Snowflake: Product, Business Model, Competitors

Sign up for ARPU: Stay informed with our newsletter.

For this week, we will look at Snowflake by dissecting its value proposition, its go-to-market strategy and consumption-based business model. We will also analyze key business metrics and the growth trajectory of this business that got Berkshire Hathaway interested.

Without further ado, let’s dive in!

What is Snowflake

First, a bit of industry context. The average enterprise has 300+ custom applications deployed today to run their business processes, and each application is structured with a unique set of requirements for its use cases and its users. These applications might be run in the cloud or on-premise with unique and separate databases, and quite often do not talk to each other.

Against this backdrop, Snowflake was built to become a cloud data platform that allows large companies to take their data from different sources, migrate it to the cloud, store it in one, safe place, and then use it to gain business insights, build data-driven applications, and share it inside and outside their organizations.

The company was founded in 2012 by two ex-Oracle data architects Benoit Dageville and Thierry Cruanes and a co-founder of a Dutch start-up called Vectorwise, Marcin Żukowski. The business was dead in the water for two years until Bob Muglia, an ex-Microsoft executive came on board as CEO to raise $26 million in capital and land 80 strategic customers, including Adobe, CondeNast and White Ops.

In 2019, Frank Slootman became Snowflake’s CEO, quickly taking charge of the company’s hypergrowth mode. He is well known for steering Data Domain through an IPO to its acquisition by EMC for $2.4 billion and leading ServiceNow from around $100 million in revenue to a public company generating $1.4 billion. His distinct leadership style has attracted considerable media attention, while his book Amp it Up is a revered classic in Silicon Valley circles.

In 2020, the company went public in one of the largest software IPOs and is currently valued at over $40 billion.

Initially, Snowflake started as a cloud data warehouse and enabled a lot of companies to conduct first gen cloud migrations. For non-technical readers, it is important to note the difference between a database and a data warehouse. Databases are organized collections of stored data. Data warehouses are information systems that sit on top of various data sources, including databases, for the purpose for data analytics.

Snowflake was created to solve the issue of data silos that most companies were (and still are) struggling with. At the time, existing databases were not designed to compile data in one place and to run smooth analytics on top of it. Different data buckets existed in fragmented patchworks. Companies would need to spend a lot of money and IT resources to stitch this data together for these buckets to play well with each other.

Then, setting up underlying hardware and software to query this data was not only costly but resulted in a slow and restrictive process. On top of that, as storage and compute resources increased, more capital and oversight from technical staff was required. Frequent outages and time-consuming maintenance caused delays and diverted resources from high impact initiatives.

Snowflake was able to address all of these by bridging data silos, removing data management and infrastructure complexities, improving the price-to-performance ratio and centralizing data in an analytics-ready format. Companies could then query this data quickly without any friction.

Interestingly, Snowflake succeeded where hyperscalers failed, often getting involved after Amazon, Google and Microsoft flopped. The company was able to achieve this, as it has co-written good tooling to translate the proprietary language the code was stored in and, on top of that, was able to get the new cloud system to work.

Snowflake was also one of the pioneers of an early paradigm shift, where the data warehouse and data lake (i.e. a vast pool of raw data for centralized data sharing that enables data scientists to extract new insights) blended into a data lakehouse that ensured there was just one copy of data for multiple workloads.

Once companies had their data in the cloud, Snowflake quickly focused on data sharing which allowed companies to share data within organizations, as well as with their partners, customers, and suppliers, without moving the underlying data. It also helped companies purchase ready-to-query third-party data sets on its marketplace and commingle existing data with broader context to gain deeper insights.

Currently, the company is focused on enabling developers to write applications directly in Snowflake, through Snowpark which enables developers to interact with Snowflake through popular programming languages on top of a SQL-programming model, providing companies with choice and saving them the need to learn new skills or hire new talent. It has also recently acquired a company called Streamlit to double-down on this process.

There are two additional benefits Snowflake prides itself on. First, the product is easy to use, so you do not have to be a tech mastermind to operate it. Second, Snowflake offers robust security and governance. It knows exactly who is accessing what, tightly controls data access (known as data masking) and encrypts data in transit and at rest.

Snowflake’s platform is built on a cloud-native architecture consisting of three integrated layers across storage, compute, and cloud services.

The storage layer allows companies to ingest large amounts and varieties of structured, semi-structured, and unstructured data to construct a unified data record. The compute layer enables users to simultaneously access data sets for many use cases with minimal latency. The cloud services layer optimizes each use case’s performance with no administration.

This architecture is built on three major public clouds (AWS, Azure and GCP) across 31 regional deployments around the world, so organizations can optimize for the best features and not rely on a single provider.

As you may have guessed, Snowflake’s integrated, end-to-end solution enables nearly limitless use cases across data warehousing, data lakes, data engineering data science, data application development and data sharing.

Data engineers can import and manage data or pull datasets from other sources. Analysts can track key business metrics, whereas data scientists can deploy ML for further insights. Developers can build data-driven apps, data brokers can sell datasets on the marketplace, while sales and marketing teams can elevate their game through enhanced analytical capabilities and better targeting.

Let’s have a look at a few examples.

KFC is using Snowflake to collect data from the company's mobile app, the KFC website, and in-store point-of-sale terminals to gain an insight into its customers’ ordering habits, build customer profiles and, ultimately, improve its service.

Vimeo ingests and analyzes billions of streaming events per day to identify customers requiring additional bandwidth and then to develop upsell campaigns for them. Vimeo’s marketers, on the other hand, use the data to improve targeting, manage acquisition costs, and build look-alike audiences for better campaign performance.

Finally, one of the most interesting use cases is in the ad tech space where Snowflake’s clean room technology allows partners to securely join first party data without exposing their customers’ IDs. Disney Advertising Sales recently developed its own clean room called Disney Select, where brands that advertise on Disney can gain access to more than a thousand user segments built from Disney’s intelligent data set to ensure better targeting.

How Does Snowflake Make Money

Snowflake has a consumption-based business model, as opposed to traditional subscription-based software companies that recognize revenue ratably over the contract term.

This means Snowflake’s customers can consume the platform under (i) capacity arrangements with a term of one to four years, where they commit to a certain amount of consumption at specified prices, charged annually in advance or (ii) on-demand arrangements charged monthly in arrears.

When consumption exceeds the initial capacity commitment, customers can amend their existing agreement or request early renewals. When consumption is lower than anticipated, customers can roll over unused capacity to future periods, upon the purchase of additional capacity.

The difficulty of this model is that Snowflake does not have visibility into the timing of revenue recognition and has a hard time predicting revenue. In addition, Snowflake constantly improves features to make the platform more efficient which enables customers to accomplish the same workloads with fewer compute, storage, and data transfer resources. If these improvements do not result in increased workloads down the line (which the management is very confident it will), they can lead to lower revenue.

The upshot is that once customers realize the benefits of the platform, they typically increase consumption by processing, storing, and sharing more data, leading to higher top-line.

In this model, Snowflake derives revenue from:

- Fees charged to customers who consume storage (average terabytes per month stored), compute (type of compute resource, duration of use or volume of data processed) and data transfer resources (terabytes of data transferred). These three resources are offered as a single, integrated package.

- Fees for professional and other services such as consulting, on-site technical solution services, and training related to the platform.

- Annual, ratable deployment fees to gain access to a dedicated instance of a virtual private deployment.

Snowflake’s go-to-market strategy is to acquire new customers and drive increased platform use for existing customers, primarily through a robust and expansive direct sales force which offers vertical-specific solutions and goes after large organizations with vast amounts of data.

Snowflake has a sizable army of sales reps aggressively targeting C-level executives at Global 2000 companies to dazzle them with their product. Sales personnel has been growing fast, increasing from 1,257 employees in 2021 to 1,891 in 2022. In February 2022, Snowflake has also verticalized part of its selling motion to address the largest customers by industry.

Frank Slootman is known for running high velocity sales operations at massive scale and leaning in as hard as possible to discover the limits of the growth model.

Here is his philosophy on the subject:

“In high growth companies, sales productivity should be turning sideways or down. That's how you know you're hiring fast […] You think there's a reason why Snowflake gets more than a billion dollars of revenue, currently still growing north of 100%? It hasn't happened in the history of enterprise software to grow at that level of scale. There's lots of reasons why that happens. Okay? Because when you break down growth and all the different elements that go into it, I mean, all of them have to be thought about, managed and resourced”.

The strategy is costly. In 2021, 81% of revenue was committed to sales and marketing expenses. In 2022, it has gone down to 61% as revenue growth, larger customer relationships and renewal mix leading to lower commissions allowed for a significant improvement in operating leverage.

However, it is also working. The increased headcount coupled with industry vertical investments are yielding strong results. Last quarter, Snowflake had the largest number of net new bookings. Financial services, retail, advertising and media, health care and technology accounted for 85% of these. In just three months, Snowflake closed 7 deals at or above $30 million in total contract value.

Snowflake is also expanding its global footprint to EMEA, APJ and Latin America and invests in its partner network of data providers, resellers and system integrators to accelerate the platform adoption. In 2021, it introduced the Powered by Snowflake program to help customers and partners build applications using Snowflake. To date, there are over 285 Powered by Snowflake partners.

Though Snowflake is not active in the M&A space and prefers to spend money on sales and engineering talent, it has recently acquired Streamlit for $800 million in a 80% stock, 20% cash transaction. This company has an easy-to-use framework powering all sorts of applications for internal consumption of data within companies. Snowflake’s goal is to use this purchase to help companies build data applications and data experiences on Snowflake.

Revenue Breakdown and Key Business Metrics

Judging by all important business metrics, FY2022 was a stellar year for Snowflake.

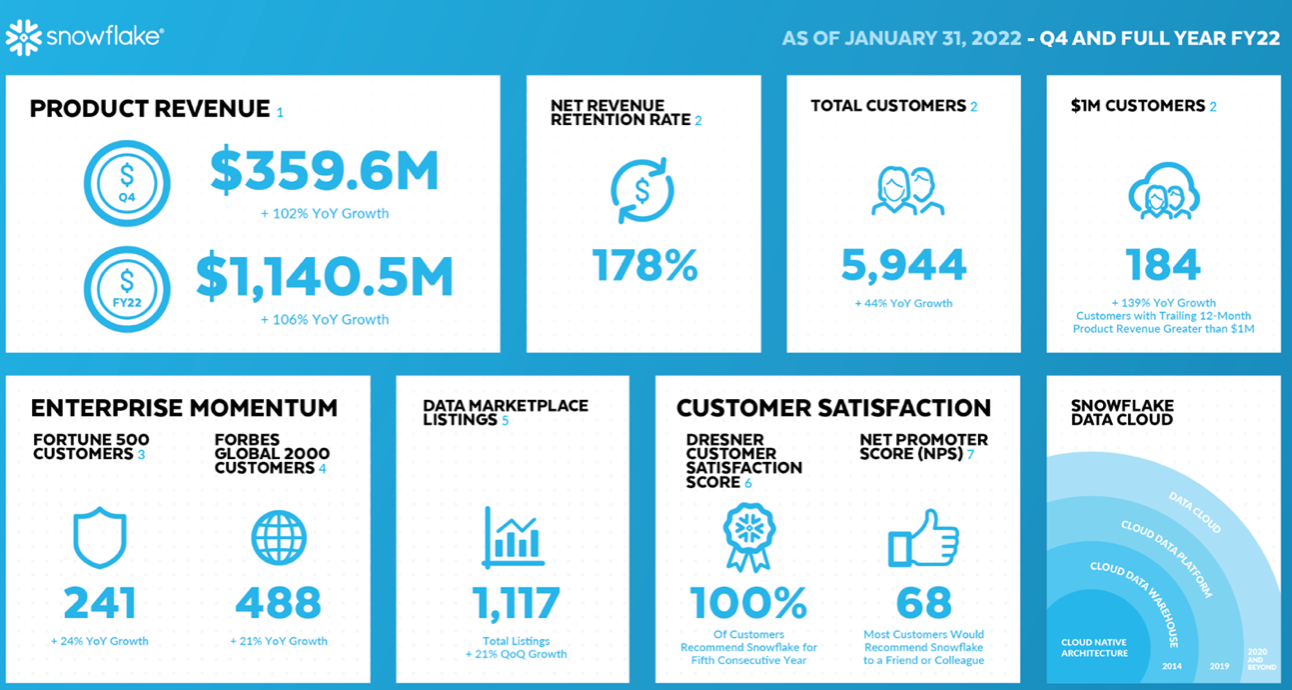

Snowflake’s revenue growth has been significant. Top-line grew 106% year-over-year from $592 million in 2021 to $1.2 billion in 2022. Net loss increased from $539.1 million to $679.9 million.

Product revenue surged by $586.7 to $1.14 billion, primarily due to higher consumption by existing customers and increased sales of higher-priced platform editions. Product revenue amounted to 94% of revenue.

Professional services and other revenue increased $40.6 million to $78.8 million and amounted to 6% of revenue. Deployment revenue represented approximately 1% of revenue.

Approximately 93% of revenue was derived from existing customers under capacity arrangements. Revenue derived from new customers under capacity arrangements represented approximately 4%. The remainder was driven by on-demand arrangements.

Remaining Performance Obligations (RPO) reflecting deferred revenue and committed unbilled backlog stood at $2.6 billion, representing year-on-year growth of 99%.

In 2022, Snowflake’s total customers grew at 44% year-over-year, increasing from 4,139 to 5,944. Snowflake’s customers include 241 companies from the Fortune 500 and 488 companies from the Global 2000 index. These companies were responsible for contributing approximately 26% and 40% of revenue respectively.

Net revenue retention rate for 2022 was incredibly strong amounting to 178% (by comparison, SaaS average is around 110-120%). Snowflake also boasts a 100% Dresner Customer Satisfaction Score for the fifth year in a row and an NPS Score of 68.

However, the management is also cautioning that in the near term, due to improvements of the platform leading to lower consumption, NRR will go down to stay above 150%.

Customers contributing more than $1 million in trailing 12-month product revenue grew at 139% growth year-over-year, increasing from 77 to 184. Such customers represented approximately 56% of product revenue for the trailing 12 months. Within these customers, Snowflake had 30 customers with product revenue greater than $5 million and 9 customers with product revenue greater than $10 million.

In 2022, Snowflake processed an average of over 1,496 million daily queries across all customer accounts, up from an average of over 777 million daily queries in the prior fiscal year.

Product gross margin also keeps improving. For 2022, it reached 70% (up from 65% in the prior year) in large part due to third-party cloud infrastructure discounts, higher consumption of compute resources and purchases of higher-priced platform editions. In Q4 2022, product gross margin reached 74% (growing 11 percentage points in two years).

Even though Snowflake intends to invest heavily to grow the business rather than optimize for profitability or cash flow in the near future, it seems able to pair high growth with improving unit economics and operational efficiency. Free cash flow keeps improving, pointing to the strength and performance of core business operations. GAAP net cash provided by (used in) operating activities went from negative $85 million to positive $81.2 million.

Snowflake data sharing also sees continued traction, as the number of stable edges grew 130% year-on-year. Snowflake Data Marketplace listings grew 195% with more than 1,100 data listings from over 230 providers.

When it comes to the competitive landscape, Snowflake makes no secret about going against Amazon, Google and Microsoft for on-prem migrations.

The company’s management is transparent in articulating that the competition with Google is most fierce. Their BigQuery product is probably the closest to Snowflake’s platform and Google is most competitive on deals.

Snowflake is confident that it has the technical upper hand but may still lose deals, as the behemoths can afford to throw in more things for free.

Interestingly enough, Snowflake has also co-sold $1.2 billion in contract value with cloud vendors (majority came from AWS and a small fraction from Microsoft). Snowflake also sees a 20% overlap within existing customers with Databricks which tends to do well with more sophisticated data scientists.

Finally, as we look ahead, C-level executives proclaim Snowflake is entering into larger customer relationships and customers' consumption is picking up.

When looking into the future, Michael Scarpelli, Snowflake’s CFO provides the following guidance:

“For the full fiscal 2023, we expect product revenue between $1.88 billion and $1.9 billion, representing year-over-year growth between 65% and 67%.

As we have mentioned before, certain product improvements create a revenue headwind for our business. We undertake these initiatives because they benefit our customers and expand our long-term market opportunity. Last year, we called out improvements in storage compression that reduced storage costs for our customers. Similarly, phased throughout this year, we are rolling out platform improvements within our cloud deployments. No two customers are the same, but our initial testing has shown performance improvements ranging on average from 10% to 20%.

We have assumed an approximately $97 million revenue impact in our full year forecast, but there is still uncertainty around the full impact these improvements can have. While these efforts negatively impact our revenue in the near term, over time, they lead customers to deploy more workloads to Snowflake due to the improved economics.

Turning to profitability. For the full year fiscal 2023, we expect, on a non-GAAP basis, 74.5% product gross margin, 1% operating margin and 15% adjusted free cash flow margin.” – Michael Scarpelli, Q4 2022 Earning Call

Conclusion

- Snowflake is a cloud data platform. Its integrated, end-to-end solution allows large companies to take their data from different sources, migrate it to the cloud, store it in one, safe place, and use it to gain business insights, build data-driven applications, and share it inside and outside their organizations.

- Snowflake’s platform solved a lot of pain points experienced in on-prem legacy solutions by eliminating data silos, removing data management and infrastructure complexities, improving the price-to-performance ratio and centralizing data in an analytics-ready format.

- Snowflake’s platform is built on a cloud-native architecture on three major public clouds and consists of three integrated layers across storage, compute, and cloud services.

- Use cases are vast. Data engineers can import and manage data or pull datasets from other sources. Analysts can track key business metrics, while data scientists can deploy ML for further insights. Developers can build data-driven apps, data brokers can sell datasets on the marketplace, and sales and marketing teams can elevate their game through enhanced analytical capabilities and better targeting.

- The product is easy to use and offers robust security and governance.

- Snowflake has a consumption-based business model, so customers are only charged for the resources they use.

- As the company improves features to make the platform more efficient, customers accomplish the same workloads with fewer resources. This negatively impacts revenue in the near term, but, over time, leads customers to deploy more workloads due to improved economics.

- Snowflake’s go-to-market strategy is to acquire new customers and drive increased platform use for existing customers, through a large direct sales force offering vertical-specific solutions and going after large organizations with vast amounts of data.

- The increased sales headcount coupled with industry vertical investments results in strong net new booking, with financial services, retail, advertising and media, health care and technology verticals leading the way.

- The company is entering into larger customer relationships and sees customers' consumption picking up.

- Snowflake is also expanding its global footprint to EMEA, APJ and Latin America and invests in its Powered by Snowflake program.

- Snowflake has also acquired Streamlit to help companies build data applications and data experiences on Snowflake.

- Google is the company’s most fierce competitor.

- Snowflake has recently co-sold $1.2 billion in contract value with Amazon and Microsoft.

- For the full fiscal 2023, Snowflake expects product revenue to grow 65% to 67% year-over-year.