Private Credit's Software Problem

Sign up for ARPU: Stay informed with our newsletter - or upgrade to bespoke intelligence.

Programming note: ARPU returns 23 March, where we will take a look at the real-world adoption of AI.

Software Cockroach

In the summer of last year, JPMorgan CEO Jamie Dimon offered a grim warning about the sudden collapse of a few obscure companies funded by private credit. "My antenna goes up when things like that happen," Dimon said. "When you see one cockroach, there are probably more."

For the last month, the $1.8 trillion private credit market has been frantically turning on the kitchen lights, terrified of what they might find scurrying across the floor.

The immediate catalyst for this panic is the "AI Scare Trade" we discussed in depth. The private credit industry has, for years, treated enterprise software like a financial perpetual motion machine. According to Pitchbook, software borrowers have been the primary engine of the private credit market since 2020, driving the rise of the "unitranche" loan—a structure that bundles various layers of debt into one massive, opaque check.

Lenders were drawn to what they thought was a safe business model: reliable subscription revenue and high switching costs that made software customers effectively captive. But that confidence has turned into a major pressure point. CNBC reports that software now accounts for roughly 17% of investments by all U.S. business development companies—essentially, private credit funds gussied up in a public ticker symbol—making it the second-largest exposure in the market.

Now that AI is threatening to allow those "captive" customers to cut the cord and build their own bespoke software, the market is re-evaluating the risk. UBS has warned that in an aggressive disruption scenario, default rates in private credit could spike to 13%—starkly higher than the stress projected for traditional high-yield bonds.

This fear has triggered a classic liquidity squeeze. Investors, spooked by the headlines, are demanding their money back from the private credit funds, forcing the biggest names in the industry into defensive postures:

- Blue Owl Capital: A major player in the space, Blue Owl saw withdrawal requests skyrocket to 15% in one of its funds—triple the usual limit. In response, it had to permanently halt redemptions for that vehicle and orchestrate a $1.4 billion asset sale just to return capital to investors.

- Blackstone: Earlier this month, Blackstone took the highly unusual step of having its own senior executives inject $150 million of their personal cash into a fund to meet investor demands and "show a sign of strength."

- BlackRock: Rather than injecting cash or selling assets, BlackRock simply pulled up the drawbridge on its HPS corporate lending fund last week, strictly enforcing its 5% cap on withdrawals and telling the rest of the queue they would just have to wait.

Cash Flow Shield

But if you look past the panic of the lenders and examine the actual balance sheets of the borrowers, a different picture emerges.

The market is treating every software company as if it is a cash-burning startup six months away from bankruptcy. But the reality is that the modern software industry is largely composed of mature, resilient cash-generating machines.

Looking at at the most recent Free Cash Flow (FCF) margins across the sector, the numbers do not quite support the idea of an imminent wave of defaults:

- Blue-Chip SaaS: Established players like Salesforce (35%) and Adobe (41%) remain dominant cash generators.

- Vertical Champions: Niche vertical softwares like Veeva Systems (44%) and AppFolio (25%) are operating at a high level.

- Cash-Flow Positive Growth: Some of the younger names such as Asana (10%) and Toast (10%) run much thinner. But they are still cash-flow positive.

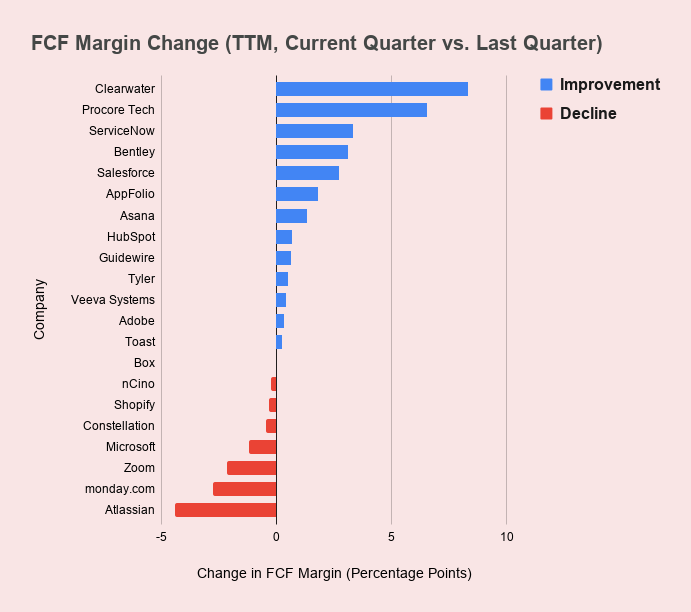

More tellingly, the majority of the vertical and horizontal software firms have improved or maintained their FCF margin according to latest data (see chart in Data > Narrative section below).

The underlying software companies are not going to default tomorrow because Anthropic released a new plug-in. They have a massive cash flow cushion that gives them years of runway to adapt, acquire, or pivot their way through the AI transition.

Liquidity Mismatch

So, if the underlying companies are still printing cash, why do private credit funds seem to be melting down? The problem is a sudden collision with the oldest rule in finance: maturity transformation.

Private credit funds took a highly illiquid asset (a 5-to-8 year private loan backed by the promise of future software subscriptions) and sold it to institutional and retail investors with the promise of 'semi-liquidity' (the ability to withdraw a portion of your money every quarter). This is the fundamental trade-off of the lending business. But that trade-off only works as long as everyone stays calm. The AI Scare Trade has effectively triggered a bank run on an asset class that doesn't have a central bank to backstop it.

When you buy a share of Salesforce, you can sell it in microseconds on an exchange. When you want to exit a $100 million private loan, there is no "sell" button. You have to hire lawyers, find a specific institutional buyer, and negotiate a price.

As Morningstar noted recently: "When too many people rush for the exits in a fund holding illiquid, hard-to-sell loans, the math stops working."

Blue Owl was forced to sell $1.4 billion of its loans not because the software companies had stopped paying interest, but because its own investors were panicking. They had to arrange a discrete, non-arm's-length transaction with a group of pension funds and insurance companies just to generate enough cash to appease the redemption.

Trouble with Being Private

This is the ultimate irony of the SaaSpocalypse as it applies to credit.

Software companies have the cash, for now, to survive the AI transition. The private credit funds that lent to them do not have the structural mechanics to survive a bank run.

Perhaps the market has misidentified the risk? Investors are dumping software stocks because they fear the AI revolution, but the real structural vulnerability lies with the funds that promised investors they could treat an illiquid, seven-year corporate loan like a high-yield checking account. As Brian Chappatta of Bloomberg noted: "Liquidity never matters until it matters."

And right now, for the private credit industry, it matters a lot.

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech. Monitor the industry vitals here (beta access).

Cash Flow Reality

- The Data: Horizontal and vertical SaaS players have increased their cash-flow efficiency:

- The Takeaway: Private credit investors are panicking about the long-term terminal value of software, while the companies themselves are busy strengthening their current ability to pay the rent.

P.S. we are launching the Tech Sector Diagnostics—a weekly tracker of how capital, margins, and multiples are flowing across tech companies. Click here for beta access.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.