Twilio: Product, Business Model, Growth

Sign up for ARPU: Stay informed with our newsletter.

In this week’s business review, we will look at Twilio. In particular, we will dissect Twilio’s value proposition, its go-to-market motion, its gross margins versus typical SaaS companies, and how its revenue model allows it to scale with its customers’ business use cases. We will also share our observations and thoughts on the growth trajectory of Twilio.

Without further ado, let’s dive in!

What is Twilio

Twilio is a software platform used by companies to communicate with their customers through SMS, voice, video or chat. Its value proposition is to empower companies of all sizes to create personalized experiences for their customers, which in turn drives customer engagement and loyalty.

If you ever get a text message from your favorite app or company, there is a good chance that it is powered by Twilio. Examples include Uber, who will text you when your Uber ride is here, Airbnb, who will remind you to confirm your booking through SMS, and Dell, who will keep you posted on the status of your order through SMS.

Today, more than 10 million developers worldwide use Twilio. Twilio provides companies with application programming interfaces (APIs), allowing them to access the communications networks (such as AT&T and Verizon) in just a few lines of code. The engineering teams then take these lines of code to create apps that allow them to communicate and engage with their customers.

What makes Twilio unique is that the platform turned the entire infrastructure and operation of sending SMS, voice, video and chat into a few lines of code. In a digital first world, where software engineers are a scarce resource, the ability for a company to instantly set up and test customer communication use cases – without the need to hire additional software engineers – is what differentiates such company from its competitors. And this is the insight has led Jeff Lawson, the founder of Twilio, to build Twilio into the platform it is today. What Twilio does to messaging, is what Stripe does to payment

So, let’s try and unpack their revenue model.

How Does Twilio Make Money

Twilio derives revenue from:

- Charging usage-based fees from customers using the software products within its communication APIs (for example, the number of text messages sent or received, minutes of call duration activity or the number of authentications).

- Charging monthly subscription fee from certain fee‑based products, such as the Email API, Marketing Campaigns, Twilio Flex and Twilio Segment.

In 2021, usage-based fees were responsible for generating 72 per cent of revenue (down from 76 per cent in 2020) and non-usage-based fees amounted to 28 per cent (up from 24 per cent in 2020). For the purpose of this article, I will focus on their usage-based service – i.e. communication APIs – which is their bread and butter. These APIs enable businesses to reach their customers on their preferred channels (SMS, voice, Whatsapp and so on).

It is important to understand the implication of Twilio charging these APIs on an usage-based and pay-as-you-go basis: any low-budget team can (1) implement the whole shebang of customer communications for, say, $10 on a credit card; (2) test and iterate different campaigns, strategies and use cases, and (3) continually scale customer communications as the business grows.

Such a usage-based model also sets Twilio apart from traditional software companies. Because a typical software charges on a price times user/seat basis, there is inherently a limit on how many seats and how many users a company can spend for that use case. That same limit for Twilio is much higher, because it is priced to the actual usage of a company’s sales motion to its customers that can be quantified with ROI. The laser focus of Twilio on communications means any business, regardless of industry and verticals, will have a use case of Twilio.

Take Nike as an example. They know when a customer lives in a fancy zip code, or has left a pair of Air Jordan in his cart, or has visited the Nike store multiple times the past week. Now if they send a thousand SMS to such customers, they know that they can convert, say, 30% of them. What is that worth to Nike? Perhaps 1% of the extra sales? So the unit economics is really shifted away from one of SG&A (cost center), to one of cost of goods sold. And the upshot is that the total addressable market (TAM) for Twilio is a multiple of how we traditionally look at software companies under a price times seat framework.

Traditionally, Twilio has a very developer-centric, self-service approach to its go-to-market motion, as it targets mainly SMBs and mid-market customers through land-and-expand. Starting in around 2017, they have dialled up their investment in enterprise sales and landed enterprise customers such as Nike, JP Morgan Chase and eBay. As Jeff Lawson has put it:

“And so every kind of company can really use our platform to improve their communications. We're very big believers in that. Whether it's for internal communications or external with your own customers, every company has an opportunity. And the bigger the company, the more communications occur and therefore, the bigger opportunity for Twilio. And so it's really -- for us, it's just about getting that first use case at a customer and then expanding out from there, and that's where we see the power of our usage-based model and that developer-first model.” - Jeff Lawson (Q4 2016 Earnings Call)

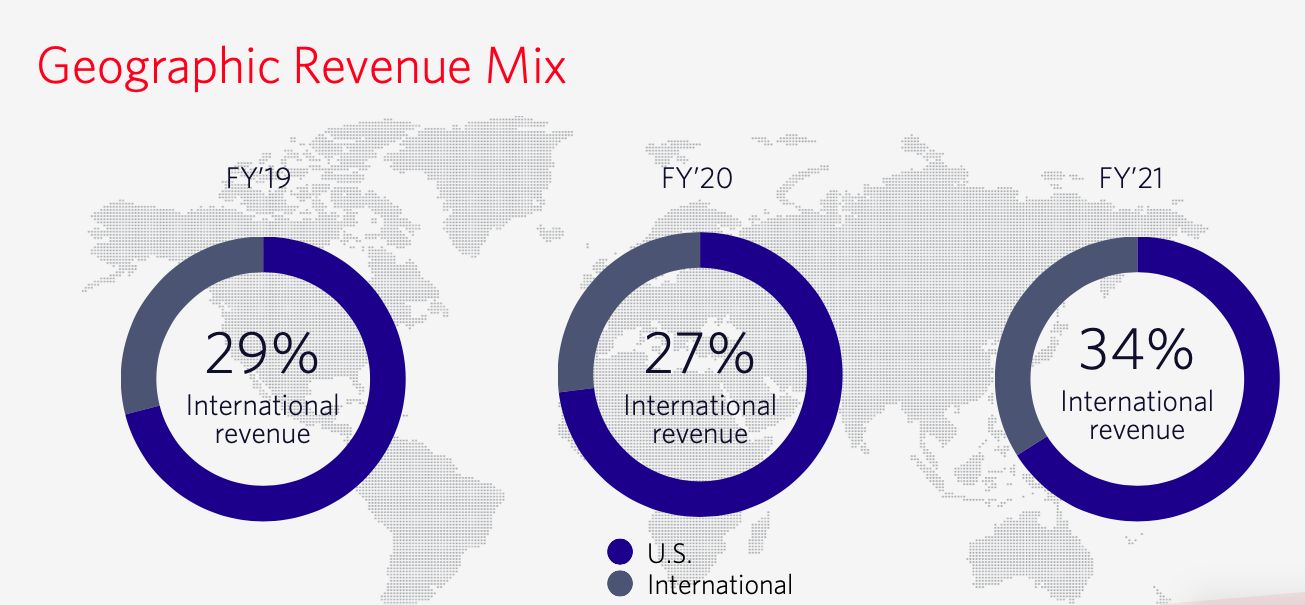

The biggest market for Twilio is the U.S. (66 per cent of revenue in 2021) but international exposure has been gaining traction. In 2021, international revenue increased to 34 per cent (from 27 per cent in 2020).

In the 13 years of its existence, the company enjoyed high double-digit revenue growth and gobbled up multiple, strategically important businesses along the way.

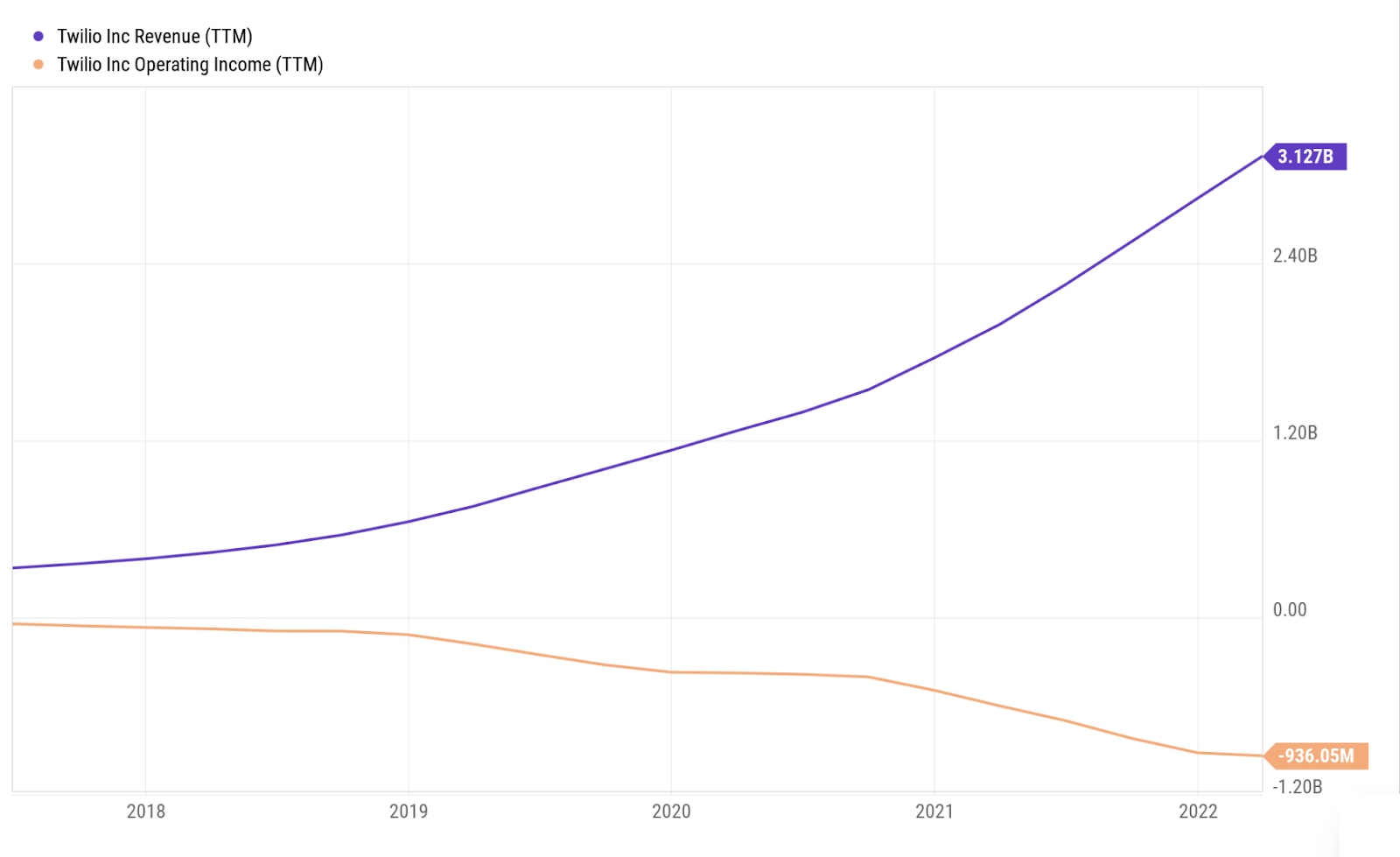

In 2021 alone, the company generated more than $2.8 billion in revenue, growing 61 per cent year-over-year. In just one year, it was able to deliver 1.3 trillion emails and sent nearly 127 billion messages.

And yet, the company has been unprofitable throughout, with operating loss exploding to $936 millon during the past 12 months.

Revenue Breakdown

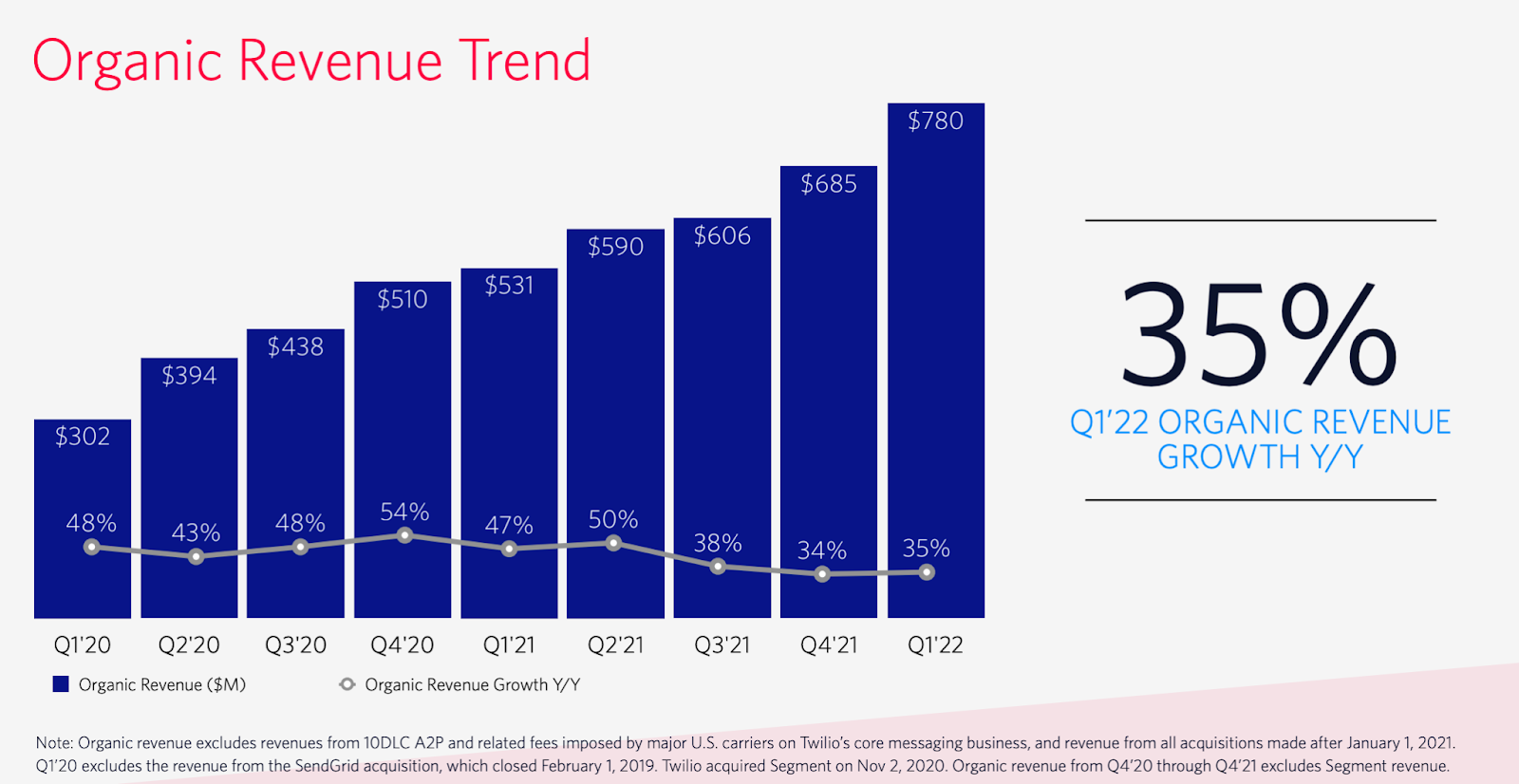

Organic revenue of Twilio has been growing consistently at over 30% year on year.

They have also consistently generated more than $1 incremental revenue per dollar spent on sales & marketing (by comparison, the sales & marketing efficiency for tech companies are typically less than 1)

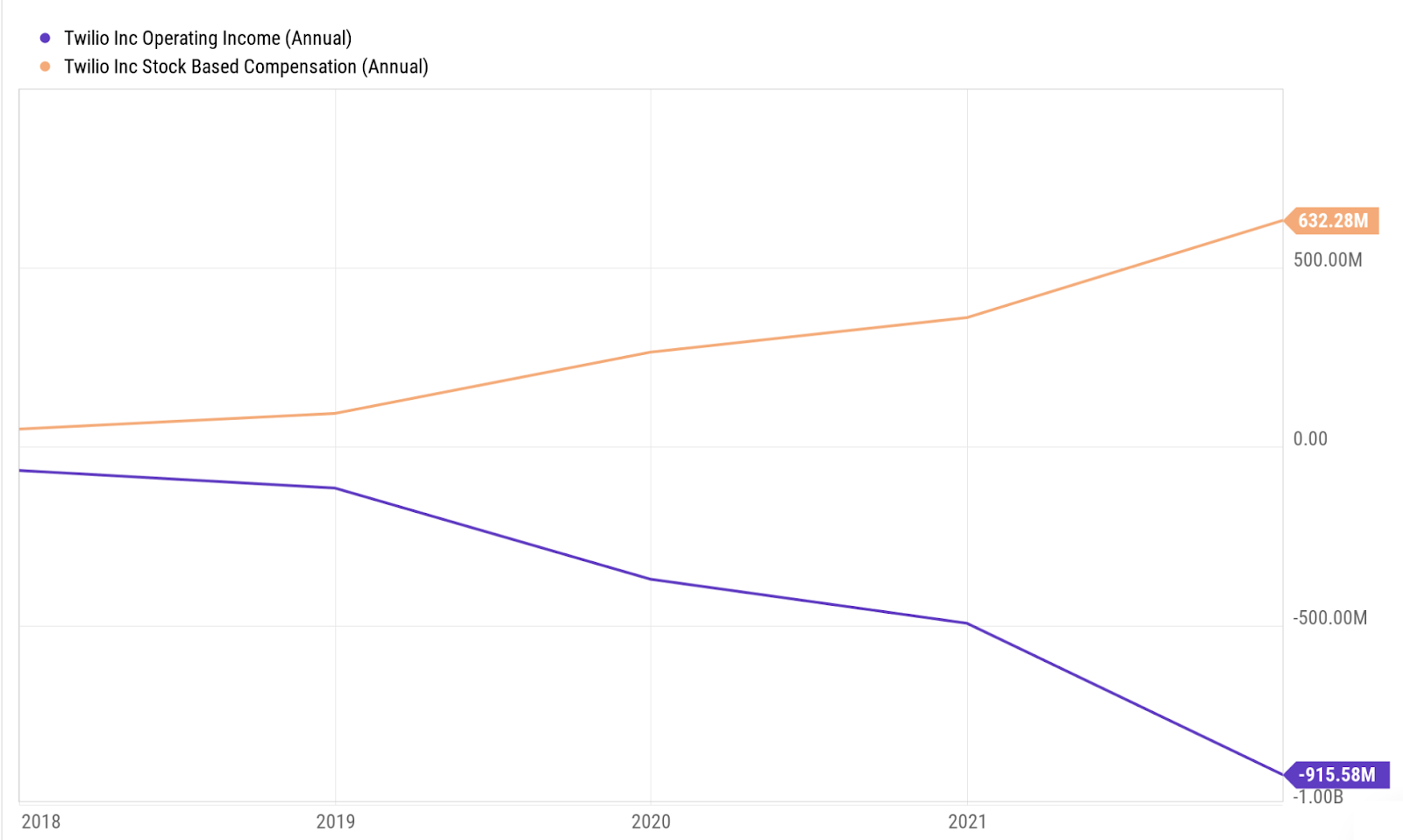

However, the revenue has not been translated into meaning operating income or free cash flow for the company. For the past 3 financial years, Twilio has racked up a combined $1.7 billion in operating loss and still paid out a combined $1 billion stock-based compensation (and one might wonder if the business is just a massive compensation scheme for the management)

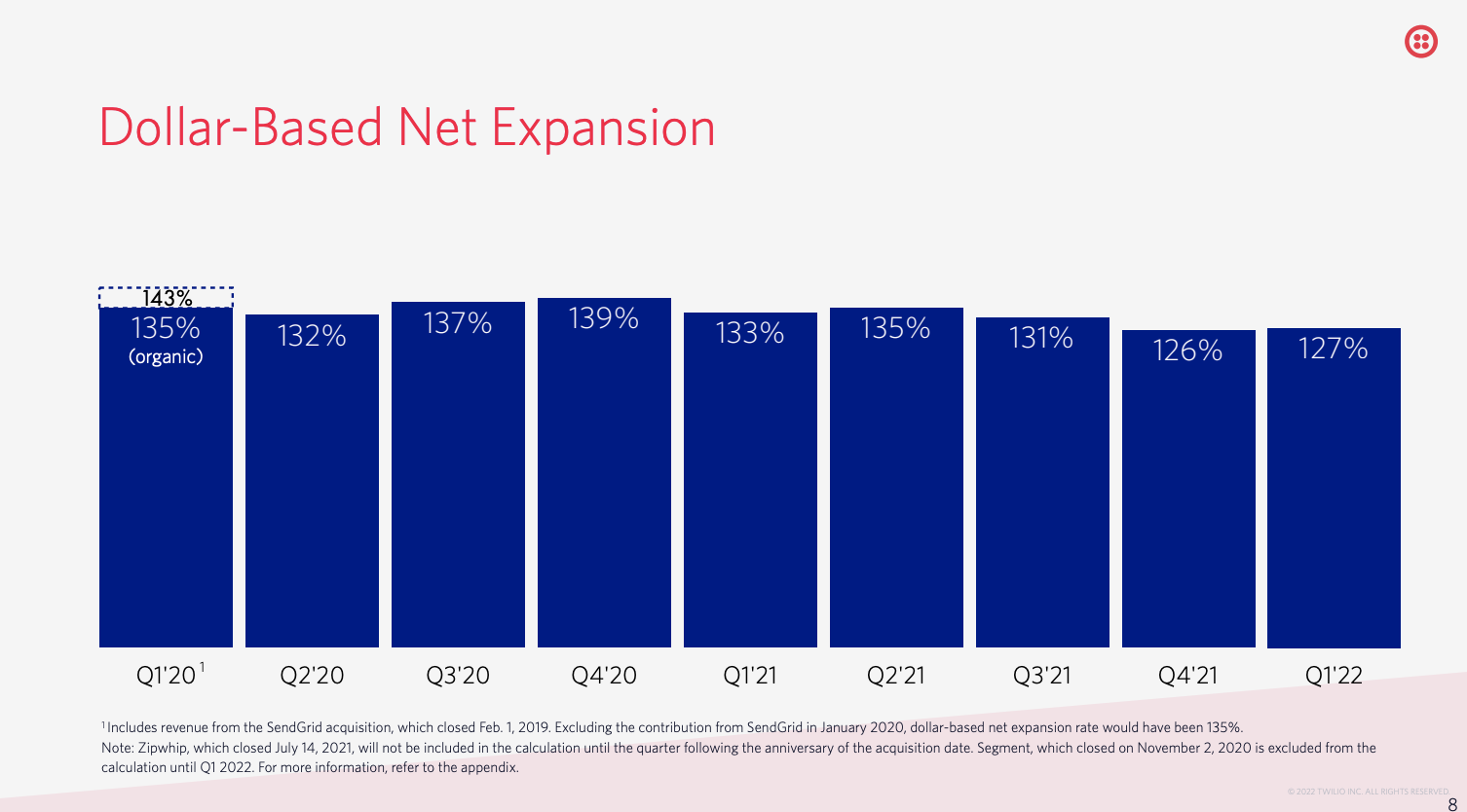

Another metric in the usage-based revenue model is the Dollar-Based Net Expansion Rate, which is a measure of revenue growth from the same cohort of existing customers. In the recent quarters, Twilio’s Dollar-Based Net Expansion Rate showed signs of slowing down:

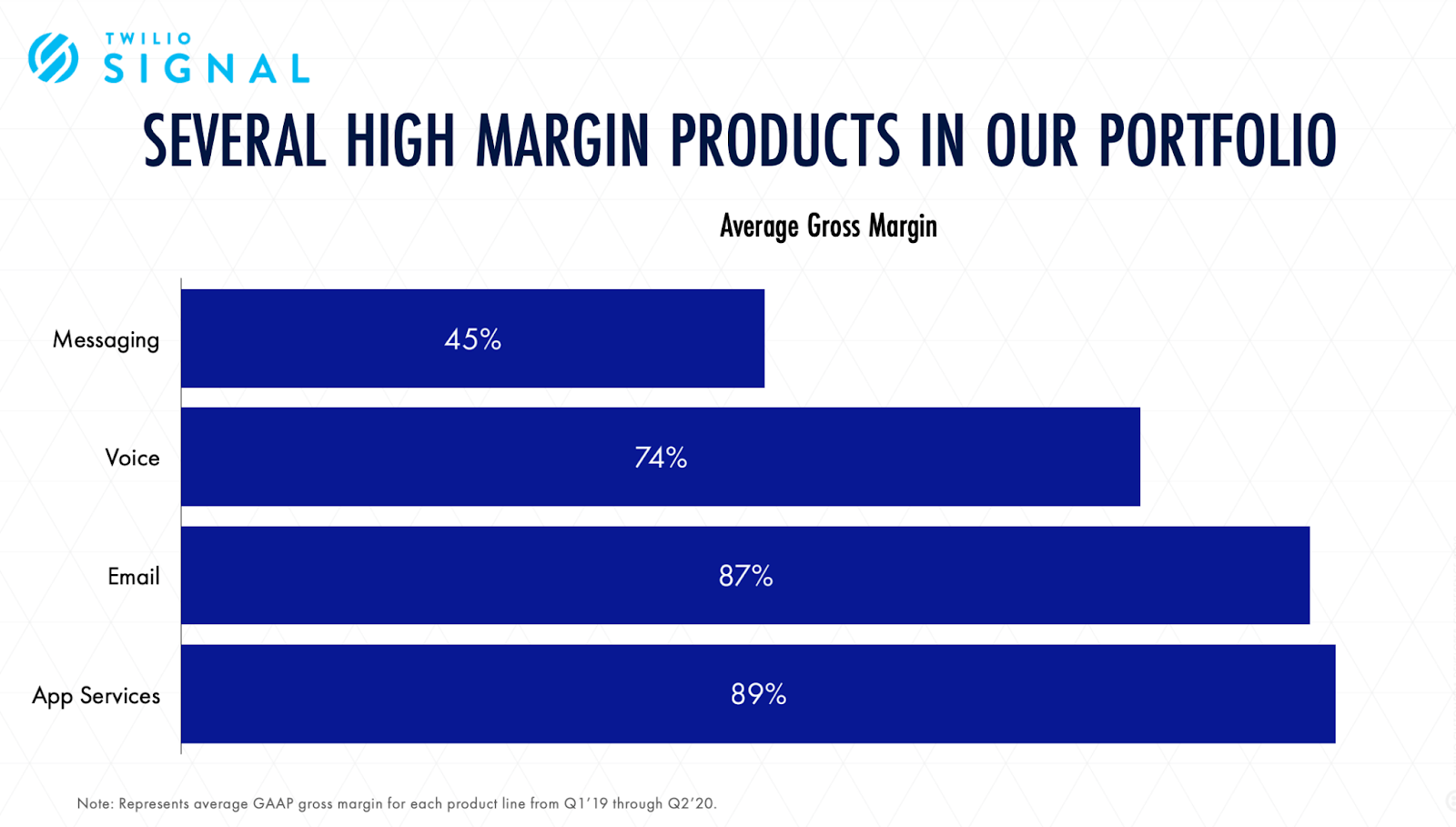

Note that Twilio’s gross margins are typically around 50%, which is much lower than the typical 70-80% you would expect from a software company. This is because a large bulk of Twilio’s revenue comes from their SMS API, and they have to route all the messages on behalf of its customers through the networks of AT&T or Verizon and pay these telecom providers. The chart below shows the average gross margin of their different products:

Conclusion

Twilio is surfing the digitization wave with tailwinds from the need to harvest first-party data and hyper-personalize interactions. They have a large addressable market beyond the typical SaaS limitation of people x seat, and their top-line growth has been very strong. However, the management also seems to have a short-sighted focus on revenue growth despite ever-rising losses, not to mention the extremely generous stock-based compensation. The technology stack is fascinating, but it remains to be seen how the business will evolve.

I hope you enjoy this article! Hit the button below to have insights and stories like this delivered to your inbox!