Microsoft's AI Problem Is Not Demand. It's Regret.

Sign up for ARPU: Stay informed with our newsletter - or upgrade to bespoke intelligence.

A note before we start: we published "Two Clocks, One Stock" — a systematic framework for reading the gap between software valuations and operational reality. It scores every software name on two dimensions: where its trailing PE sits in its own three-year history, and where its operations do. The result is a four-quadrant diagnostic showing which regime each name occupies and what has historically followed each one. This is the methodology behind a weekly scan we are launching later this year — but with software down 25%, we think the framework is worth understanding now. Read it here. We return next Friday with Nvidia.

When Capital Discipline Backfires

Normally, the risk in an infrastructure boom is overbuilding. You spend too much, demand disappoints, and the shiny new capacity becomes an accounting problem.

Microsoft appears to have found a more awkward outcome: spending enough to worry investors, but not enough to avoid scarcity.

That, at least, is the uncomfortable implication of Bloomberg's profile of Amy Hood, Microsoft's longtime CFO. According to Bloomberg, Hood looked at Microsoft's late-2024 data-center expansion plans, questioned the reliability of internal demand projections, and hit the brakes on multiple projects.

The decision was controversial then. It looks even more awkward now: Microsoft is still constrained by data-center shortages, demand has outrun available capacity, and some of the sites it walked away from were later picked up by rivals.

The Most Expensive "Maybe" in Tech

The central problem of the AI buildout is that nobody really knows what the final demand curve looks like, but everyone is terrified of being the one who underbuilds.

That sounds like a perfect environment for a CFO to say no. It is also, unfortunately, a perfect environment for a CFO to be wrong in the most expensive way possible.

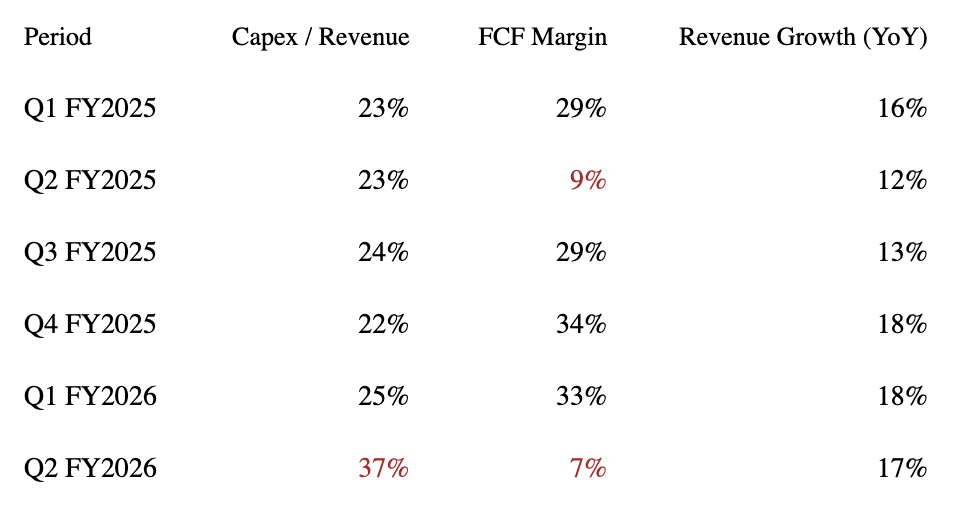

Microsoft's own financials show just how far the company has already gone. Capex as a percentage of revenue has climbed from 23% in Q1 2025 to 37% in the latest quarter. That is not a gentle increase. That is Microsoft spending like a company that has decided the future belongs to whoever can pour the most concrete around Nvidia chips.

And yet the return has not arrived in the tidy way investors were probably hoping. Quarterly revenue growth has remained in a relatively narrow mid-teens band — between 12% and 18% over the last several quarters. Free cash flow margin has plummeted. The forward P/E has de-rated from a peak of around 38x in mid-2024 to roughly 22x today, a meaningful compression for a company that was once treated as the cleanest AI monetization story in big tech.

The Cost of Being Rational for One Quarter

There is a familiar way to tell the Microsoft story. Microsoft made an early, brilliant bet on OpenAI, rode the first wave of generative AI enthusiasm, and is now prudently scaling into the next platform shift while keeping margins relatively intact.

Wall Street likes this version because it allows everyone to believe in both infinite AI upside and responsible adult supervision.

The less flattering version is that Microsoft may have tried to optimize too finely in the middle of a land grab.

Hood reportedly believed the company's demand projections were unreliable and worried the spending binge was getting out of hand. On ordinary corporate terms, that sounds sensible. On AI-infrastructure terms, it may have been like deciding in 1849 that the gold rush looked a bit overheated, so perhaps this is the moment to pause the shovel orders.

Hood later acknowledged that she had expected Microsoft to catch up with AI demand. As she put it on an earnings call: "I thought we were going to catch up. We are not."

That is the whole column, really. Microsoft's AI problem is not that demand is weak. It is that demand seems strong enough to justify overbuilding, but uncertain enough to make overbuilding feel insane right up until the moment you discover you needed the capacity after all.

Microsoft's Allocation Machine

The more interesting lesson here is not really about Amy Hood. It is about what Microsoft has become.

The company is still sold to investors as a software-and-cloud winner, but more and more of its business now behaves like a constrained utility. Compute has become a scarce internal resource. Demand has to be triaged. Capacity has to be rationed. Growth is no longer limited primarily by how much software Microsoft can sell, but by how much infrastructure it can bring online fast enough to support what it has already sold.

Bloomberg reports that Microsoft now holds regular internal fights over who gets access to scarce compute power, especially Nvidia chips. OpenAI wants them. Internal product teams want them. Sales wants to rent them out to customers. Nobody gets enough.

That is not the operating model of an abundant software platform. That is rationing.

And once a company starts rationing, it stops being a software story. It becomes a triage operation: which customer, which workload, which region justifies the next megawatt. These are not the glamorous questions of the AI boom. They are the ones that decide who actually monetizes it.

There is also a certain dark irony lurking in the company's own legal paperwork. Microsoft updated its Copilot terms of service last October to specify that the product is "for entertainment purposes only" and that users should "not rely on Copilot for important advice." A company spending $37.5 billion in a single quarter on AI infrastructure for a product its own terms of service call "entertainment purposes only" has a particular kind of problem.

The Wrong Kind of Scarcity

For Microsoft, it was never a choice between a good option and a bad one. Spend more aggressively, and investors worry that the company is torching margins on speculative demand. Stay too disciplined, and they worry the company is losing ground in AI. In this cycle, both excess and caution can look like strategic failure.

The problem is sharper because Microsoft does not appear to have the same silicon flexibility that Google has with TPUs. It still depends heavily on Nvidia's very expensive GPUs, while its own in-house AI chips do not yet seem mature enough to materially reduce that reliance. And increasingly, the buildout faces constraints that have nothing to do with capital allocation at all: shareholders are pressing the company on water usage, communities are pushing back on new sites, and regional power grids are not keeping pace with demand. The physics of infrastructure are catching up with the ambitions of the financial model.

The company is not being punished for refusing to spend. It is being punished because it spent heavily and still did not buy enough relief.

In a normal cycle, the danger is overbuilding. In this one, the greater danger turned out to be something stranger: pausing just long enough for scarcity to become someone else's advantage.

📊 Data > Narrative

We pull key data points to show you the mathematical reality of what's happening in tech. Monitor the industry vitals here.

Microsoft's Squeeze in Six Numbers

The Data: Over the past 6 quarters, Microsoft's capex burden as a share of revenue has risen by 10 percentage points — from 23% to 37%. Free cash flow margin has compressed in the opposite direction. Revenue growth, meanwhile, has barely moved: it sits at roughly the same level today as when the spending surge began.

The Takeaway: This is what a company looks like when it is paying the full cost of an infrastructure buildout without yet collecting the full return. The spending is real and already in the numbers. The payoff is still a forecast.

You received this message because you are subscribed to ARPU newsletter. If a friend forwarded you this message, sign up here to get it in your inbox.