Oil Shock and the Cost of Intelligence

Sign up for ARPU: Stay informed with our newsletter - or upgrade to bespoke intelligence.

Programming note: our next issue lands 6 April, where we will take a look at the memory crunch.

How to Fund AI with $100 Oil

During the past few years, the Federal Reserve has been trying to pull off a soft landing—bringing inflation down without crashing the economy—something akin to landing a 747 on a very short runway. If it worked, the payoff would be lower rates, easier financial conditions, and a gentler backdrop for risk assets. Meanwhile, the tech industry looked at that delicate macroeconomic balancing act and decided it was the perfect moment to borrow a few trillion dollars.

The working assumption in Silicon Valley—and, more importantly, on Wall Street—was that money was on a glide path back to being cheap. And if capital is getting cheaper, you lock in as much of it as possible to fund the AI arms race. Just a few weeks ago, Amazon sold a near-record $54 billion in investment-grade bonds, with demand reportedly four times oversubscribed.

That was the implicit wager behind the AI buildout: not just that demand for compute would explode, but that the macroeconomic conditions financing that buildout would steadily improve. The boom rested on three assumptions at once: cheaper capital, manageable energy costs, and durable enterprise demand.

Now all three are under pressure.

The US-Iran war has blown up the Fed's narrow runway. Oil is back around $100 a barrel and European natural gas prices have nearly doubled. The Strait of Hormuz is not just a headline; it is the physical transit point for 20% of global petroleum liquids and 19% of global liquefied natural gas (LNG). The obvious effect is higher energy costs. But the more important effect is macro: an energy shock revives inflation risk, gives the Fed less room to cut, and raises the odds that rates stay higher for longer.

And that matters because the AI boom was never just a software story. It was a capital-intensive financing story.

Shadow Debt

Tech monopolies are valued on the premise that they generate geysers of free cash flow without breaking a sweat. If one of them suddenly announces it needs to borrow $100 billion to pour concrete and buy electrical transformers, Wall Street analysts will start asking uncomfortable questions about return on invested capital.

Tech companies love looking asset-light until someone asks asset-heavy questions. So, the industry found a way to borrow the money without it ever showing up on their balance sheets, engaging in what the Bank for International Settlements (BIS) calls "shadow borrowing." The structure is simple:

- The hyperscaler partners with a private credit fund to create a Special Purpose Vehicle (SPV).

- The SPV technically owns the data center.

- The SPV borrows billions from insurers and asset-backed markets.

- The hyperscaler signs a long-term "Credit Tenant Lease," promising to pay rent for the capacity.

It is elegant financial alchemy. The hyperscaler gets the infrastructure without the debt landing cleanly on its own balance sheet. Lenders get what looks like safe, contracted cash flow backed by a trillion-dollar tenant.

But the lenders priced these loans like boring, risk-free infrastructure debt, forgetting that data centers are highly energy-intensive factories heavily exposed to the price of natural gas. With the inflation shock sending the 10-year Treasury yield spiking from 3.9% to around 4.4%, the cost to refinance this mountain of private credit just jumped. Suddenly, the SPV structure that looked so ruthlessly efficient in a low-rate world starts to look less like a clever workaround and more like a pressure point, squeezed simultaneously by surging operating costs and skyrocketing refinancing rates.

AI Labs' Two-Front War

A spike in energy prices will not bankrupt a hyperscaler, but it will erase the slack in the AI ecosystem. Even in highly efficient data centers, electricity dictates the operating margins. When a energy price shock compresses those margins, the entire system becomes less forgiving: compute gets more expensive, enterprise customers get cautious, and weaker business models lose their room for error.

Once the era of cheap power ends, the defining metric for an AI company shifts to sheer financial endurance. On this point, Parmy Olson of Bloomberg has argued that the AI labs themselves—companies like OpenAI and Anthropic—may be more insulated than the market assumes. After all, they sell software subscriptions, and running an existing AI model (inference) is cheaper than training a new one. They can just pause model development and ride out the storm, right?

But that view deeply understates how exposed the labs really are. They are not mature software businesses calmly harvesting subscription revenue; they are capital-intensive combatants in an arms race. If you stop pushing the frontier because capital is too tight, you lose relevance.

That leaves the AI labs fighting a brutal two-front war:

- The Financing Crunch: AI labs burn enormous amounts of cash, and they have increasingly turned to private credit to fund it. But private credit has its own problems. According to BIS data, private credit funds are currently sitting on over $500 billion in loans to legacy Software-as-a-Service (SaaS) companies. AI is actively disrupting those exact SaaS companies, whose stocks have been absolutely hammered. If private credit funds are taking losses on their legacy software portfolios and facing a rising base interest rate, they are going to pull back. The funds that were begging to finance AI at the peak of the hype cycle might suddenly stop returning calls.

- The Enterprise Pullback: AI labs are desperate to prove they are real enterprise businesses. They need massive corporations to sign massive contracts. If an energy-driven stagflation shock hits, CEOs get defensive. One of the first budgets to get reexamined will be the multi-million-dollar "experimental AI integration" budget.

Put differently, the question is no longer whether AI is important. It is who can still afford to compete when the easy money, cheap power, and expansive enterprise budgets of the last three years suddenly vanish.

Until now, the AI boom was mostly an abundance play. The geopolitical shock hasn't killed that story, but it has forced an economic reckoning.

When conditions tighten, markets do not die; they concentrate. The cash-rich hyperscalers consolidate their advantage, while the more speculative edge of the AI trade gets squeezed. In that environment, capital does not disappear; it gets choosier. And in periods of geopolitical stress, that capital rotates toward technologies with immediate strategic value—away from consumer chatbots and into defense software, intelligence systems, and autonomous weapons. The cost of intelligence is going up, and the winners will be the ones who can still afford to build it.

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech. Monitor the industry vitals here.

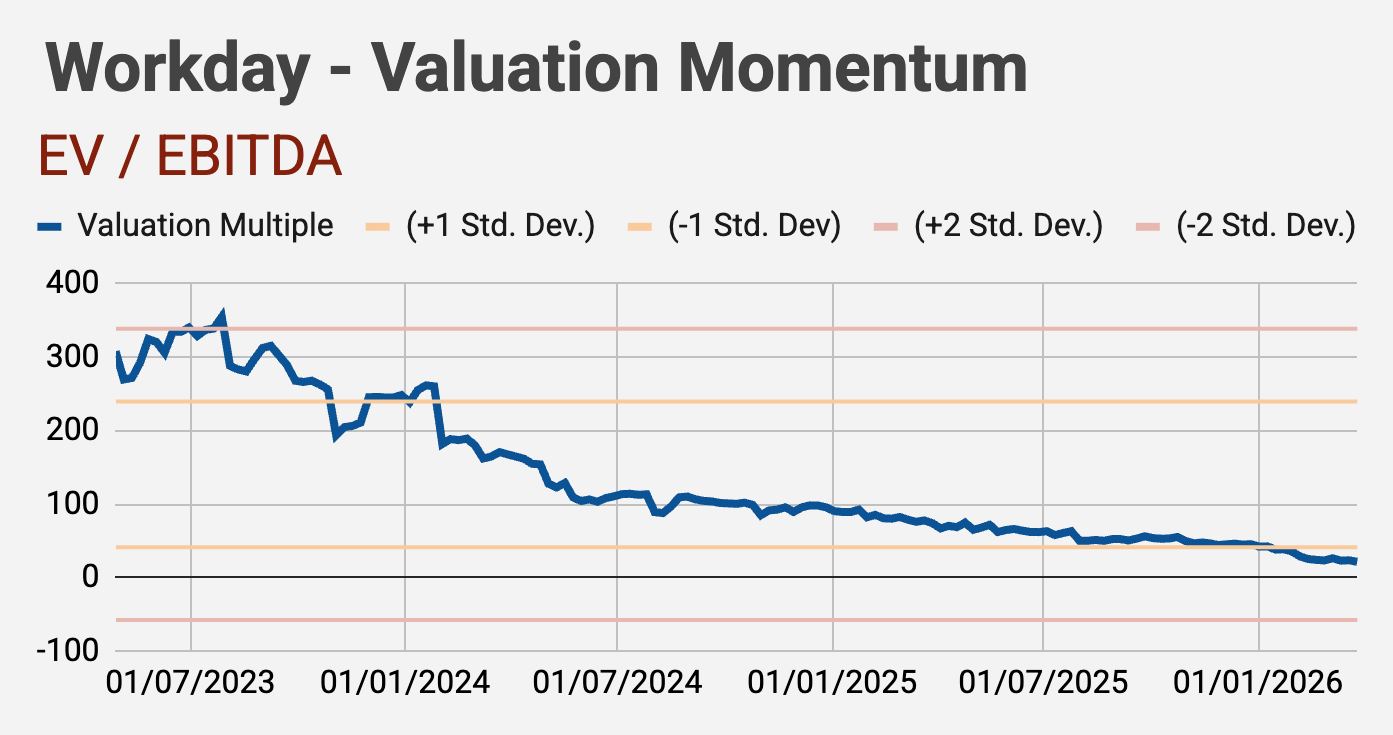

Workday's Re-Rating

- The Data: Workday's EV/EBITDA multiple fell from 42.5x in early January to 21.4x by late March, breaking well below the negative one standard deviation band of its historical range.

- The Takeaway: The market is no longer treating Workday like a premium-growth software name. It is being valued more like a maturing enterprise applications company facing slower growth, tougher demand, and less room for narrative premium. The debate now is whether this derating has already priced in the risk, or whether investors think back-office software deserves a structurally lower multiple in an AI-driven market.

P.S. In this week's Tech Sector Diagnostics (Software), we explore the valuation trends of the enterprise SaaS players. Download the 2-page PDF here.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.