SoftBank's Woes: A Deep Dive

Sign up for ARPU: Stay informed with our newsletter.

In this week’s deep dive, we will look at SoftBank by unpacking its trajectory, its key financial metrics, the recent turbulence and what could be next for this complex conglomerate.

Without further ado, let’s dive in!

The Context

Masayoshi Son is among the most recognizable entrepreneurs and investors in the tech sector. His relentless optimism, boundless risk-appetite and flamboyance translate into a life and business story worthy of a Hollywood blockbuster movie script.

Some say that SoftBank, the Japanese multinational conglomerate holding company he created in 1981, is the ultimate corporate expression of his larger-than-life personality.

Even though the founder defines the company in simple terms as “a capital provider driving the Information Revolution”, it is anything but straightforward to explain.

Son-led quarterly conference calls are known for grand statements and hyperbolic presentations. In the past, Son compared himself to Jesus Christ and the Beatles, while earnings presentations were populated with graphics of geese laying golden eggs or unicorns flying over the “Valley of the Coronavirus”. The company’s motto promises happiness for everyone through the information revolution.

Yet, on 12 May, during the latest earnings results briefing, there was not a hint of flamboyance or optimism. The mood was subdued, if not apocalyptic.

All for good reasons.

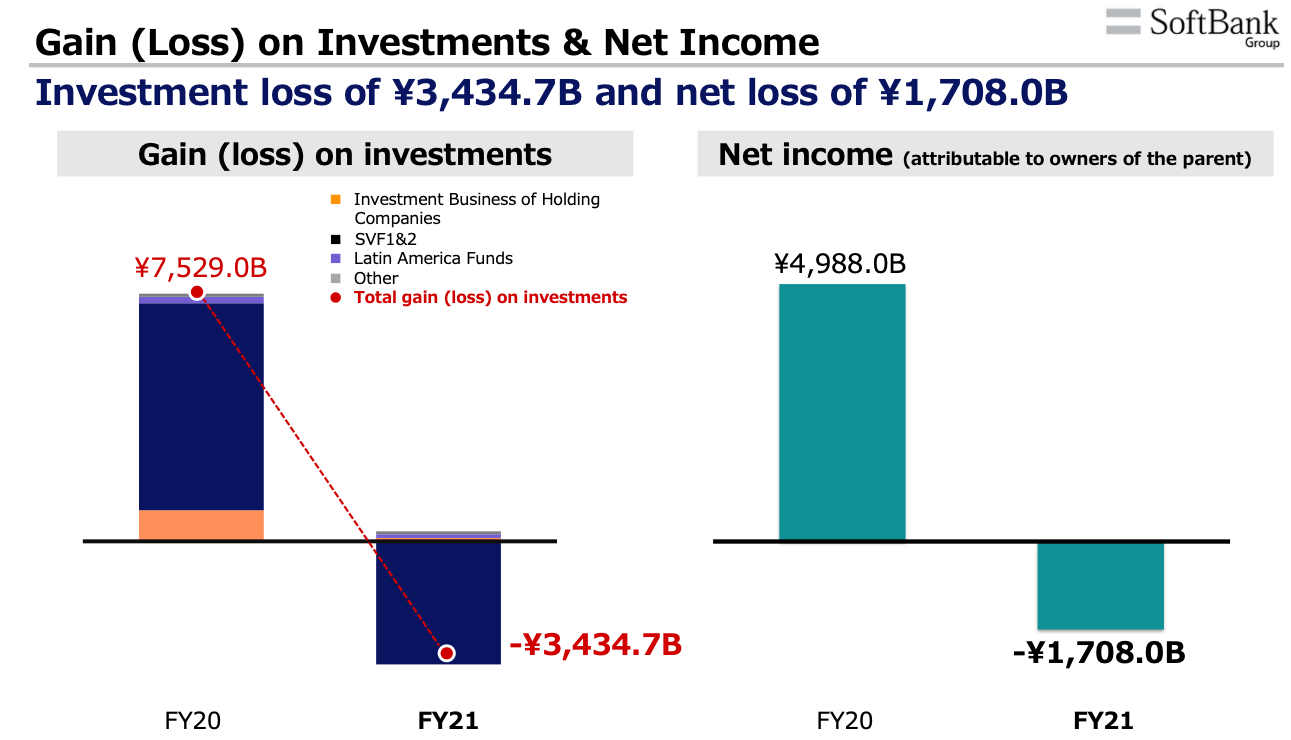

For the fiscal year ended in March 2022, SoftBank’s annual net loss amounted to a record $13 billion. Its Vision Fund lost a historic $27 billion, the largest annual loss for the group since SoftBank moved into tech investing. The company also took a $5.2 billion hit from shutting down the infamous SB North Star hedge fund, responsible for the so-called “Nasdaq whale” purchases of call options on US technology stocks that send shockwaves across the markets two years ago.

The plunge was propelled by many factors, including the US technology stocks sell-off in light of imminent rate rises, the increased Chinese regulatory crackdown on tech companies, and private markdowns.

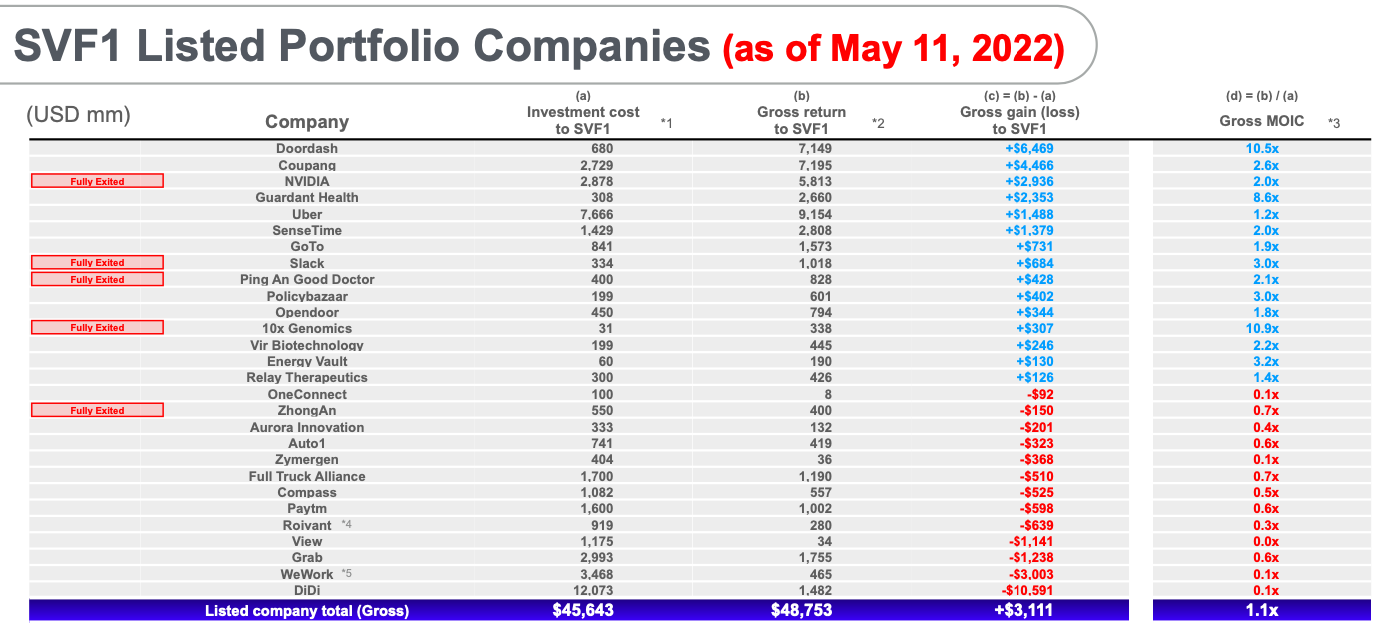

The worst performers in the quarter included their investments in Didi Chuxing (the Uber-equivalent in China that has been in the crosshair of regulators), which lost about half its value, and in Coupang (the Amazon-equivalent in South Korea), which fell about 80% since its IPO and declined 40 % this year.

On average, publicly listed companies in the Vision Fund tumbled 62% since going public. Only 3 out of 24 IPOs were able to record price increases since being listed in 2021.

The financial woes are not the end of the story. They are further compounded by managerial chaos and chronic internal clashes, resulting in a high-level executive exodus, after key people fell out with Son and left SoftBank in a string of resignations.

The most recent exit of Marcelo Claure, the Bolivian billionaire who was recruited by virtue of an acquisition of his telecoms start-up Brightstar and who quickly became a key player in Son’s inner circle, is the most high-profile.

Claure was known as SoftBank’s key “risk man”, orchestrating the rescue of any investment that went awry. He was behind the successful merger between Sprint and T-Mobile US, the revival of the work office-sharing group, WeWork, after its spectacular implosion and a key architect of the Latin America Fund, a profitable SoftBank pocket.

The exodus started with the 2016 departure of former Google executive, Nikesh Arora, followed by a succession of high-level management desertions of chief compliance, legal and communications officers, all of whom were meant to put safeguards to Son’s style of managing the company. Last year, the former Goldman Sachs banker Katsunori Sago, quit as strategy director after less than three years.

Claure, Sago and Rajeev Misra, a former Deutsche Bank trader and the head of its private investing arm, were the three executives who were regarded as possible successors to Son.

Misra is the last man standing. Known for complex financial engineering and acrimonious clashes with other execs (his worrisome tactics are detailed by the Wall Street Journal), he is credited with bringing a cohort of bankers who sank Deutsche Bank with terrible derivatives trading to help run SoftBank Investment Advisers.

Son, who is 64, has recently said that he plans to stay as the leader of the group beyond the age of 70.

Before we dissect the recent woes of Softbank, let’s first turn to its history.

The History

Son’s story prior to SoftBank (1957 - 1981)

It is not possible to understand SoftBank, without learning about Son’s unusual life story, as the two are inextricably intertwined.

Masayoshi Son was born in 1957 in a small village in Japan to a family of second-generation Korean immigrants. His entrepreneurial spirit came to the fore early in life.

At the age of sixteen, bursting with energy, Son wanted to seek guidance on how to achieve business success. So he started calling the founder and president of McDonald’s Japan. As he could not get a hold of him, he flew to Tokyo and sat in the reception until he secured a meeting. During the short encounter, he was encouraged to learn English and computer science.

With no time to waste, he quit high school the same year and flew to the US to pursue economics and computer science at UC Berkeley. While still at the university, he devised and patented an electronic translator that he sold to Sharp for $1 million. Soon after, he imported popular games from Japan, adapted them to the US market and sold them for a handsome profit. He also created a game software company called Unison World which he sold for almost $2 million.

He then moved back to Japan as a young multimillionaire, to think deeply about his next move. He devised a list of key success metrics he wanted to follow. One of them stated that he had to fall in love with his next business venture, so that he could stay involved in it for the next 50 years.

While still in the US, he came across a photo of a microchip in a science magazine which led him to believe that the world was on the cusp of a new era, where personal computers would reign supreme.

PC and software business (1981 - 1996)

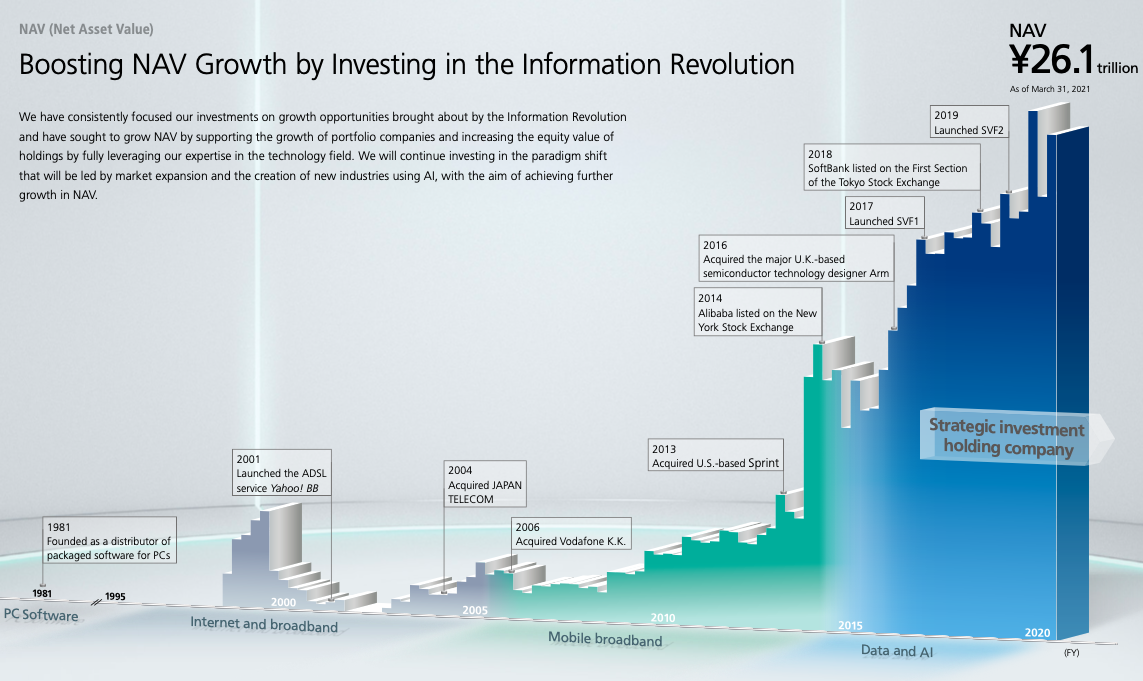

In September 1981, Son founded SoftBank. In the early days the company distributed PC software throughout Japan. But the name hinted at a much grander vision. The company was meant to become a software bank serving as the underlying infrastructure for the new Japanese information society.

Over the next decade, Son grew SoftBank’s revenue to $354 million.

As computers grew in popularity, he launched two monthly magazines entitled Oh! PC and Oh! MZ. In contrast to the magazines of the time, they exclusively targeted engineers and manufacturers and generated significant attention.

In July 1994, SoftBank began offering shares in the OTC market. Using capital raised from this offering, SoftBank acquired the events division of Ziff Communications Company, took a stake in the Interface Group which operated the world’s largest computer trade show and acquired Ziff-Davis Publishing Co., a publisher of PC WEEK.

This acquisition helped Son discover Yahoo! Inc. in the U.S. and invest $100 million for 35% of the company.

The Internet era, Alibaba and Apple (1996 - 2006)

In January 1998, SoftBank listed on the Tokyo Stock Exchange and became a pure holding company the following year.

Just before the dot-com bubble, Son made the greatest investment of his life, and one of the best tech investments of all time.

When Son met young Jack Ma, the founder of Alibaba had no business plan and no revenue. He was employing only 35 people. But Son saw the fire in his eyes and quickly determined that he had the necessary charisma to bring his vision to life. Son later said:

“I could smell him, right? We are the same animal”.

Ma noted that Son “probably has the biggest guts in the world on doing investment. Very few people in the world have that courage.” He also told the WSJ that the two never discussed business details but only spoke about a shared vision and made the decision quickly.

Son decided to invest $20 million in Alibaba. The investment paid off big time. At one point, in 2020, it was worth more than $150 billion. Following Jack Ma’s stand off with Chinese regulators and the subsequent sell-off, however, the stake is now worth under $60 billion which is still a 3,000x return on the initial investment.

Many claim this victory planted the seeds of the current turbulence, as the spectacular return emboldened Son to believe he is clairvoyant and possesses superior investing prowess. Recently there has also been speculation that the Japanese firm may need to monetize the Alibaba holding to get out of the current crisis.

For the time being, Son was riding the wave. In 2000, for three days, SoftBank reached a $200 billion market cap and Son toppled Bill Gates as the world’s richest man.

The victory, however, was short-lived. As the dot-com bubble burst, SoftBank’s shares tumbled 99% and the company nearly went bankrupt. Son lost more money than any other person on the planet with nearly $7 billion vanishing from his net worth.

Never one to despair, Son soon launched a broadband commercial service and started evolving SoftBank into a telecoms organization. In July 2004, the company acquired Japan Telecom, started operating on telecommunications networks and offered data communication services for corporate use.

In January 2005, it acquired Fukuoka Daiei HAWKS, a professional baseball team with the aim of enhancing SoftBank’s reputation and brand recognition.

Around that time, the illustrious Japanese entrepreneur spotted another trend to seize - the mobile internet. Son drew a sketch of an “iPod phone” and flew to the US to persuade Steve Jobs to create one. Jobs was already advancing the works on the iPhone but decided to give Son exclusive iPhone rights in Japan, even though he did not operate a mobile network.

Here is his depiction of the story to Charlie Rose:

“I gave [Jobs] my drawing, and Steve says, ‘Masa, you don’t give me your drawing. I have my own,” Son said. “I said, ‘Well, I don’t need to give you my dirty paper, but once you have your product, give me for Japan.’

Armed with the exclusive rights to the iPhone, Masa approached Rajeev Misra (then a banker at Deutsche Bank) and secured a $20 billion loan for SoftBank for the eventual acquisition of Vodafone Japan.

Mobile Internet (2006 - 2014)

In April 2006, SoftBank acquired Vodafone Japan to enter mobile communication. Apparently, in an attempt to dazzle Steve Jobs, Son changed the SoftBank’s logo, so that it resembled Apple’s design philosophy and reformed Vodafone’s store design for it to look like an Apple Shop. In July 2008, iPhone 3G hit the Japanese market, becoming one of Japan’s top-selling mobile devices.

More bold moves soon followed. In 2011, Son created a renewable energy business and two years later acquired the U.S.-based Sprint, rendering SoftBank a telecoms operator with one of the largest customer bases in the U.S. and Japan.

AI, IoT and Smart Robotics (2014 - present)

In July 2015, the company changed its name from SoftBank Corp. to SoftBank Group Corp., to clearly identify as a holding company. While SoftBank Mobile became SoftBank Corp.

The next big purchase came in September 2016 with the acquisition of ARM Holdings, the British semiconductor and software design company in a deal worth more than $32 billion

The same year, Son held a breakthrough meeting with Saudi Crown Prince Mohammed bin Salman. His pitch was straightforward: “give me $100 billion and I will turn it into $1 trillion”. Known for his desire to wean Saudi Arabia off oil and to shed the “dumb money” label associated with his sovereign wealth fund, MBS was quickly sold. Son would later joke that the meeting lasted for 45 minutes and the investment amounted to $45 billion, earning Son a record $1 billion per minute.

In May 2017, Son launched the first Vision Fund. $28 billion came from SoftBank, $45 billion from the Saudis, $15 billion from the UAE’s fund. Apple, Qualcomm, Sharp, Foxconn, and Larry Ellison’s family office contributed $1-3 billion each. The fund was established to invest in companies with the potential to bring about the AI revolution. It has a 12 year time horizon with a two year extension.

In December 2018, SoftBank Corp. went public. It also clearly delineated the division between the SoftBank Group Corp., the global investment company, and SoftBank Corp., its Japan-based telecoms business.

A year later, it launched a new fund focused on Latin America and the SoftBank Vision Fund 2, committing $30 billion of its own money, after failing to raise outside capital.

And it failed to raise capital from others because cracks started to emerge in the first fund with some of the high-impact implosions coming to the surface.

First came Uber. The ride-hailing company’s IPO was meant to be a big moment of triumph for SoftBank which had a 13% stake in the company. However, on 10 May, Uber experienced one of the worst opening day plunges for a company that was raising more than $1 billion.

Then the WeWork implosion followed. In August 2019, the S-1 filing revealed multiple issues regarding the company’s governance and unit economics. A month later, the company co-founder Adam Neumann was forced to resign and the IPO had to be postponed.

In October 2019, Neumann received $1.7 billion from SoftBank in a controversial exit deal brought about by the special voting rights which gave him leverage. Son was previously very close to Neumann and showered him with praise and capital but the relationship has been souring for some time. On the occasion of the exit, he told his colleagues “we created a monster, we gave him all the capital.”

The New York Times described the failed IPO as “an implosion unlike any other in the history of start-ups”, attributing much of the debacle to the easy money previously provided by SoftBank.

Concerns about the entire fund started to emerge too. Atul Goyal, an equities analyst at Jefferies said at the time “we suspect there are many such questionable investments or assets within SoftBank Vision Fund’s 80-plus investments.”

Another company that has raised eyebrows was India’s Oyo, the SoftBank-backed hotel chain. The company was one of the Japanese group’s biggest bets in India’s technology market. It burned investor cash at a rapid pace to expand globally but huge losses forced it into a painful retreat, drawing comparisons with WeWork.

In April 2020, SoftBank completed the merger of Sprint and T-Mobile and divested a portion of its shares in the new combined company T-Mobile.

2020 was also the year when the FT unmasked SoftBank as the “Nasdaq Whale”. In essence, SoftBank deployed $4 billion worth of call options to gain exposure to $30 billion worth of shares, forcing sellers of these options to buy tens of billions of dollars worth of stock and inflate their prices:

SoftBank is the “Nasdaq whale” that has bought billions of dollars’ worth of US equity derivatives in a series of trades that stoked the fevered rally in big tech stocks before a sharp pullback on Thursday and Friday, according to people familiar with the matter.

The Japanese conglomerate had been snapping up options in tech stocks during the past month in huge amounts, fuelling the largest ever trading volumes in contracts linked to individual companies, these people said. One banker described it as a “dangerous” bet.

The aggressive move into the options market marks a new chapter for the investment powerhouse, which in recent years has made huge bets on privately held technology start-ups through its $100bn Vision Fund. After the coronavirus market tumult hit those bets, the company established an asset management unit for public investments using capital contributed by its founder, Masayoshi Son.

Now it has also made a splash in trading derivatives linked to some of those new investments, which has shocked market veterans. “These are some of the biggest trades I’ve seen in 20 years of doing this,” said one derivatives-focused US hedge fund manager. “The flow is huge.”

The surge in purchases of call options — derivatives that give the user the right to buy a stock at a pre-agreed price — has been the talk of Wall Street, as the sheer size of the trades appears to have exacerbated a “melt-up” in many big technology stocks over the past few months. In August alone, Tesla’s share price shot up 74 per cent, while Apple gained 21 per cent, Google’s parent Alphabet rose 10 per cent and Amazon 9 per cent.

One person familiar with SoftBank’s trades said it was “gobbling up” options on a scale that was even making some people within the organisation nervous. “People are caught with their pants down, massively short. This can continue. The whale is still hungry.”

The entire story is also chronicled in this great blog post.

The Business Segments

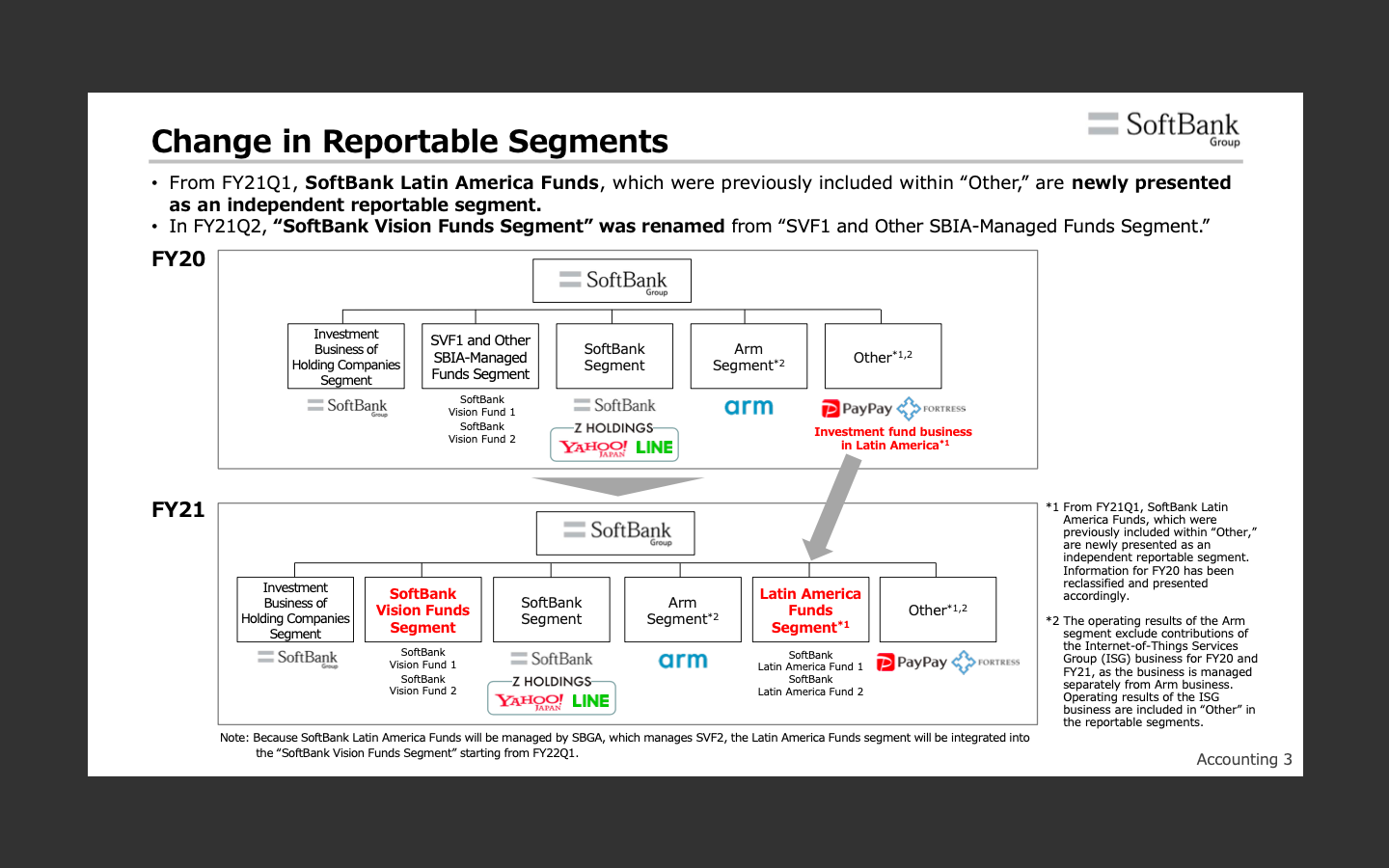

Softbank has five main segments:

1. Investment Business of Holding Companies

This segment is led by the SoftBank Group and conducts investment activities, either directly or through its subsidiaries. The companies from this segment hold approximately 120 portfolio companies, including Alibaba, T- Mobile, and Deutsche Telekom. Investees of the infamous Nasdaq Whale hedge fund SB Northstar are also part of it. What is interesting, SBG indirectly holds 67% and Son indirectly holds 33% of interests in SB Northstar.

2. SoftBank Vision Funds

This segment includes the SoftBank Vision Fund 1 and SoftBank Vision Fund 2.

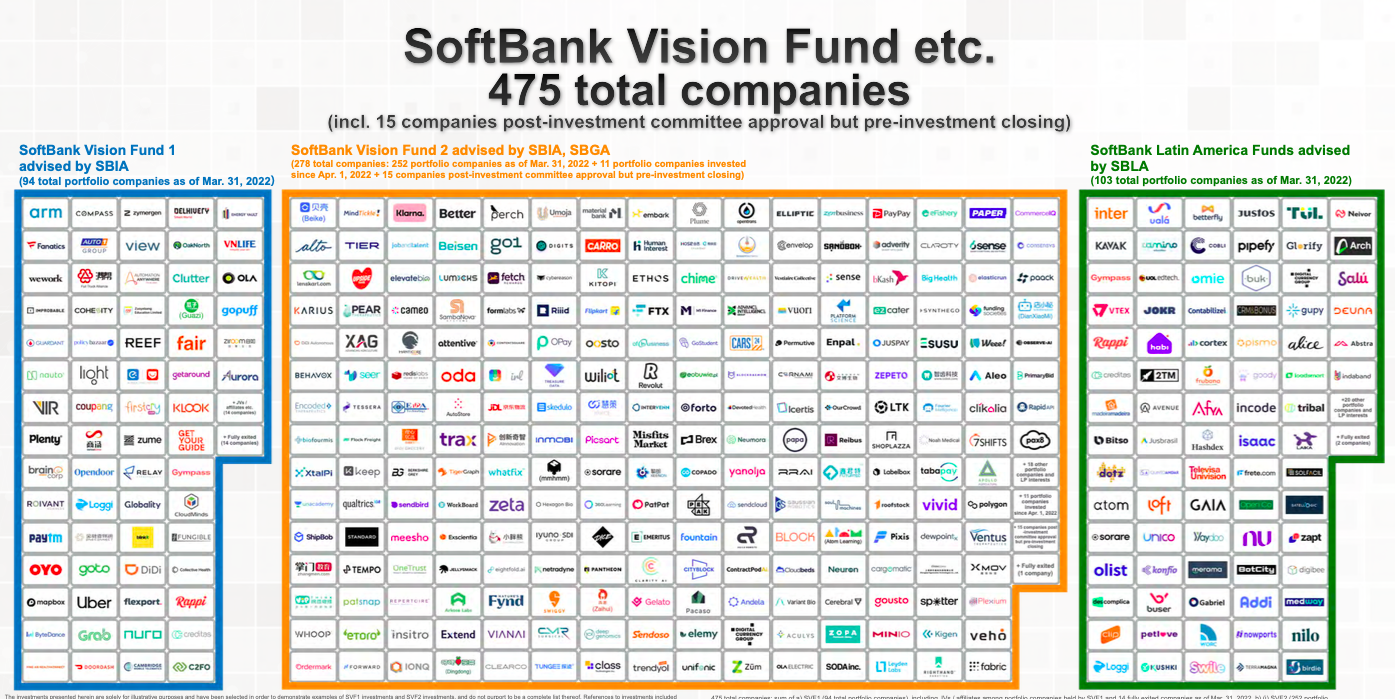

Vision Fund 1 makes large-scale investments in high-growth-potential companies leveraging AI, particularly in private companies valued at over $1 billion at the time of investment. This fund is highly concentrated in the top 10 holdings and has 94 companies in the portfolio.

The first $100bn Vision Fund became known for taking multibillion-dollar stakes in companies such as WeWork, subsidizing their heavy losses. The first Vision Fund needed to invest at least $100m per deal which limited its ability to make investments in young companies.

During the fiscal year, Vision Fund 1 made new and follow-on investments totaling $3.33 billion and sold all interests in three portfolio companies and a portion of its interests in 13 portfolio companies for a total of $18.89 billion at the initial acquisition cost of $7.95 billion.

With the second Vision Fund, the conglomerate has changed its investment approach, shying away from multibillion-dollar investments.

Vision Fund 2 is much more distributed with smaller ticket size investments across 278 tech-enabled growth companies. It made new and follow-on investments totaling $40.82 billion and sold all of its interest in one portfolio company and a portion of its interests in three portfolio companies for a total of $2.06 billion at the initial acquisition cost of $0.91 billion.

3. SoftBank

This segment includes core business activities conducted by SoftBank in Japan, such as the provision of mobile, broadband and ecommerce services and the sale of mobile devices. The main three fields include telecoms, Yahoo! JAPAN/ LINE business, and new businesses.

4. Arm

Arm is considered a separate segment. The company licenses semiconductor intellectual property, including the design of energy-efficient microprocessors and associated technologies.

5. Latin America Funds

The final segment includes the SoftBank Latin America Fund 1 and SoftBank Latin America Fund 2 which hold a total of 103 investments and are valued at $9.4 billion.

With these five segments, SoftBank is clearly divided into legacy assets and investments which are tied together by Son’s conviction of enabling an AI-driven future through aggressive, high-risk bets on entrepreneurs in the field.

Here is his philosophy on the business:

“SBG is especially keen to focus on AI, which is the most advanced component of the Information Revolution. We are proud to say that SBG is likely the largest provider of capital to entrepreneurs in the field of AI. AI is redefining every industry, including autonomous driving, healthcare, finance, education, and retail.

Just as human power was replaced by machines in the Industrial Revolution, I suspect machines will be replaced by AI in the Information Revolution. And, just as the Rothschilds played a pivotal role in the Industrial Revolution, I would hope that SBG, as a capital provider, will become a key player in the Information Revolution. This is what being a capital provider for the Information Revolution means.

In the Industrial Revolution, inventors and capital providers shared a vision to create the future. In the Information Revolution, especially the Information Revolution driven by AI, SBG will share a vision with AI entrepreneurs and aspire to shape the future together. For example, if autonomous driving using AI becomes widespread, we could see a world without traffic accidents; if medical science evolves dramatically through AI analysis, a world free of fatal diseases will be possible; and if online education using AI becomes widely available, all children can have equal access to education. In our daily lives, the way we spend money, work, and enjoy our leisure time is changing dramatically. AI is about to bring us a whole new lifestyle.

Recently, I am sometimes asked if SBG is a venture capitalist (VC). In simple terms, SBG may be a huge VC. From my perspective, however, I am not comfortable with this definition. I believe that SBG is a VC—“Vision Capitalist” that will shape the future of the Information Revolution over the course of several decades. Our corporate philosophy of “Information Revolution— Happiness for everyone” has not changed since our first day of business 40 years ago, no matter how many times our business has changed. As a capital provider for the Information Revolution and a Vision Capitalist, we will continue our efforts to make this philosophy a reality”.

Masa's mess

“If we were in a casino, he would be the guy doubling down every time he wins with his money. He never takes the chips off the table and he just lets it ride as far as he can go.” - Arash Massoudi, Corporate Finance Editor, Financial Times about Masayoshi Son

As it becomes clear from the evolution of the company since 1981, with the exception of the implosion during the dot-com bubble, most of Son’s business advanced the company in the right direction, until the Vision Fund came to being.

Son detected most of the big trends (software, telecoms, mobile internet) and made good strategic moves along the way. The kiss of death came as soon as Son took the Saudi money and created a vehicle known for a combination of excessive capital deployment, poor investment selection, bad judgment of character, a toxic, conflict-prone culture and a great deal of financial engineering.

The Vision Fund’s well-known strategy is to use capital as a weapon. It would often offer larger amounts of capital than the company was initially asking for under the threat of funding competitors, if the company declined.

It also invested in follow-up rounds at higher valuations, artificially inflating the prices. The Fund assumed that drowning companies with liquidity would allow them to outspend their competitors and elbow them out of the marketplace all the way to a winner-takes-all finale.

In many cases, however, the strategy harmed the companies because they moved away from the tactics that made them successful, as they had to pivot to unsustainable spending in order to grow.

When asked about Softbank’s strategy, Marc Andreessen, cofounder and general partner at Andreessen Horowitz said:

“Sometimes too much money is very damaging to a company right. And you can really screw up a company”.

Many of the Vision Fund’s investments were simply not good. However, there were also good companies that were damaged by SoftBank’s excessive capital deployment.

In addition to the aggressive and incessant check-writing, there is the financial engineering overlay, as spearheaded by Rajeev Misra and his ex-Deutsche Bank lieutenants.

Arash Massoudi explains:

“They wanted to basically be more effective at investing than Sequoia or Benchmark, the brand name venture capital funds. But it’s really a bunch of ex-Deutsche Bank traders who are running the show. And so what do they know about venture investing?”

As FT explains, Misra is known for populating the balance sheet with risky instruments containing multiple layers of leverage such as huge amounts of interest-bearing debt, asset-backed financing, margin loans and even preferred shares resembling debt-like products:

One of the most powerful credit traders from a pre-crisis generation of Wall Street bankers, the Indian former Deutsche Bank executive is considered by some as a pioneer of modern finance. He was feted in April by Michael Milken, the junk bond king of the 1980s who was convicted of securities fraud and later imprisoned for two years. Talking to Mr Misra at a conference, Mr Milken, now a self-styled philanthropist, said: “There is no one that has the understanding of financial markets and capital markets and the hundreds of different types of instruments that you do.”

To others, however, Mr Misra is a source of chronic instability who has stuffed the senior ranks of the Vision Fund with former Deutsche Bank colleagues and financial complexity. “SoftBank and the Vision Fund are layers of leverage upon leverage,” says one banker who has worked closely with both. This person and others see parallels to what took place at Deutsche Bank, the now struggling lender whose lack of oversight and controls saw its balance sheet laden with risky products of the sort Mr Misra specialised in.

SoftBank is saddled with $160bn of interest-bearing debt and its bonds are rated non-investment grade. The Vision Fund has a unique structure — created by Mr Misra — where roughly $40bn of outside investor funds are in the form of preferred shares that work like debt and pay an annual coupon.

When Mr Misra looked to return capital to the Vision Fund’s backers earlier this year, he added yet more leverage, taking out a $3.5bn loan mortgaged against stakes in companies including Uber.

The Financial Metrics

If we look at the financial performance in the last fiscal year, a clear picture emerges.

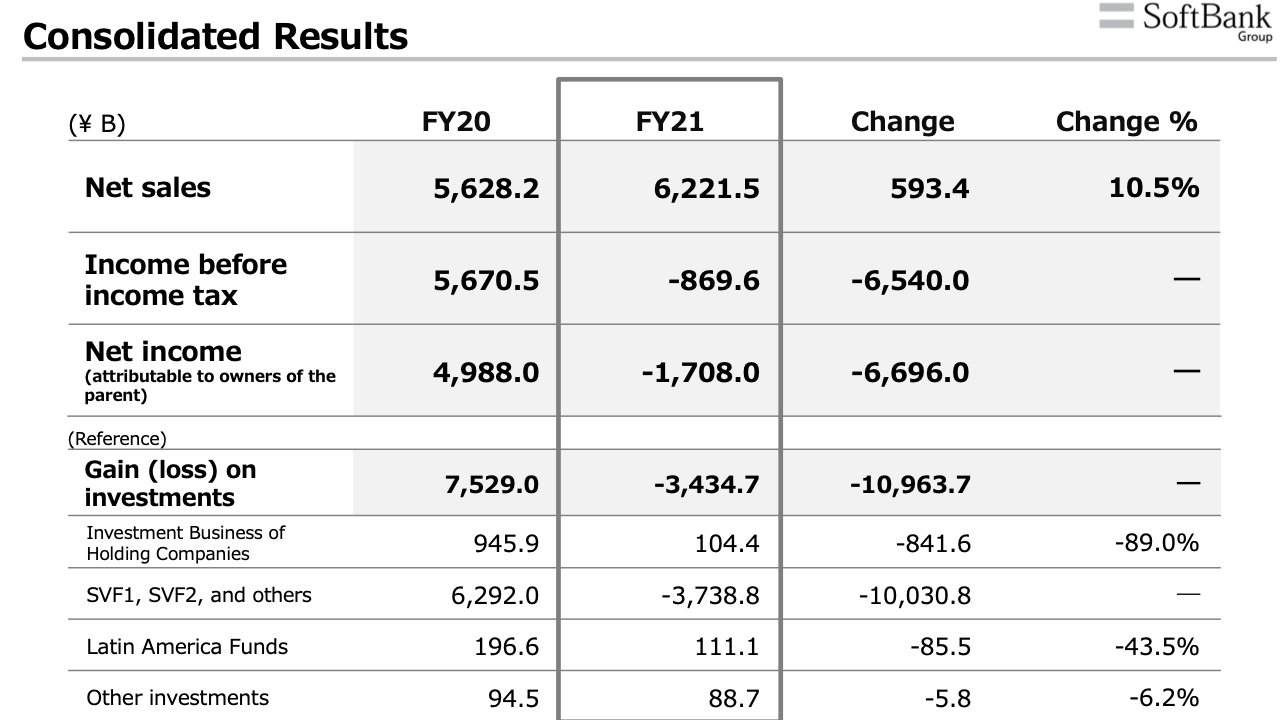

Four out of the five SoftBank segments were profitable, albeit only two (SoftBank and Arm) increased their sales relative to the previous year. However, the spectacular losses at the Vision Funds took the entire conglomerate well into the red.

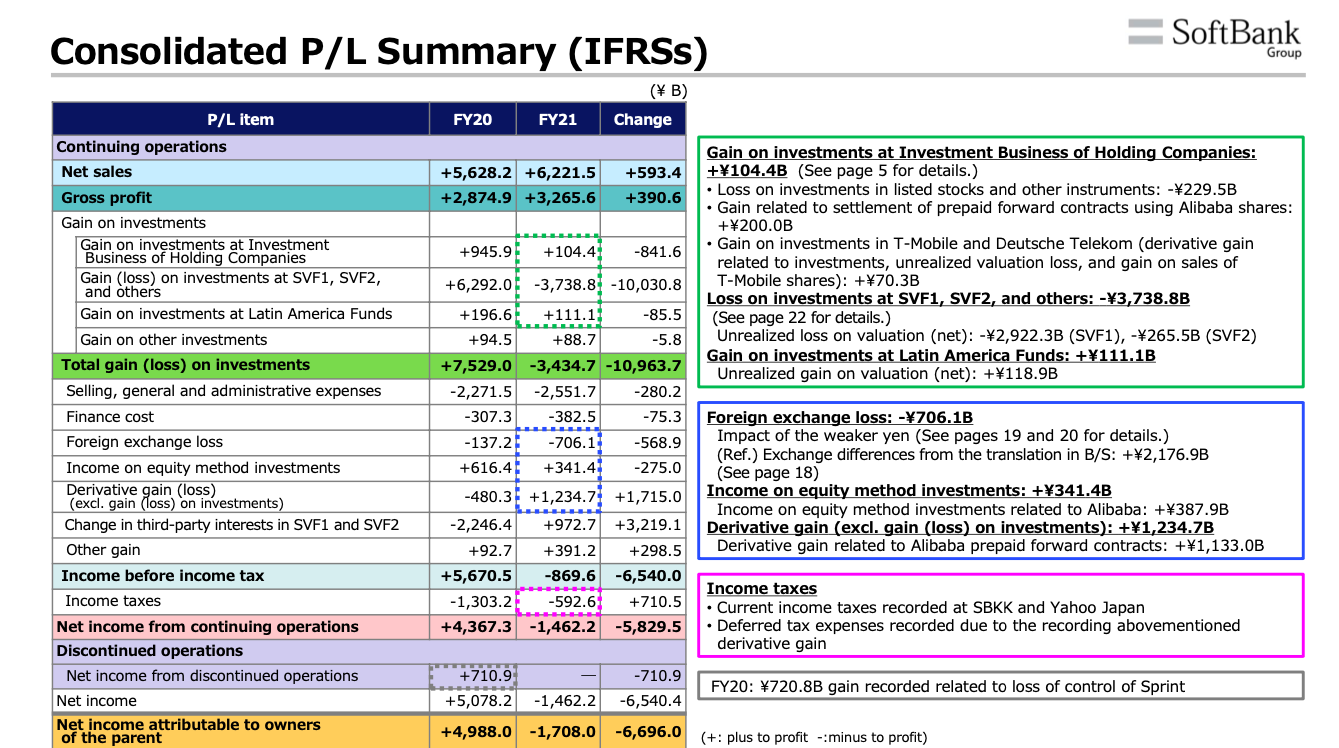

Its staggering ¥3,738 billion ($27 billion) loss in investment resulted in an overall annual net loss totalling ¥1,708 billion ($13 billion) for the owners.

The first segment (Investment Business of Holding Companies) recorded an investment gain of ¥104,362 million, largely thanks to the settlement of forward contracts on Alibaba shares (gain of ¥199,972 million), selling of T-Mobile shares and derivative trading on T-Mobile and Deutsche Telekom (gain of ¥70,307 million) and a $1.25 billion non-refundable deposit from NVIDIA for the sale of all Arm shares which eventually collapsed. Segment income stood at ¥965.9 billion. On the other hand, the Company recorded a loss of ¥229,504 million on investments in listed stocks and other instruments.

The second segment is where things turned ugly. Investment loss here amounted to ¥3,738,825 million.

Vision Fund 1 recorded unrealized net loss on valuation totaling ¥3,632,168 million for listed portfolio companies. The largest losses came from Coupang (¥1,645,327 million) and DiDi Global ( ¥911,412 million).

The plunge reflected a decline in the share prices of most of listed portfolio companies due to regulatory tightening, and a sell-off in high-growth technology stocks led by the anticipation of higher interest rates.

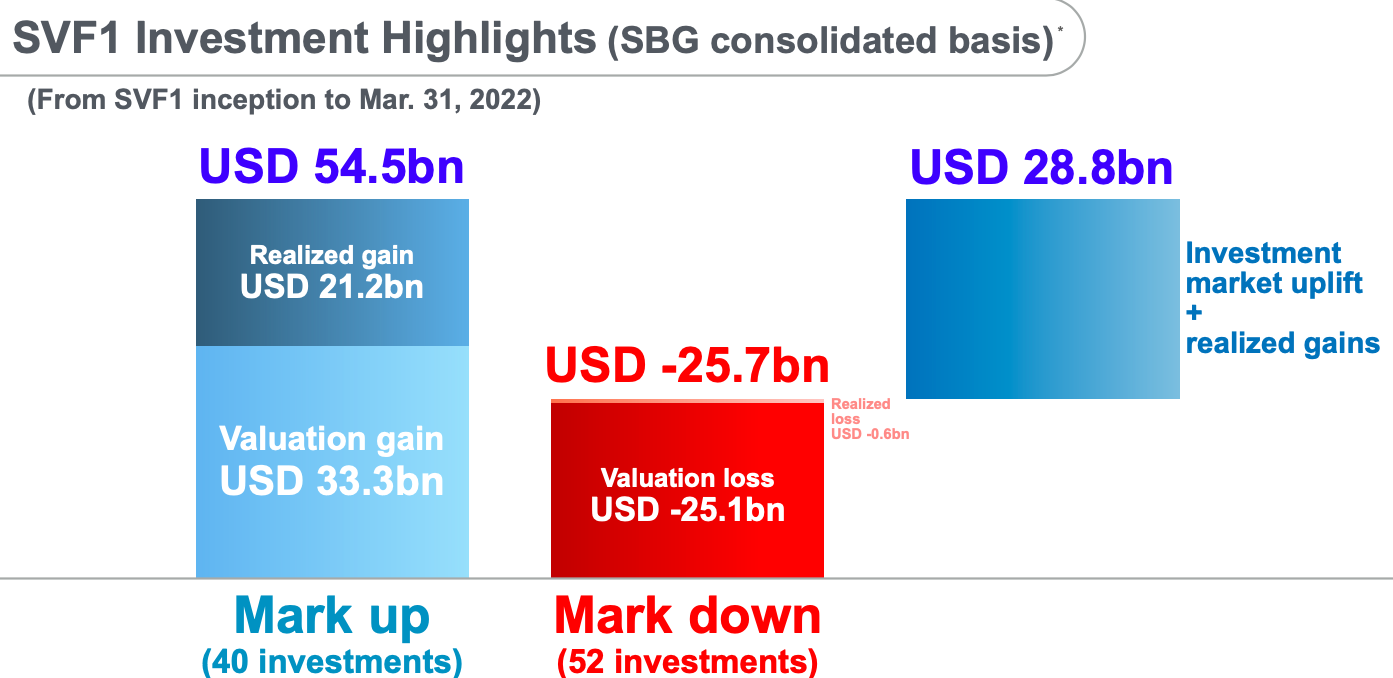

For private companies, Vision Fund 1 recorded an unrealized net gain on valuation of ¥709,833 million. Values of certain portfolio companies increased following successful funding rounds but many were also written down.

Overall, the cumulative gross gain since the Fund’s inception was $28.75 billion, including cumulative realized gain of $18.14 billion, cumulative derivative gain of $1.48 billion, and cumulative dividend income of $0.94 billion.

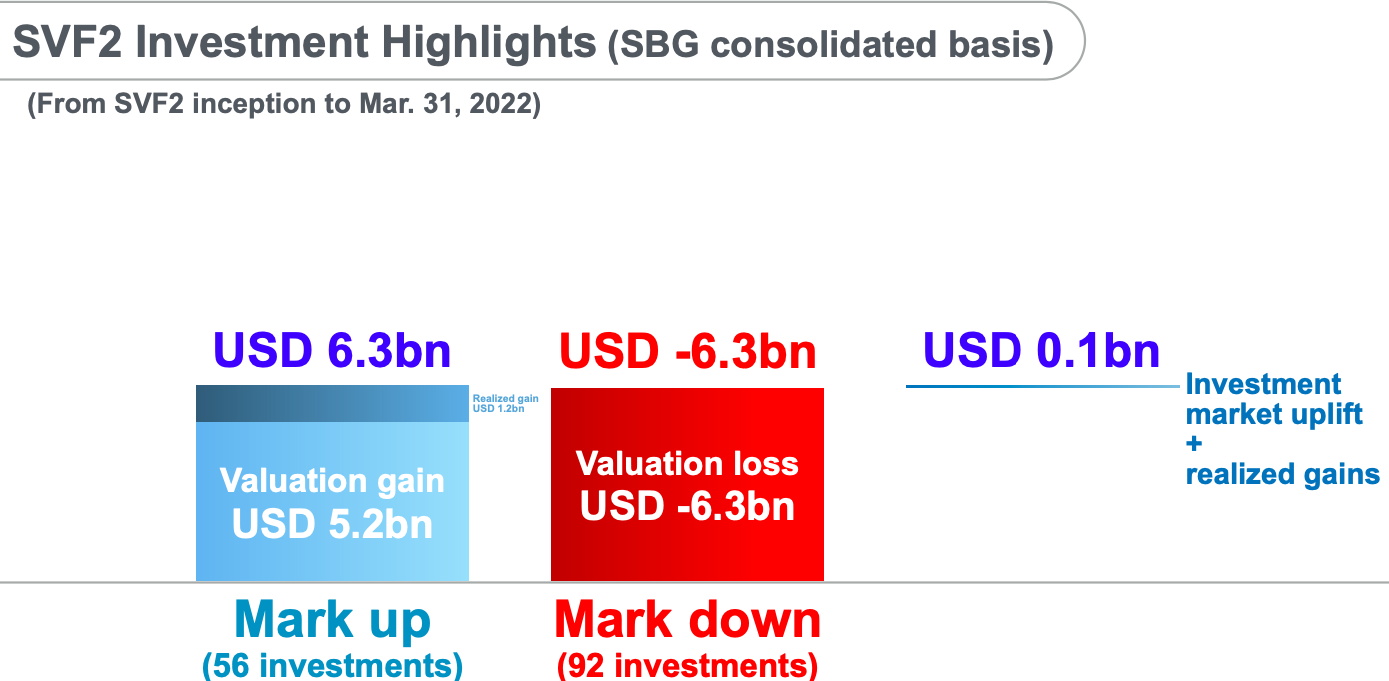

Vision Fund 2 realized a gain on investments amounting to ¥128,577 million, thanks to the partial sale of its investment in KE Holdings. In addition, the Fund recorded an unrealized net loss on valuation of ¥265,476 million, due to a decline in the share price of KE Holdings. Fair values of unlisted portfolio companies declined, while the share price of AutoStore Holdings which went public in the third quarter increased.

Cumulative gross gain since the Vision Fund’s inception was $0.08 billion, including cumulative realized gain of $1.11 billion and cumulative derivative loss of $0.42 billion.

Net blended IRR for both funds since inception is 10%.

The next two segments are the only two that grew relative to the prior year.

In the third Softbank segment, income increased by 3.8% year-over-year. Here, the Yahoo! JAPAN/ LINE and enterprise businesses increased their income, while gains on investments were offset by a decline in income in the consumer business and an increased loss on equity method investments.

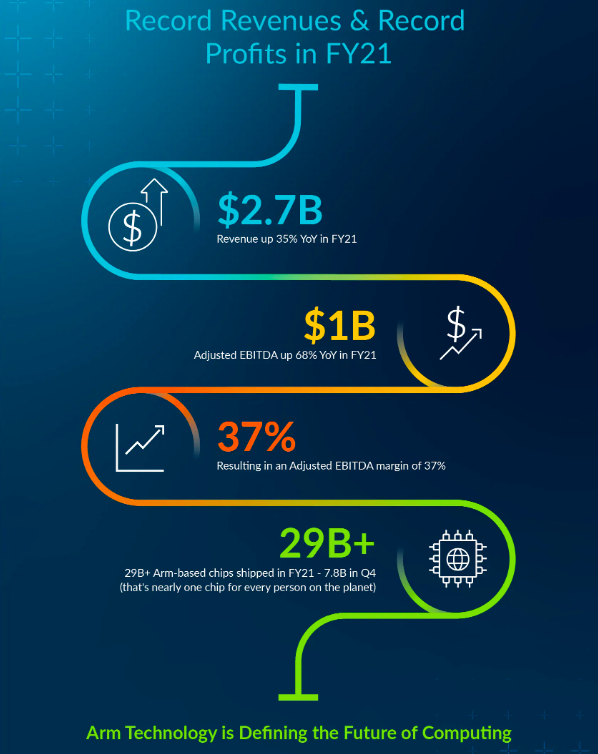

The fourth segment, Arm is the brightest spot on the SoftBank map. While SoftBank sunk to the largest ever loss, Arm reported record annual revenue of $2.7bn for an increase of 35% from the year prior. Net sales increased by 43% year-over-year and adjusted EBITDA margin was 37%.

Arm’s technology royalty revenue increased by 20% year-over-year, while technology non-royalty revenue increased by 61% thanks to the availability of Arm’s newly developed products. The increase came as a surprise to many, after years of mediocre performance.

More Arm customers chose to adopt Arm’s latest technology for their next generation products and services, helped by strong growth of 5G smartphones, ADAS and IVI chips going into cars, and price increases in 32-bit microcontrollers. Arm shipped a record 29.2 billion chips in the fiscal year and has a huge computing footprint.

In the fourth quarter, Arm also signed licenses for its CPU and GPU IP that the company’s customers will use in a wide range of markets, including automotive vision systems, networking equipment, servers and smartphones.

Rene Haas, Arm’s CEO said the following:

“Our record results demonstrate that the demand for Arm technology and the strength of the Arm ecosystem has never been greater – our compute platform will power the next set of technology revolutions across cloud computing, automotive and autonomous systems, the IoT, the Metaverse and beyond. As we look ahead to a future built on Arm, our priority is to continue to deliver on our business strategy, enable partners with the solutions they need through further investment in our roadmaps and engineering talent, and together with our ecosystem redefine the future of computing.”

In the final segment, the Latin America Funds gained ¥111,070 million. Unrealized net gain on valuation of investments totaled ¥118,922 million, thanks to an increase in unlisted portfolio companies, such as QUINTOANDAR, LTD., Kavak Holdings Limited, and Creditas Financial Solutions, Ltd. Share prices of listed portfolio companies such as Banco Inter S.A. and VTEX declined. Its net blended IRR since inception is 32%.

Given the complexity and the scale of the business, SoftBank monitors three financial metrics very closely. These include:

- Net Asset Value (NAV) which is the equity value of holdings minus net debt.

- Loan to Value (LTV) which is net debt divided by the equity value of its holdings.

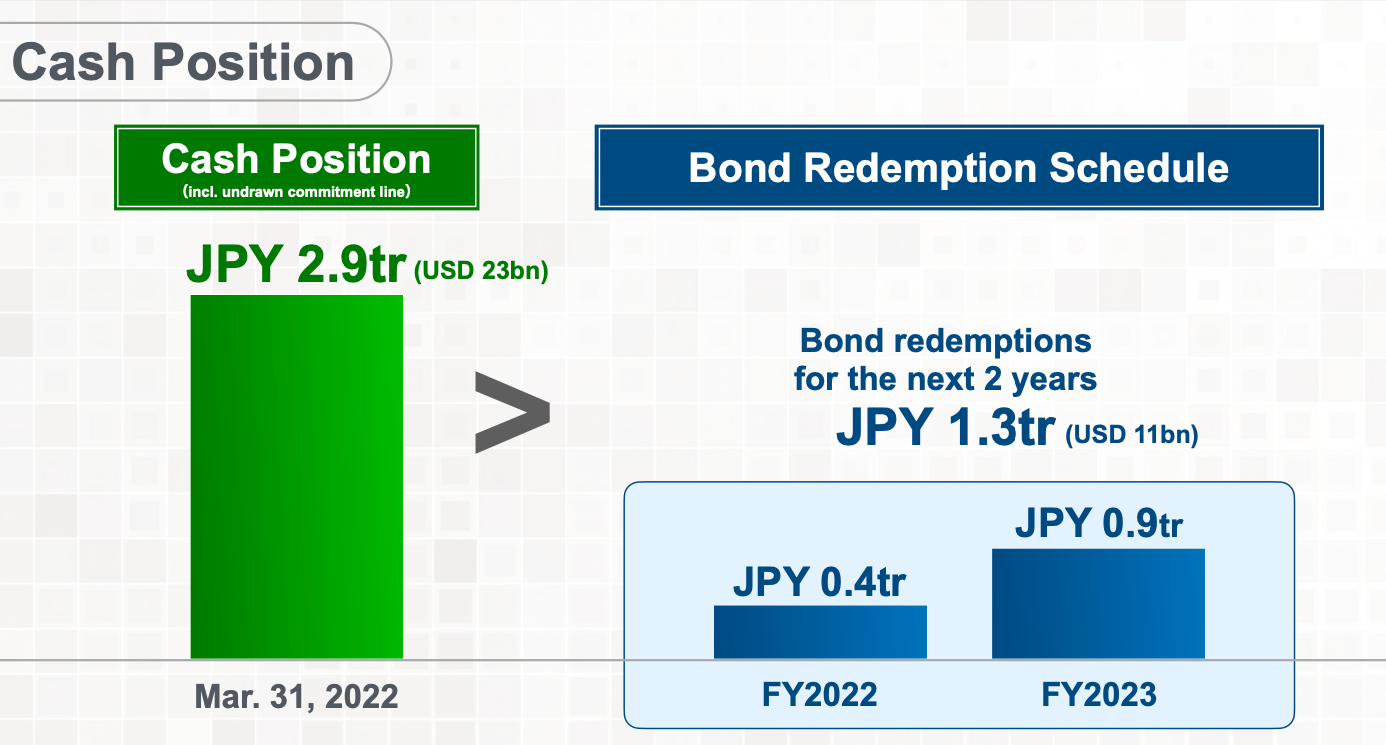

- Cash position which is meant to cover bond redemptions for at least two years.

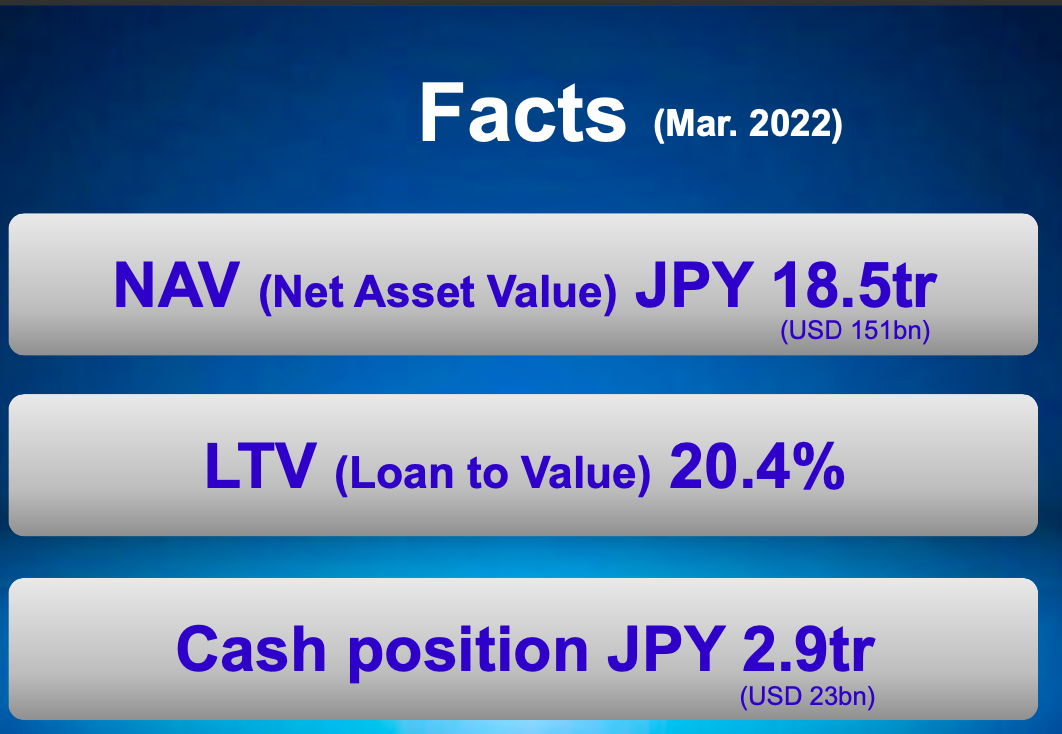

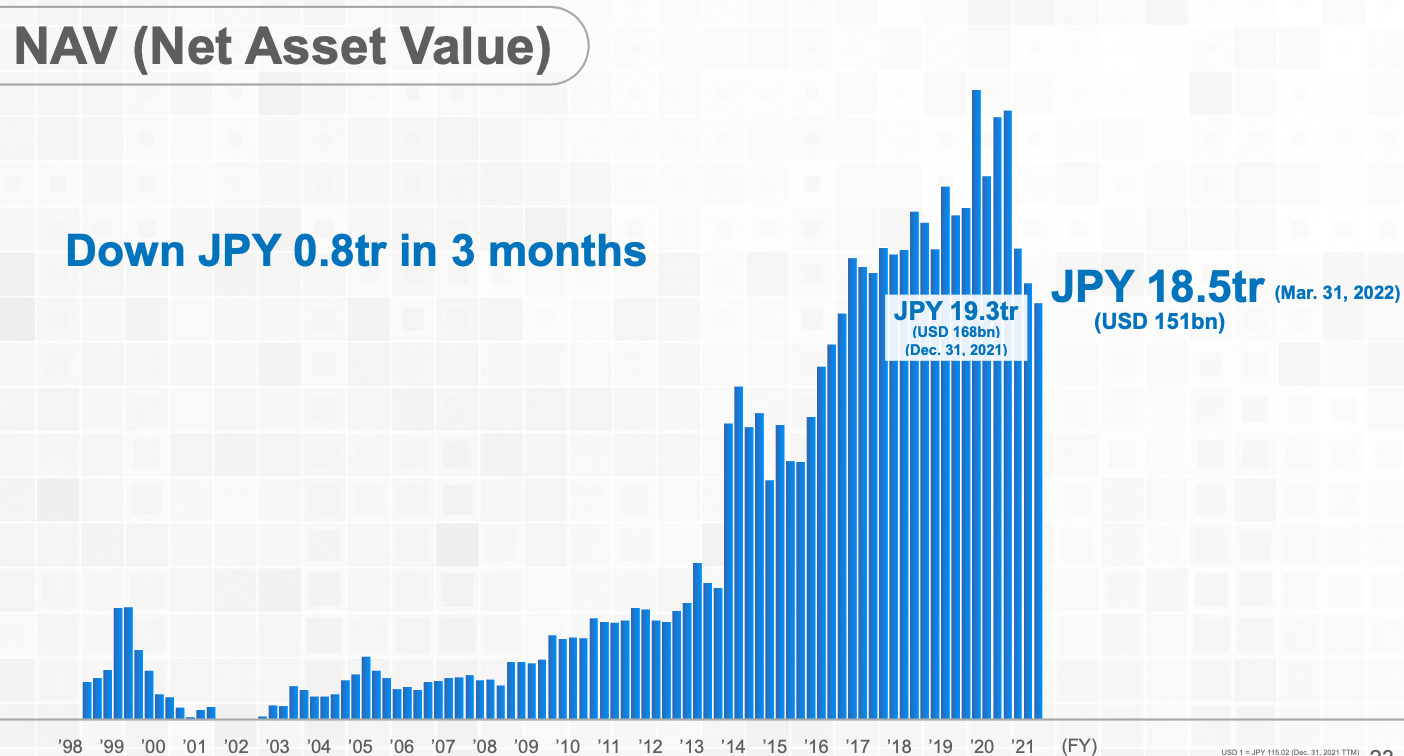

Net Asset Value

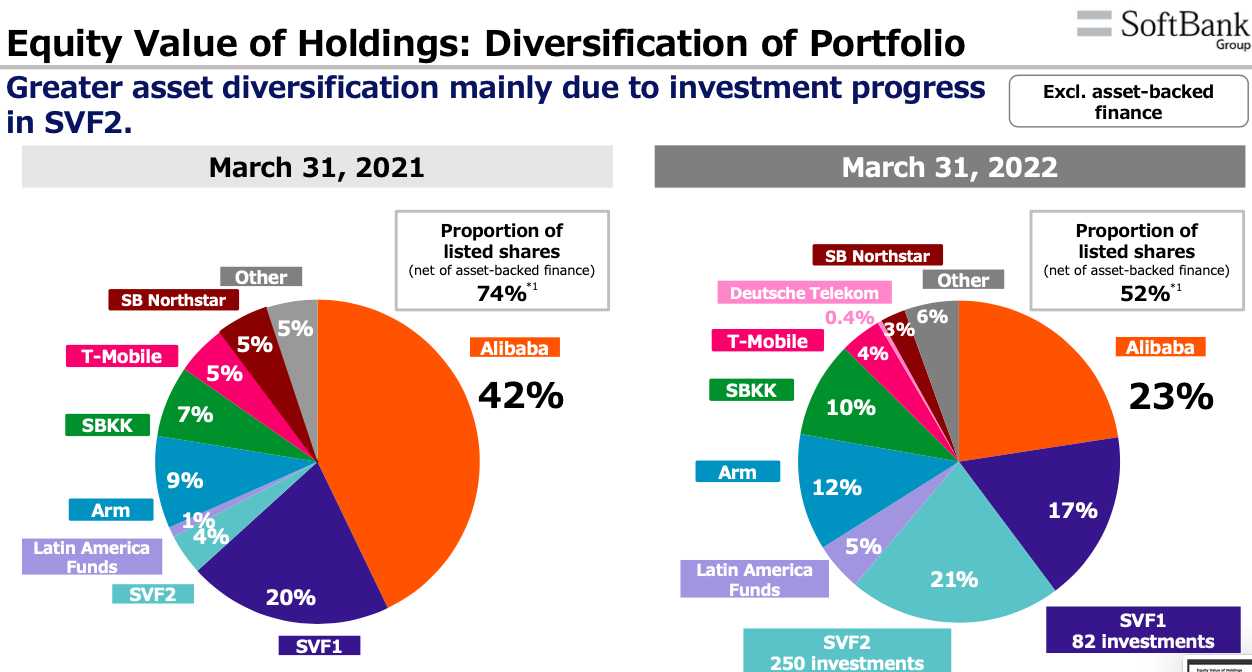

As a result of the large losses at the Vision Funds (which constitute 49% of SoftBank’s NAV), the Net Asset Value decreased by 11% year-over-year from $168 billion to $151 billion. This means that with a market cap of $68 billion, the company is currently valued at around 45% of its NAV.

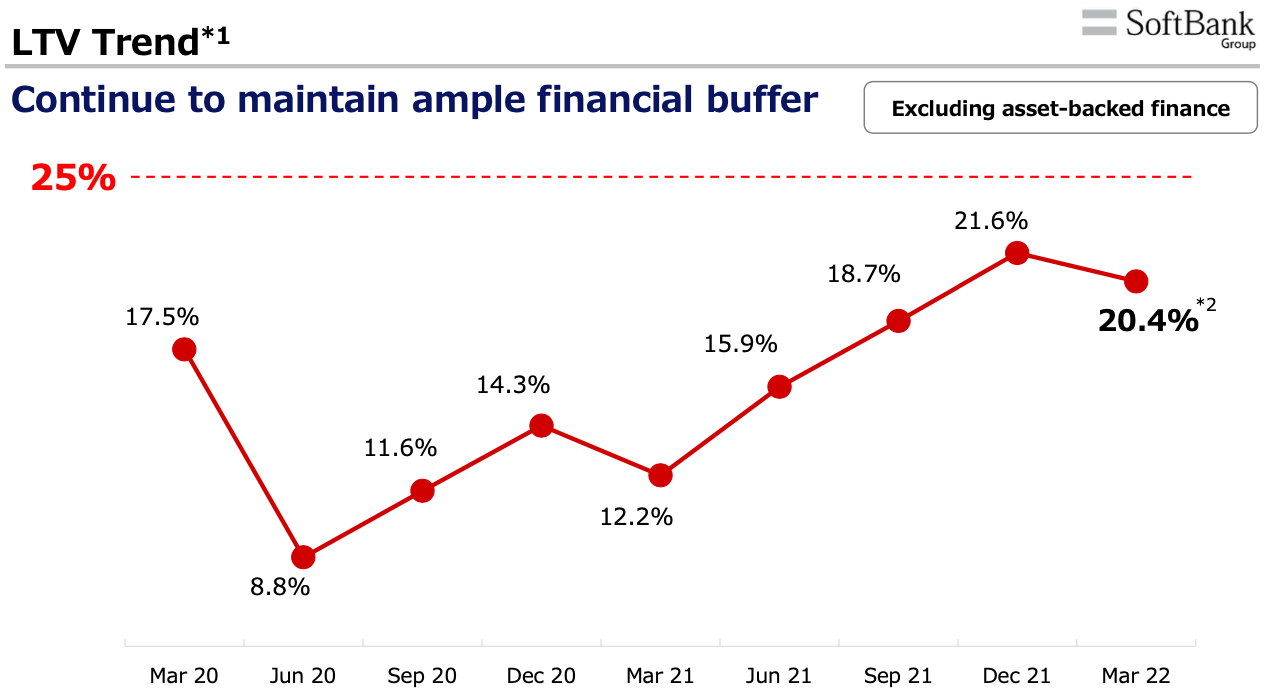

Loan-to-Value

Given that Son has personal borrowings against SoftBank shares, he closely monitors the LTV as a gauge of the company's financial health.

SoftBank has a self-imposed limit on the loan-to-value ratio which stands at 25%. This metric only reflects conventional debt and does not include asset-backed financing.

Son has vowed never to cross this threshold in normal times. However, S&P Global Ratings said it expects SoftBank to manage the ratio at about 30%. The ratio spiked from 12.2% last year to 20.4% at year end. The closest it ever flew to the sun was in the previous quarter when it reached 21.6%. To improve the ratio, the company sold many assets and undertook share buybacks.

Cash position

Another key aspect to SoftBank’s health is liquidity. The company has $23 billion of cash on its balance sheet. The goal here is for the conglomerate to be able to cover its bond redemptions for the next two years which stand at $11 billion.

Recently, the chief executive of Mizuho, Softbank’s main lender said:

“SoftBank properly controls its loan-to-value ratio and it also has a cash position covering bond redemptions for at least the next two years, so at this point, we don’t think there’s any issue. Of course, we are analysing each other carefully. But I am totally unconcerned about this.”

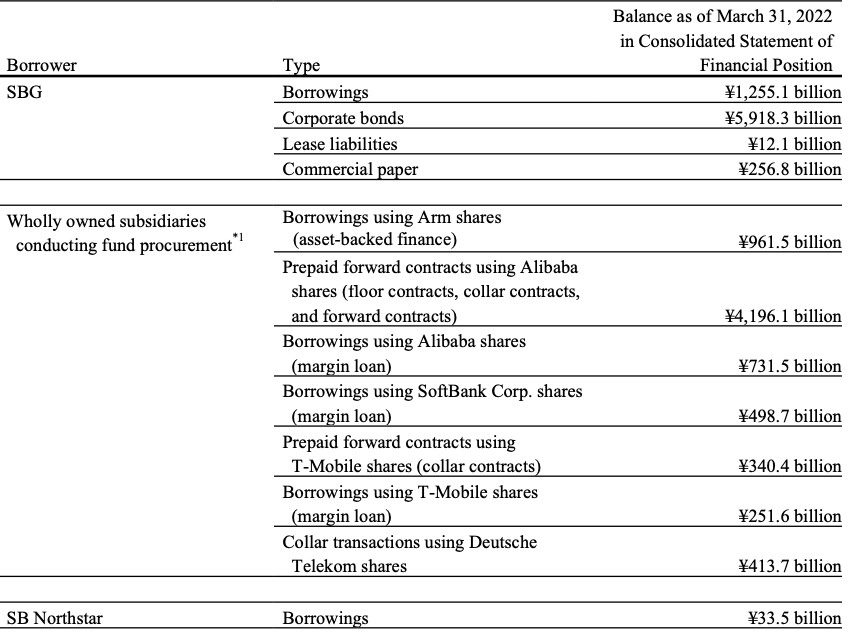

Asset-backed funding

But these three metrics are not the end of the story. In its quest to fund new investments, SoftBank has raised tens of billions of dollars backed by its shares in Alibaba, Arm, Deutsche Telekom, T-Mobile, and other listed holdings.

This so-called asset-backed funding is a complex financial arrangement using a mix of derivatives and loans and is excluded from the LTV calculation.

For example, at the end of 2021, asset-backed financing using Alibaba stock was valued at about $25.8 billion or 35% of SoftBank’s Alibaba holding.

Given all the recent capital constraints, many investors have been observing whether SoftBank intends to sell its stake in the Chinese ecommerce giant, its Japanese telecoms unit, or any other legacy asset.

However, in light of the asset-backed funding, any divestitures would mean that SoftBank could no longer borrow against these shares to fund fresh investments. On top of that, the telecoms business is a steady cash generator for the group and selling Alibaba shares at a fraction of their peak value could also be problematic for Son.

One more issue worth highlighting in this setup is that in addition to standard interest bearing debt, SoftBank has margin loans amounting to $6 billion.

FT reported that when Alibaba’s shares dropped to $73, SoftBank came very close to a margin call on the loan against Alibaba and if it wasn’t for the Chinese regulators stepping in, it would end in a “lights out” moment for Son’s company.

Softbank then commented:

“We do not comment on individual financing details. The balance of margin loans is $6bn, which is not a concern considering its proportion within our group’s total asset-backed financing, as well as liquidity on hand (¥2.9tn as of March 2022),”

What’s next

When Son had to unveil the record loss, his presentation started with a sign that said mamori which means to defend or protect. “We put up an umbrella when it rains,” he said “It is the time to strengthen our defence now.”

What this means in practice is that, in the short-term, SoftBank will put in place three interconnected tactics:

- Reduced pace of investments

- Continued Monetization

- Share Buybacks

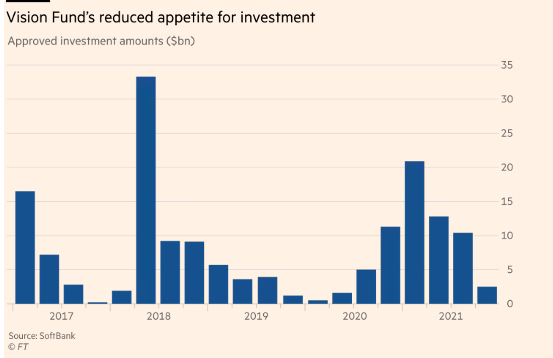

When it comes to scaling back the investment frenzy, Son announced that in the next twelve months, SoftBank would be reducing the velocity of investments by half or even 75%. He also said that currently it is not a good time to invest in the private market, given the inflated valuations relative to the public market in light of the sell-off. He also mentioned that SoftBank has increased its investment expertise by hiring experts in different fields rather than rely on generalists.

Here is what he had to say on these matters during the last earnings call:

“We would reduce the pace of investment compared to last year, probably half or one quarter of last year’s, but we are not saying which quarter would be how much. It depends on the situation. Overall, 12 months looking forward, we would be reducing to by half or 75%. That will be the case. With that, when we liquidate the other assets, we have enough room for improving many things or share buyback.

Right now we are checking every company, their multiple comps are too expensive compared to the public market because the public market went down. Now is not the time to invest at today's valuation of the private market. We just wait for the right valuation to come down.

We have dedicated about 30 teams depending on geography or subjects. We have developed more expertise for each specific field whereas most VC firms have small numbers of partners or are more generalists. We have more specialists for each segment of industries and geography. Geography‐wise, the U.S. is still the center, but we are looking at worldwide”.

Secondly, SoftBank continues to monetize its assets to increase the cash position. In the last 12 months, the company sold $50 billion worth of shares and will, most likely, continue to sell at similar scale going forward.

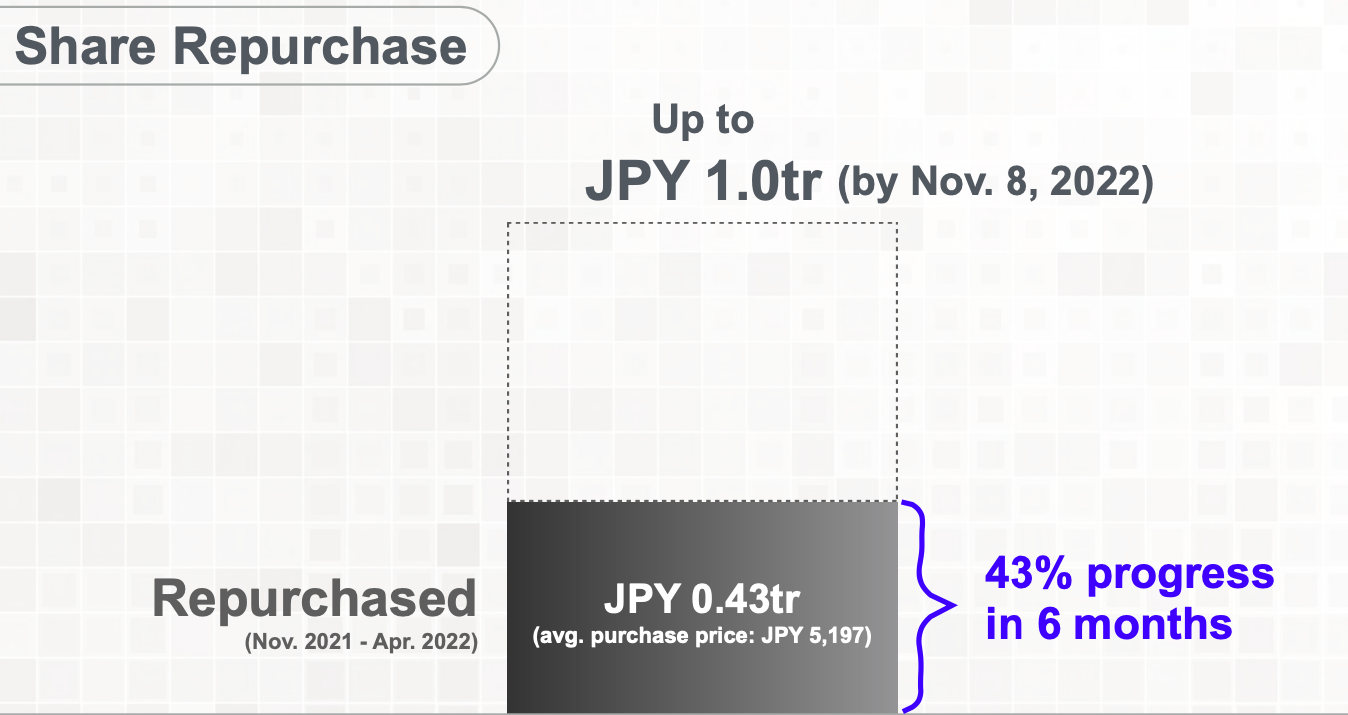

The third part of the package includes share buybacks. The plan here is to complete ¥1 trillion worth of buybacks by November. However, the execution here will also depend on maintaining the LTV ratio at tolerable levels.

Arm IPO

SoftBank is planning to list Arm on the Nasdaq after the sale to chipmaker Nvidia has collapsed. The company has also made big progress to reign in the renegade China unit headed by Allen Wu who has been entangled in a vicious dispute with the company. The inability to audit Arm China was the last obstacle to the IPO which has now been removed. SoftBank would keep the majority stake in the company after the listing. In light of the company’s strong performance, it is one of the last rays of hope for the conglomerate.

As the Fed is taking away the punch bowl and financial conditions tighten, SoftBank is not the only company suffering historic losses. Many big name long tech companies are sharing the same fate. Chase Coleman’s Tiger Global lost $17 billion this year, while Baillie Gifford’s Scottish Mortgage is down 9.5%.

Masayoshi Son often proved able to spot big trends he later monetized. As the digital transformation and the marriage between quantum computing and life sciences continue, his thesis on AI can still prove to be right.

He has once survived a 99% dot-com bubble plunge and came out stronger on the other side. The next 12-24 months will show whether he can do it again.