was exacerbated by two major factors. Firstly, the rise of the mobile market and the proliferation of ARM-based chips led to a massive increase in wafer volumes produced by TSMC and other foundries for these mobile devices:

When PC volumes peaked in 2012, Intel’s manufacturing cost advantages began to wane. Arm wafer volumes exploded with the adoption of smartphones… these volumes surpassed those of x86 and conferred major cost and time-to-market advantages to TSMC and its design partners.

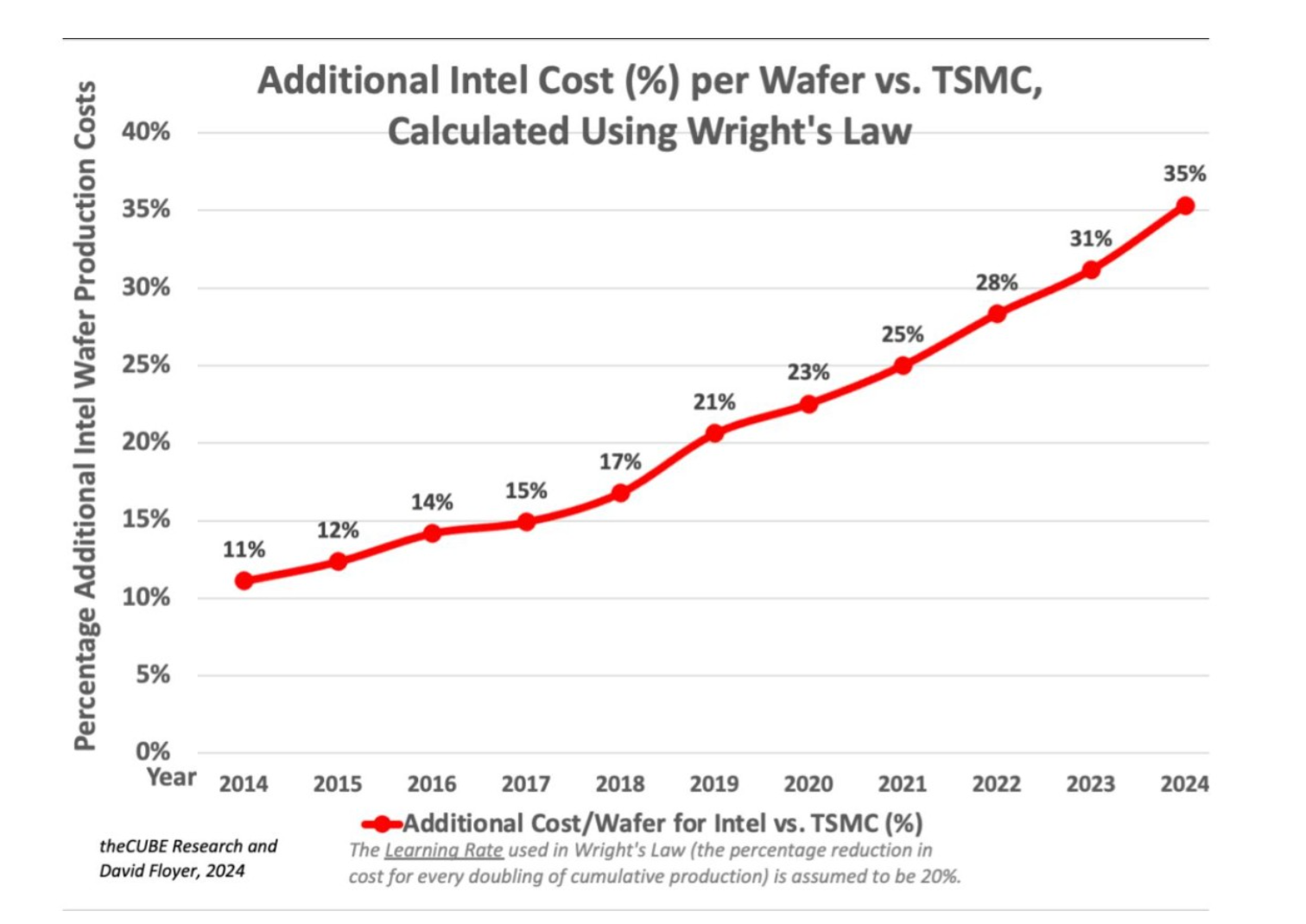

Secondly, Intel itself faltered in its manufacturing execution, falling behind in the race to produce smaller and more efficient nodes. This combination meant that Intel could no longer leverage Wright's Law, instead becoming less cost competitive than other companies, including AMD who partnered with TSMC for chip manufacturing. Industry analysis estimates that Intel’s production cost per wafer is approximately 35% higher than TSMC’s.

Intel’s adherence to the vertical integration model also made it less agile and responsive to market changes. Because they had an established infrastructure and production process, the company was slow to embrace the mobile revolution. Meanwhile, fabless design houses like AMD, who worked closely with dedicated foundries, were able to quickly iterate and produce more cutting-edge designs. The rise of the smartphone era, combined with Intel's manufacturing stumbles, eroded the vertical integration advantage, turning it into a barrier to innovation and competitiveness, as Intel could no longer rely on its own fabs to provide it with a competitive edge.

Fading Relevance of x86 Architecture

The company's reliance on its x86 architecture also became a limitation. x86 is a type of instruction set architecture (ISA), which defines the basic instructions that a CPU can understand and execute. For decades, the x86 architecture was the dominant standard for personal computers and servers, and Intel built its business around this architecture. However, the rise of mobile computing and AI has shifted the focus towards more energy-efficient and specialized architectures, like those based on ARM.

ARM, unlike x86, is not a monolithic architecture; it is an architecture that can be licensed by other companies to create custom designs. It also allows for a focus on energy efficiency and has made it a mainstay in mobile phones and many other low power applications.

ARM, unlike x86, is not a monolithic architecture; it is an architecture that can be licensed by other companies to create custom designs. It also allows for a focus on energy efficiency and has made it a mainstay in mobile phones and many other low-power applications:

Before the smartphone era, x86 was the dominant instruction set within general-purpose CPUs... this platform shift is precisely what happened with the smartphone era... power efficiency was far more critical for smartphones due to battery constraints... and this is where Intel lost out to competing ARM-based smartphone SoCs. (SemiAnalysis)

The shift towards ARM has challenged the long-held dominance of x86 in the computing world and Intel's inability to adapt to this shift is a major factor in its decline.

Intel's Pivot

Faced with these challenges, Intel has started to treat its foundry business as a more independent entity – a move initiated even before Pat Gelsinger’s removal as CEO:

Mr. Gelsinger has already announced plans to make Intel’s foundry business an independent subsidiary. He has argued that the time is not right for a complete spinoff, since the foundry needs guaranteed business from Intel’s own chip design operations to fill its factories. Intel already uses Taiwan Semiconductor Manufacturing Company to make some chips it designs and might make more such decisions if it were entirely independent, some analysts said.

While a full separation is not imminent, this move signals a potential shift away from Intel's traditional, vertically integrated model.

Intel's hopes for a turnaround are also pinned on its 18A node technology, the culmination of Gelsinger's ambitious plan to regain a leadership position in chip manufacturing. The "18A" designation refers to Intel’s attempt at producing a new generation of chips, with a feature size of 18 angstroms (an angstrom is one ten-billionth of a meter). 18A is designed to be the final phase of Gelsinger’s plan to have Intel race through five so-called nodes in four years. If successful, this new manufacturing process is meant to allow Intel to produce the world's most cutting-edge and fastest chips once again.

However, the success of 18A is far from assured. Per Stacy Rasgon of Bernstein:

We might have expected Pat to at least make it until 18A is out the door (at which point we would see how it stacks up), and as he hasn’t, one has to wonder whether his departure foreshadows any negative implications for the health of the process roadmap.

So, what lies ahead for Intel? The company's core market — x86 CPUs — continues to shrink as the industry increasingly shifts toward ARM chips and GPUs, eroding Intel's once-dominant position. Compounding this challenge is the removal of Gelsinger, whose ambitious roadmap for manufacturing leadership, including the much-touted 18A node, was meant to revive Intel’s fortunes. While Gelsinger's departure raises doubts about Intel's ability to execute its turnaround strategy, the broader issue is that Intel’s current predicament is rooted in strategic missteps made years ago.

From its failure to anticipate the rise of mobile computing to its manufacturing setbacks and inability to adapt to emerging technologies like AI, the company has struggled to keep pace with a rapidly evolving market. As Intel now seeks to pivot— redefining its foundry business and pursuing cutting-edge manufacturing processes — its future hinges on whether it can overcome these structural challenges. The road ahead will be steep, and as Wolfe Research analyst Chris Caso notes, "Intel is in a difficult position, and the path forward will be difficult no matter the leadership."